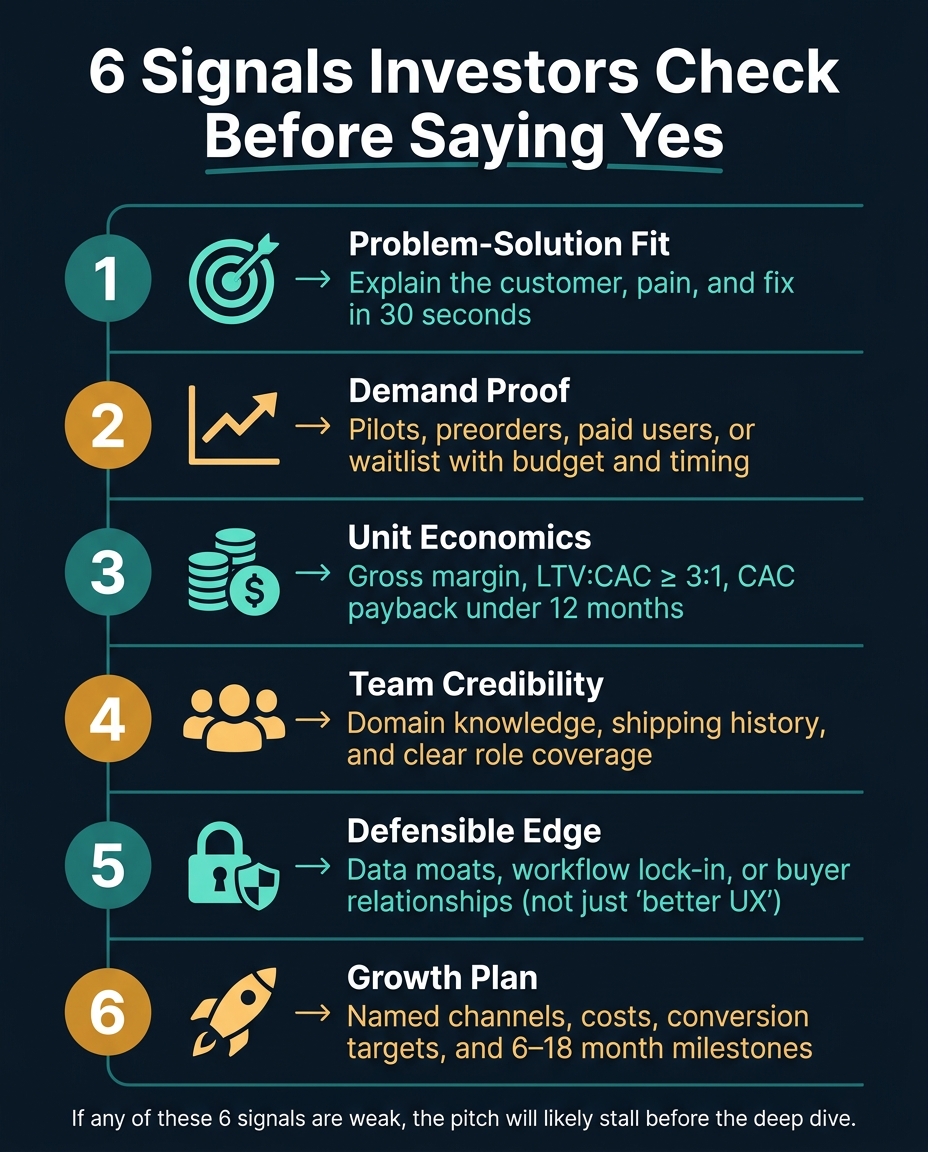

Most investors decide fast. Before they study a spreadsheet, they usually look for six things: a clear problem, proof people want the fix, healthy unit economics, a team that can ship, an edge that is hard to copy, and a plain growth plan.

If I were getting ready to pitch, I’d check these points first:

- Problem: Can I explain the customer, pain, and fix in 30 seconds?

- Demand: Do I have proof beyond interest, like pilots, preorders, paid users, or a waitlist with budget and timing?

- Economics: Can I show core numbers like gross margin, LTV:CAC near 3:1, and CAC payback under 12 months?

- Team: Can I show why this team can execute, with direct market knowledge and clear roles?

- Edge: Can I point to data, workflow lock-in, or buyer relationships instead of vague claims like “better UX” or “AI”?

- Growth: Can I name channels, costs, targets, and what the money will do over the next 6–18 months?

Here’s the short version: investors don’t back loose stories. They look for proof, clear math, and a path from early traction to repeatable sales. If any of those pieces are weak, the pitch will often stall before the deep dive starts.

| Checkpoint | What I’d want ready |

|---|---|

| Problem-solution fit | One-sentence pain point, clear buyer, plain fix |

| Demand proof | Paid users, pilots, preorders, or strong waitlist signals |

| Unit economics | Margin, CAC, LTV, payback, burn, runway |

| Team | Domain knowledge, shipping history, role coverage |

| Differentiation | Proof-backed moat tied to retention, pricing, or acquisition |

| Growth plan | Channel mix, budget, conversion targets, milestones |

This article breaks those six signals into a simple pre-pitch checklist I can use before I start investor meetings.

