If I had to boil it down to one line: franchises trade freedom for support, acquisitions trade speed for diligence risk, and startups trade control for uncertainty.

If I'm choosing between these three paths, I need to weigh six things first:

- Upfront cost

- Risk

- Time to cash flow

- Control

- Ability to grow

- Skill required

The article’s main takeaway is simple:

- I’d lean franchise if I want a system, training, and a lower-risk path.

- I’d lean acquisition if I want revenue on Day 1 and can review financials with care.

- I’d lean startup if I want full control and know my market well.

A few numbers stand out:

- Franchise fees often start around $15,000 to $60,000

- Franchise royalty and fee load can reach 7% to 11% of gross revenue

- Startups may take 12 to 24 months to break even

- Franchises may take 18 to 36 months to break even

- Many business purchases use pricing around 2x to 4x EBITDA

- About 42% of startups fail because there isn’t enough market need

Before I spend anything, I’d validate the idea and test:

- local demand

- competition

- pricing

- monthly burn

- break-even timing

- downside cash flow if sales come in 20% to 30% below plan

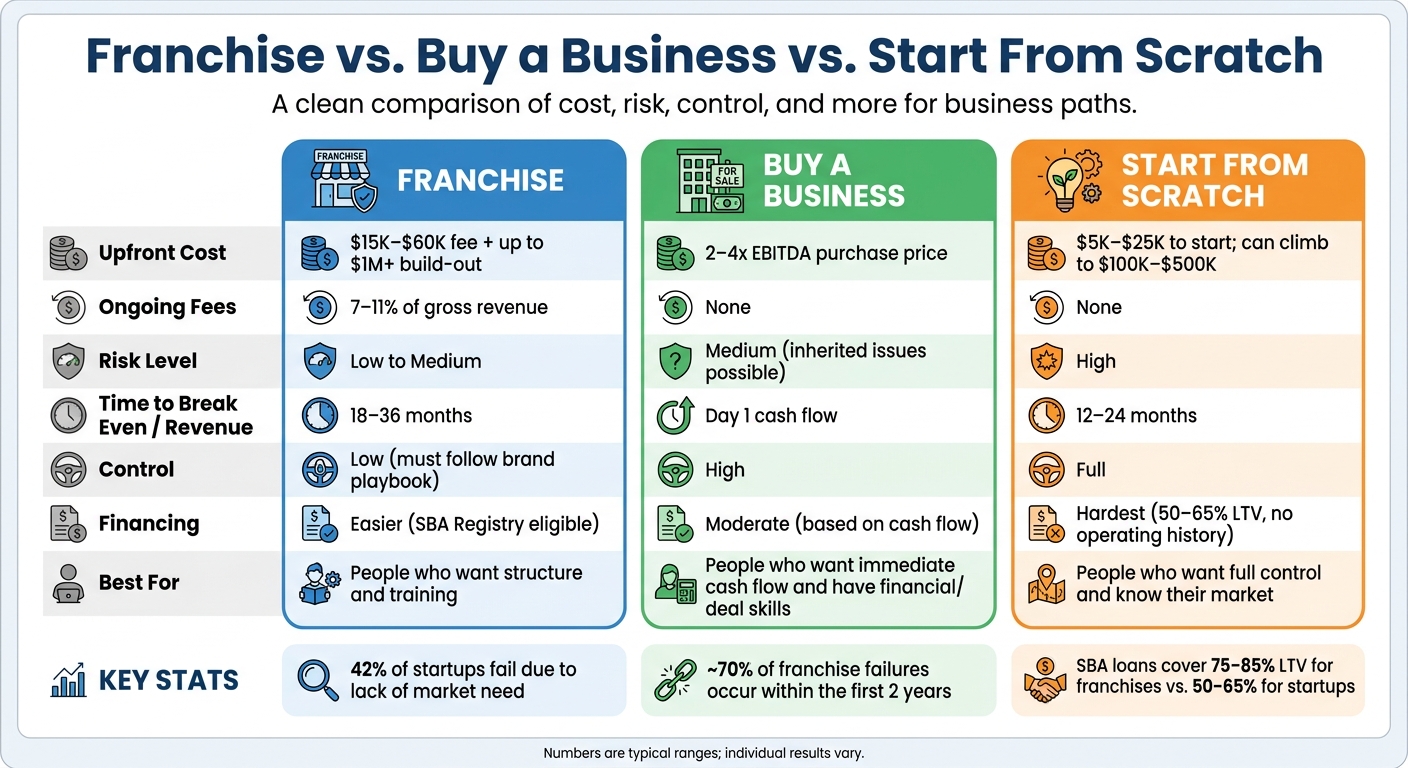

Franchise vs. Buy a Business vs. Start From Scratch: Side-by-Side Comparison

Should You Start a Business, Buy a Business, or Buy a Franchise?

sbb-itb-08dd11e

Quick Comparison

| Path | Upfront Cost | Risk | Time to Revenue | Control | Best For |

|---|---|---|---|---|---|

| Franchise | High | Low to medium | Medium | Low | People who want structure |

| Buy a Business | High | Medium | Fastest | High | People who want cash flow now |

| Start From Scratch | Low to medium at launch, but can climb fast | High | Slowest | Full | People who want full control |

My read: there’s no single best option. The right move depends on how much cash I have, accurately estimating startup costs, how soon I need to reach profitability, and whether I want a playbook or a blank page.

That’s the frame for the rest of the article.

Franchise vs. Buying a Business vs. Starting From Scratch: A Side-by-Side Look

Here’s the quick comparison.

| Factor | Franchise (New Unit) | Buying a Business | Starting From Scratch |

|---|---|---|---|

| Initial Investment | $15K–$60K fee + $100K–$1M+ build-out | Purchase price (often 2–4x EBITDA) | Variable; $5K–$25K branding/legal to start |

| Ongoing Fees | 7–11% of gross revenue | None | None |

| Risk Level | Low–Medium (proven system) | Medium (inherited issues) | High (highest uncertainty) |

| Speed to Predictable Revenue | Several months after build-out; 18–36 months to break even | Immediate (Day 1 cash flow) | 12–24 months to break even |

