The short answer: keep one startup story, but change the order, proof, and wording based on who is in the room. A technical investor may want architecture, performance, and why your product is hard to copy. A non-technical investor usually wants the problem, market, revenue path, and traction first.

If I were building this pitch, I’d keep the same base deck and change the emphasis around these points:

- Problem: show a clear pain point

- Solution: explain what the product does in plain English

- Market: use TAM, SAM, and SOM with cited numbers

- Business model: show pricing, CAC, and path to breakeven

- Traction: use pilots, revenue, benchmarks, or partner proof

- Team: link founder history to the problem

- Ask: tie funding to clear milestones

A good seed deck in the U.S. is often 9 to 12 slides. And one of the biggest pitch mistakes is simple: leading with deep product detail before the business case is clear.

Here’s the core split:

- For technical investors, I’d lead with how the system works, why it scales, and what makes it hard to copy.

- For non-technical investors, I’d lead with customer pain, market size, proof of demand, and how the company makes money.

- In both cases, I’d turn raw product claims into business outcomes like lower cost, faster delivery, fewer errors, or more revenue.

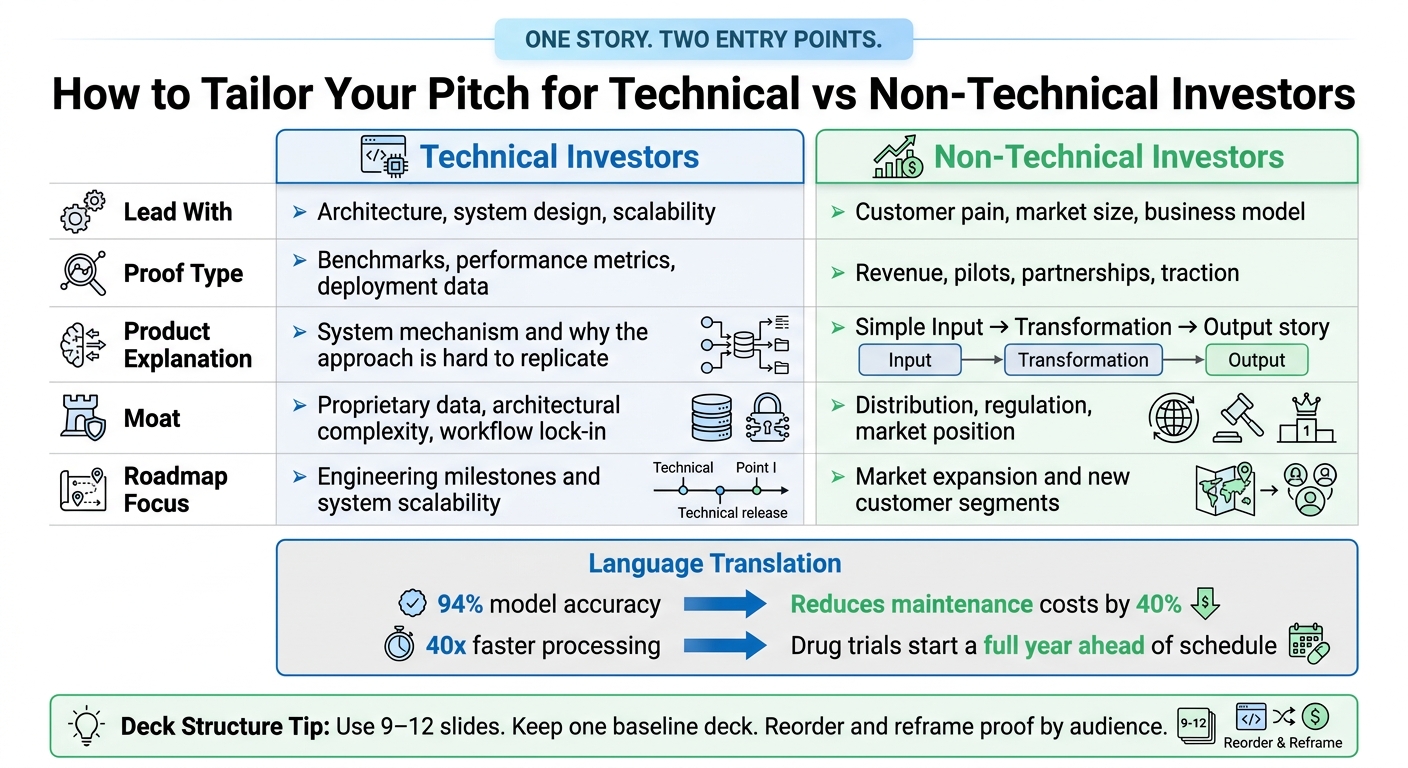

Technical vs Non-Technical Investors: How to Tailor Your Pitch Deck

What investors ACTUALLY want to see in your PITCH DECK

sbb-itb-08dd11e

Quick comparison

| Area | Technical investors want first | Non-technical investors want first |

|---|---|---|

| Problem | System gap or workflow failure | Customer pain and urgency |

| Product | High-level architecture | Simple input → output story |

| Proof | Benchmarks, performance, deployment | Revenue, pilots, partnerships |

| Moat | Data, architecture, system difficulty | Distribution, regulation, market position |