| Control | Low (must follow brand playbook) | High (more flexibility) | Full (complete creative freedom) |

| Scalability | High (systematized for replication) | Moderate (depends on existing systems) | High potential, hardest to build |

| Financing Difficulty | Low (SBA Registry) | Moderate (based on cash flow) | High (no operating history) |

The right path depends on three things: your budget, your goals, and how you plan and validate your business.

Franchise: Faster Systems, Less Freedom

A franchise is basically a shortcut. You’re buying a playbook that already exists: training, supply chain, operating process, and a brand people may already know. That usually lowers execution risk and cuts down the learning curve compared with building a business on your own.

The tradeoff is cost. Initial franchise fees usually land between $15,000 and $60,000, and build-out plus equipment can push the total investment past $1,000,000 for some concepts.

Then come the recurring charges. Royalties, ad fund payments, and required tech fees can stack up fast. In many cases, the total fee load reaches 7–11% of gross revenue. That also means less room to make your own calls. You may have limits on pricing, vendors, and even what kind of similar business you can open after you leave the system.

Buying a Business: Existing Cash Flow, Possible Hidden Problems

Buying an existing business lets you skip the startup stage. That’s the big draw. Instead of waiting months or years to get to stable sales, you may step into cash flow on Day 1. SBA 7(a) loans are often used for these deals, and in some cases the seller carries part of the note to help get the deal done.

But this path has its own trap: what you don’t see at first glance.

A business can look solid from the outside and still come with problems under the hood. Due diligence should cover:

- Tax returns

- Profit-and-loss statements

- Lease terms

- Customer concentration

- Key employee retention

- Deferred maintenance

- Online reputation

Any one of those can turn a deal that looks profitable into an expensive headache. That’s why diligence matters more than price alone.

Starting From Scratch: Full Control, Highest Uncertainty

Starting from scratch gives you the most control. You choose the brand, the pricing, the vendors, and the product. If you want to build things your way, this is the cleanest route.

It’s also the hardest one to get right. Most brick-and-mortar startups spend between $100,000 and $500,000 before reaching profitability, and branding plus legal setup alone usually costs $5,000 to $25,000.