| Roadmap | Scale and engineering milestones | Growth and customer expansion |

Bottom line: I wouldn’t build two different company stories. I’d build one clear baseline, then shift the framing so each investor gets the proof they care about first.

Core pitch elements every investor wants to see

A U.S.-style seed deck usually lands at 9 to 12 slides and covers the basics investors expect: problem, solution, market, traction, business model, team, financials, and use of funds. That format keeps the deck easy to scan, whether you're presenting it live or sending it as a standalone PDF.

Problem, solution, and market proof

Start with a specific workflow failure. Show a pain point that's concrete, costly, and easy to grasp even for someone without a technical background. This isn't the moment for deep product architecture. Keep it simple and plainspoken.

For market proof, use cited TAM, SAM, and SOM numbers, not back-of-the-napkin guesses. If revenue is still early, build your proof around a simple four-part model:

- Baseline - what the user did before

- Intervention - what changed

- Outcome - what improved

- Timeframe - how long it took

For example: "Baseline: manual ticket triage; Intervention: automated ranking; Outcome: 40% faster prioritization; Timeframe: 60-day pilot." That kind of proof keeps the story clear for both technical and non-technical investors.

Once the problem and proof make sense, the next job is to show how the startup turns that value into revenue.

Business model, team, and financial logic

Investors want a realistic path to revenue with stated assumptions around pricing, customer acquisition cost, and breakeven timing. If your pricing model is still in flux, say how you're working through it - for example, by testing different licensing models with early partners.

Your ask should be tied to what it unlocks: commercial pilots, patents, or another concrete milestone. On the team slide, connect each founder's background straight to the problem. Confidence goes up when an investor can quickly see why this team should be the one solving this problem.

Using IdeaFloat to prepare the shared investor baseline

Building this baseline from scratch can eat up a lot of time. IdeaFloat can help with problem validation, consumer insights, market sizing with verifiable sources, pricing research, and financial projections, so you have the core material ready before tailoring it for different audiences. The Financial Projections & Breakeven Analysis tool creates month-by-month revenue and cost forecasts, and the Business Plan Generator exports a polished investor plan in PDF, Word, or PowerPoint. That gives you one steady starting point for both pitch versions.

This baseline stays the same. The next step is deciding what technical investors need first - and what non-technical investors need translated.

How to pitch technical investors

Technical investors want proof that the product can be built, can scale, and can stand up against copycats. The core story doesn't change. The evidence does.

Lead with architecture, performance, and hard-to-copy advantage

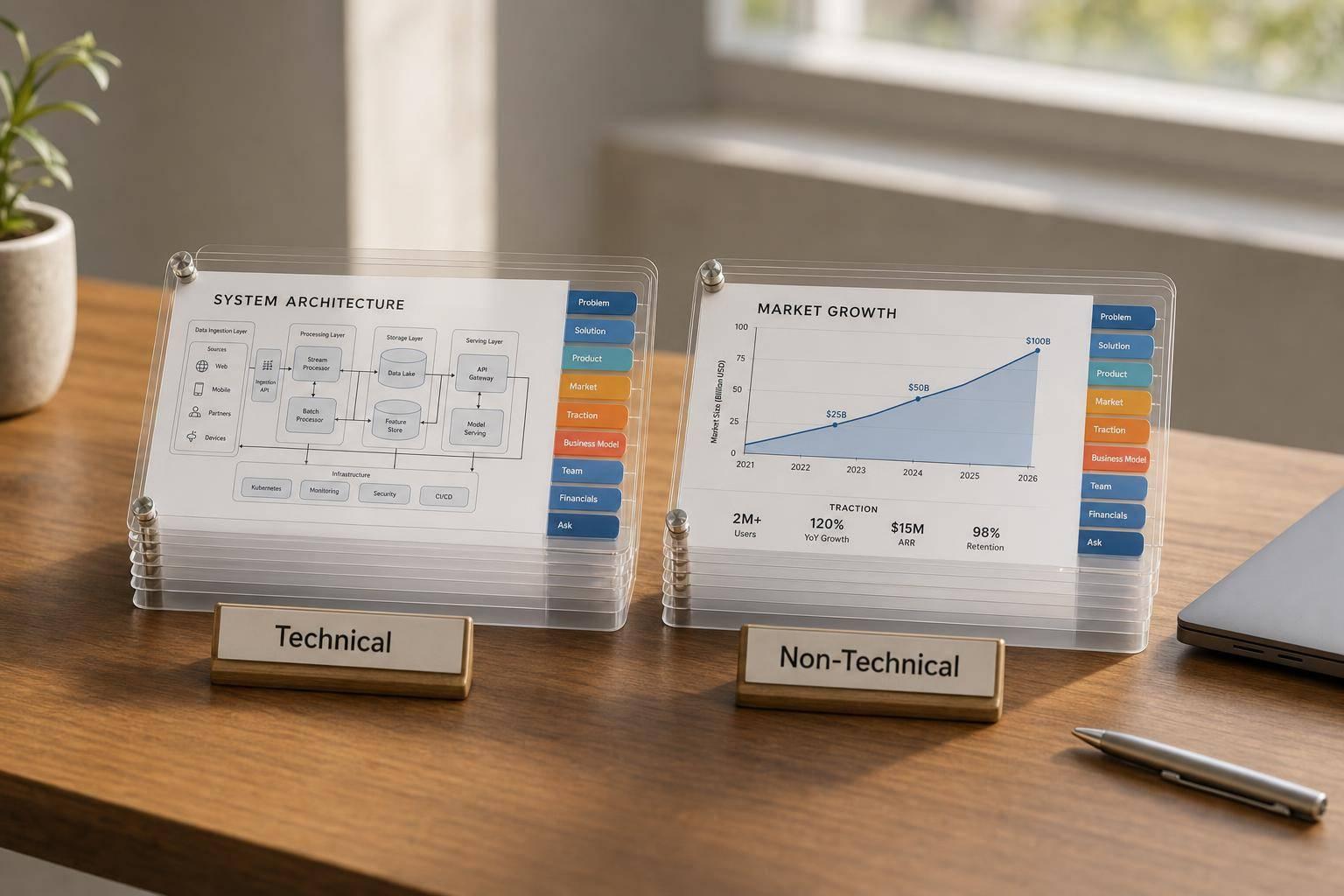

Open with one architecture slide that moves left to right: customer or data input on the left, your core product layer in the middle, and the business outcome on the right. Keep it simple. One diagram. Clear labels. This is not where you dump a full system spec. It’s a high-level map that helps a technical investor see, fast, how the product works at the system level.

Once that picture is clear, explain why the product is hard to copy. Say exactly what the hard-to-copy asset is: proprietary data, workflow lock-in, or regulatory advantage. Then support that claim with numbers. Show inference cost, uptime targets, throughput, or deployment complexity. Use language tied to results, not jargon. Instead of “classification engine,” say “prioritizes critical issues in real time”. If your setup lets customers deploy in two weeks instead of three months, say that plainly.

Connect engineering decisions to business outcomes

Every engineering choice should lead to a business result. A technical investor doesn’t just care that your model is accurate. They care what that accuracy does for the company.

A raw metric like “94% accuracy” lands better when you frame it as “reduces maintenance costs by 40%”. That gives the number a job to do. Tie each technical term to something concrete, like speed, cost, sustainability, or scale. Also explain the why now angle. If the product only became commercially practical because inference costs dropped or a new regulatory framework changed the math, spell that out. It shows you understand more than the product itself.

Save the deep technical proof for backup materials.

Use appendices and IdeaFloat outputs to back up diligence questions

Detailed security architecture, model benchmarks, integration maps, and data flow diagrams belong in the appendix or your data room, not in the main story . Keep the main deck tight. Put the proof where investors can pull it up when they want to dig in.

IdeaFloat can help build that support layer:

- The Competitor Analysis tool maps the competitive landscape with sourced data, which helps back up defensibility claims.

- The Cost Analysis and Financial Projections & Breakeven Analysis tools give you cost models and forecasts that technical investors often test during due diligence.

- The Lean Canvas export gives you a one-page summary you can drop into a data room fast.

That same core story now needs a different emphasis for non-technical investors.

How to pitch non-technical investors

Non-technical investors care most about business logic. They want to see a painful problem, a clear product, a big market, strong execution, and tech that’s hard to copy. So start with the business opportunity, then show how the tech backs it up. For this audience, clear beats deep.