The risk is not just the cost. About 42% of startups fail because there is no genuine market need, and nearly 60% of small business owners start with less than $25,000 in startup capital. That’s a rough mix: weak proof of demand and not enough cash to absorb mistakes.

Financing is tougher too. Lenders usually want more owner equity from startups, offering only 50–65% loan-to-value, compared with 75–85% for franchises in the SBA Registry. So yes, this route gives you full freedom, but freedom doesn’t pay the rent. If you know the industry well, starting from scratch can make sense. Still, you need strong market validation before you commit. Next, test demand and cash flow before you commit.

How to Match Each Path to Your Budget, Goals, and Experience

Use the criteria above to line up each path with your budget, goals, and experience. Then match those tradeoffs to the kind of owner you are.

| Entrepreneur Profile | Best Fit | Primary Reason |

|---|---|---|

| Needs structure | Franchise | Proven systems, training, and a support network |

| Needs faster revenue | Buying a Business | Immediate revenue from day one |

| Wants full control | Starting From Scratch | Total creative control and room for a novel concept |

| Has industry experience | Starting From Scratch | Avoids redundant training and ongoing royalties |

| Has financial or deal-analysis skill | Buying a Business | Can spot undervalued assets and improve margins |

The notes below break down why each option makes sense.

Best Fit if You Want Structure and Faster Revenue

If you're a first-time owner, a franchise is often the lower-risk place to start. Quick-service restaurant franchises with strong brand recognition typically reach 80% of mature revenue within 4–6 months, while independent counterparts often take 12–18 months. That's a big difference.

And it matters even more if you're carrying debt and need cash flow to settle things down.

If that sounds like your situation, support and speed matter more than full control. You're not trying to reinvent the wheel. You want a playbook, training, and a path that gets you to revenue sooner.

Best Fit if You Want Control and Long-Term Upside

Start from scratch if you know the industry and want full control. If you have the skills, a startup gives you full margin control. The tradeoff is time and risk, so make sure demand is validated before you spend.

This path tends to fit owners who care more about autonomy than plugging into a ready-made system. You get to shape the offer, brand, pricing, and customer experience from the ground up. That freedom can pay off, but only if the market is there.

Best Fit if Your Strength Is Financial or Operational Skill

Buying an existing business fits people who can read financials, spot operational inefficiencies, and manage existing staff and customer relationships. If you can buy a business, see where margins are leaking, modernize the operations, and keep the staff and customer base in place, you can create value fast.

For this kind of buyer, the upside comes from improving something that already exists. You're not starting with a blank page. You're stepping into a working business and making it run better.

The real filter is day-to-day fit: structure, control, or deal-making. The right path matches how you want to work, how fast you need revenue, and how much risk you can absorb. The next step is to test that decision before you spend any money.

How to Test Your Decision Before Spending Money

Before you spend a dollar, test demand and cash flow. The goal is simple: see how fast the business gets paid and how much faith you can put in the numbers. Use the six criteria above to pressure-test the path before you commit.

Check Local Demand and Competition First

Start with the market. Check demand, competition, and any customer groups that local players are overlooking before you decide if a franchise, acquisition, or startup is the right move.

If you're looking at a business to buy, watch customer concentration closely. If one client makes up more than 20% of revenue, the deal gets risky. That kind of setup can turn into a headache fast if that customer leaves.

If you're starting from scratch, don't lean on your own pitch. Make sure actual customers can explain the problem in their own words. That's a much better sign that the need is real.

Pricing matters just as much. If the model only works at a price your local market won't pay, the model breaks.

Build a Basic Cost and Cash Flow Model

If demand is there, the next step is checking whether the numbers still hold up. For each path, focus on:

- total upfront cash required

- monthly fixed costs

- gross margin per sale

- expected break-even month

For a franchise, your upfront total should include all franchise fees, the full build-out, and enough working capital to get through the first several months. Don't stop at the FDD Item 7 estimate. Build a month-by-month cash flow model for at least 24 months, because roughly 70% of franchise failures happen within the first two years. Also include all franchise fees. A 6% base royalty can end up at 11% to 12% once advertising and technology fees are added.

For an acquisition, calculate Durable Owner Cash Flow (DOCF) - the seller's earnings adjusted for owner replacement, ongoing capital expenditures, and debt service. Then run a downside case with revenue 20% to 30% below the last 12 months' average. That shows whether the business can still cover what it owes.

For a startup, estimate your Cash-to-Stabilize (CTS) - pre-launch costs plus monthly burn until break-even, with a buffer for the stuff you didn't price in yet. Set aside enough reserves to cover the full ramp period.

Use IdeaFloat to Run the Numbers on All Three Paths

Comparing three business paths by hand is slow, and it's easy to miss something. IdeaFloat gives you one place to work through demand checks, market sizing, cost analysis, pricing research, and cash flow projections using the same setup for each path.

You can use the Problem Validator and Consumer Insights tools to check whether real demand exists in your target market. The Competitor Analysis feature helps map the field and spot customer segments that aren't being served well. Smart Market Sizing gives you a grounded TAM/SAM/SOM estimate with verifiable sources, which helps whether you're building a business case or checking your own assumptions.

On the money side, Cost Analysis and the Financial Model let you plug in your own cost structure for each path and see what the numbers look like. Advanced Pricing Research helps you check market pricing against competitor data. Financial Projections maps month-by-month cash flow across best-case, base-case, and downside scenarios, so you can see how long your reserves last if revenue comes in at 50% of plan.

Use the same model for all three paths so the comparison stays clean.

Conclusion: Which Path Is Right for You?

After looking at cost, risk, speed, control, and skill needs, the choice comes down to fit. There’s no one-size-fits-all answer. It’s about picking the path that matches your capital, experience, and game plan.

Choose a franchise if you want a proven system, want to get to revenue faster, and don’t mind paying fees or giving up some freedom.

Choose an acquisition if you’re good at reviewing financials and want cash flow from day one, but can handle hidden risks that may come with the business.

Start from scratch if you know the industry well and want to keep all the upside. The tradeoff is more uncertainty and a longer road to profitability.

No matter which way you’re leaning, the same factors matter most: total cost, speed to revenue, level of control, and personal fit. Before you commit, check local demand and build a 24-month cash flow model with a 30% contingency buffer. If the downside case still works, you may have a path worth pursuing.

FAQs

Which path fits a first-time owner best?

There’s no single best path for every first-time owner. The right move depends on your goals, how much risk you’re okay with, and your finances.

For many beginners with no industry background, franchising is often the safest option because it comes with proven systems, training, and support. Buying a business can give you cash flow from day one, but you need to do careful due diligence. Starting from scratch gives you the most control and may cost less upfront, but it usually comes with the most uncertainty.

How much cash should I keep in reserve?

It depends on the path you take.

If you're starting from scratch, set aside enough working capital to cover 6 to 12 months of operating expenses. Revenue often takes time to build, and those first months can feel slower than expected.

For franchises, 3 to 6 months is often enough. If you're buying a business, keep cash in reserve beyond the down payment so you can handle early costs and keep things running.

In every case, base your reserve on conservative cash-flow estimates.

What should I check before buying a business?

Before buying a business, do thorough due diligence. That means digging deep enough to spot hidden risks before they become your problem.

Some of the biggest trouble spots are the ones you don't see right away:

- Undisclosed debts

- Lawsuits

- Tax issues

- Regulatory violations

You should also review the business from several angles, not just the headline numbers. Look closely at contracts, leases, cash flow, inventory, overall financial health, day-to-day operations, and market position. And don't ignore people-related issues. A deal can look fine on paper and still get messy if there are culture clashes or integration problems after the purchase.

The hard truth is that sellers may not disclose every issue. That's why it's smart to bring in an accountant and an attorney before you finalize the purchase. They can help you spot red flags, review the fine print, and keep a bad deal from slipping through.

Related Blog Posts

- How To Work Out Start-Up Costs: A Step-by-Step Guide

- Build vs Buy: Should You Start or Acquire a Business in 2025?

- 50 Small Business Ideas in Australia for 2025 (Sorted by Start-Up Cost)

- Local Service Businesses Ranked by Startup Cost, Margin, and Payback Period