Begin with the problem, market size, and business model. Save the deeper technical material for later. When you explain the product, stay at the level of how it works, not the nuts and bolts behind it. A simple input → transformation → output explanation is usually enough. Once the business story lands, tie the tech to customer results and revenue.

Lead with market, proof of progress, and business model

Start with the problem and why it matters now. Show that the market is big enough to matter and that the solution is easy to grasp fast. If you have proof of progress, put it up front. Pilots, partnerships, and regulatory steps tend to land better than a long feature list.

Once the business case is clear, connect the technology to customer impact and financial results.

Translate technical claims into customer and financial value

"Technical founders typically speak in terms of capabilities: what the technology does. Investors listen for outcomes: what the technology means for the market, for growth, for returns." - Brehnor Communications

A simple shift in framing can make the same fact hit much harder:

| Technical Framing | Investor Translation |

|---|---|

| "Proprietary algorithm achieves 94% accuracy in predictive maintenance" | "We eliminate unplanned downtime; customers see failures 48 hours before they happen." |

| "40x faster processing" | "Drug trials start a full year ahead of schedule." |

If a technical claim doesn’t connect to speed, cost, scale, or sustainability, move it to the appendix or save it for Q&A.

Use IdeaFloat to build market and financial storytelling

Use IdeaFloat to build TAM/SAM/SOM, pricing, GTM assumptions, and investor-ready projections for non-technical readers.

Use these translations to adjust your deck slide by slide.

A side-by-side framework for adapting one deck

Use one deck, then reorder and reframe it for each audience. The facts don’t change. The story doesn’t change either. What changes is which proof you lead with, how much detail you give, and how each slide is framed.

That’s the key idea here: one company, one core narrative, two ways in.

What to change by slide: technical vs. non-technical

The table below shows what each investor type usually wants first. If you lead with the right proof, the rest of the deck lands more cleanly.

| Slide | Non-Technical Emphasis | Technical Emphasis |

|---|---|---|

| Problem | Customer pain scenario and market urgency | Specific technical gap or unsolved workflow inefficiency |

| Product | High-level mechanism: Input → Transformation → Output | System mechanism and why this approach works differently |

| Moat | Structural barriers: data access, regulation, distribution | Architectural decisions that are hard to replicate |

| Traction | Revenue, pilot logos, market momentum | Technical milestones, benchmarks, expert validation |

| Roadmap | Market expansion and new customer segments | Engineering milestones and system scalability |

| Backup slides | Detailed financial models and GTM strategy | Security protocols, data flows, technical benchmarks |

Use the main deck to make the business case. Then use backup slides for the deep proof.

Language swaps that improve clarity and relevance

After the slide order is set, tighten the wording. Then translate the same claim into the kind of language each investor is most likely to trust.

| Technical Language | Outcome-Focused Translation |

|---|---|

| "Inference pipeline" | "Delivers answers to users in milliseconds" |

| "Policy framework and retrieval engine" | "Enforces security rules automatically" |

| "Model achieves 94% accuracy" | "Cuts false positives by 40% and saves 8 hours a week" |

Use one anchor term across the deck. That small choice helps people track your story without stopping to decode new phrasing on every slide.

Conclusion: Keep one story, change the emphasis

The core facts of your company don’t change from one investor meeting to the next. The entry point does.

For technical investors, trust usually comes from depth on architecture and performance. For non-technical investors, trust usually starts with business logic that feels hard to argue with, then moves into the tech. Same facts. Different order, different emphasis, different words.

FAQs

How do I know if an investor is technical or non-technical?

Pay close attention to the questions they ask and the parts of the pitch they zero in on. That tells you what matters most to them.

Technical investors tend to ask about product architecture, scalability, technical defensibility, execution, risks, and validation.

Non-technical investors usually care more about market opportunity, business model, traction, team strength, return potential, customer benefits, and market timing.

Their language and priorities give you a clear cue on how to shape your pitch. Speak to what they care about, not just what you want to say.

What should I cut if my pitch deck is too technical?

Cut deep technical detail, dense architecture diagrams, and step-by-step lab methods.

Keep the high-level system view, the core mechanism, and a clear explanation of how the technology creates value or defensibility.

How much technical detail belongs in the appendix?

Put the technical details in the appendix as backup for the technical claims in your main pitch, not in the main presentation itself.

That way, the core pitch stays clear and easy to follow, while investors still have proof behind your technical points.

Related Blog Posts

- Tailoring Pitches for Technical vs Non-Technical Audiences

- Why Investors Rejected My First Pitch But Funded My Second

- I Analyzed 200 Successful Pitch Decks - Here's What Works

- I Analyzed 50 Successful Pitch Decks - Here Are the Patterns Nobody Talks About