6 Things Investors Look For Before Backing a Startup

What Investors Really Think During Your Pitch | Perfecting the Pitch | Shark Tank Global

1. Problem-solution fit: Can an investor understand the value in 30 seconds?

Investors usually start with one simple test: does this solve a real, specific problem? If that’s not clear right away, many of them move on. A vague idea is hard to back. That first impression acts like a filter.

Show a painful problem, a clear customer, and a direct fix

A strong opening should answer three things fast: who has the problem, how much it hurts, and what your product does to fix it. Name the customer, the pain, and the cost.

For example: "Independent restaurant owners in U.S. cities lose an average of 8–12% of monthly revenue because they can't track food waste accurately." That line does a lot of work. It points to the customer, puts a number on the loss, and leads straight to the fix.

Your solution should sound like the obvious answer, not just a neat feature. Use the words customers use. Skip the jargon. If a feature doesn’t tie back to the pain you just named, it will likely confuse people instead of winning them over.

A good gut check: if someone outside your field can’t repeat it back after hearing it once, rewrite it.

If you can land the problem in one sentence, investors will usually move to the next test: have people already shown demand for it?

Validate the problem before building the full pitch

Clear pitches start before the pitch itself. They start with proof. Customer interviews help show that the pain is real, common, and bad enough that people are already trying to patch it on their own. Workarounds like spreadsheets, manual hacks, or duct-taped processes are strong signs that the problem has teeth.

IdeaFloat's Problem Validator helps founders turn “we think this is a big problem” into claims they can test and back up. By gathering responses from target customers on frequency, severity, and current options, founders can build pitch lines based on data instead of guesswork. A line like “In interviews with 75 U.S. freelance designers, 70% face late payments at least once a month, costing them $500 or more each time” carries far more weight than a broad complaint about payment issues.

The Consumer Insights feature records the exact words customers use to talk about their pain. That matters. Investors tend to trust pitches that sound like they came from real conversations, not from a whiteboard session. As Kristine, founder of Locker, put it:

"Inspiration can strike at any time: I was sent a link two weeks ago and now I can't remember who sent it... the screenshot is lost on my camera roll."

That kind of language makes the problem feel immediate. Swapping internal jargon for phrases pulled from customer interviews gives investors something solid to react to, instead of asking them to take a fuzzy claim at face value.

Once the problem is clear, the next step is to show that customers already want the fix. That proof of pain leads straight into the next test: demand and whether the business can make money.

2. Demand and economics: Is there proof people want this, and can it make money?

Once the problem is clear, investors usually move to two plain questions: Will people pay for this? And can this turn into a business that scales without burning cash?

Replace headline market claims with demand evidence investors can verify

Bottom-up market sizing tends to land better than a big top-down market slide. A giant industry number may look nice in a deck, but investors want something they can pick apart and test.

The better move is to count the customers you can actually reach, multiply that by pricing that makes sense, and show the assumptions behind it. For example: "10 million US freelancers × $300/year software spend = $3 billion TAM." That gives investors a number they can pressure-test.

Still, even neat TAM/SAM/SOM math doesn't close the case by itself. Investors want proof that people are ready to do more than nod along. As David Bradshaw, a startup financing expert, puts it:

"What investors look for is evidence that customers or founders have already committed money, time, or budget."

| Evidence Type | Investor Confidence | Risk |

|---|---|---|

| Large TAM slide only | Low | High - assumptions may not translate into actual sales |

| Survey responses ("I would buy this") | Low to medium | High - interest doesn't equal purchase intent |

| Qualified waitlist with a stated budget and buying timeline | Medium to high | Lower - shows intent from a defined audience |

| Paying customers, preorders, or signed pilots | High | Low - proves willingness to pay and commercial viability |

What matters most is demand proof that also hints at healthy growth economics. Interest is nice. Paid traction is better.

Prove the unit economics work at small scale and at higher volume

After demand, investors look at whether each new sale gets more efficient as you grow. Even at pre-seed, they want to see the core numbers: gross margin, CAC, LTV, payback period, burn, and runway.

A good target is at least a 3:1 LTV:CAC ratio and CAC payback under 12 months. Some seed investors will accept up to 18 months.

| Metric | Strong Signal | Weak Signal | Likely Investor Reaction |

|---|---|---|---|

| Gross margin | High enough to fund marketing and overhead | Thin margins with little room to scale | Concern about scalability and cash burn |

| LTV:CAC ratio | 3:1 or better | Below 3:1 or not calculated | Questions about efficiency and growth viability |

| CAC payback period | Under 12 months | 24+ months with no improvement trend | Worry about cash timing and runway pressure |

| Burn rate and runway | Enough runway to hit the next milestone | Short runway with no clear inflection point | Pressure to raise again soon; execution risk |

| Pricing logic | Tested with real customers or A/B data | Chosen mainly to undercut price without margin analysis | Likely margin erosion or future churn |

If the numbers come from early cohorts, say that plainly. That's fine. What investors want is a founder who knows what the data means and can explain where improvement should come from. Maybe CAC drops as your channel mix shifts. Maybe retention gets better as the product gets stickier. Maybe pricing gets tighter after testing. Early numbers don't have to be perfect, but they do need to show a direction.

Use IdeaFloat to turn assumptions into numbers you can defend

IdeaFloat's Smart Market Sizing, Waitlist Landing Page, Cost Analysis, Advanced Pricing Research, and Financial Projections tools help turn rough assumptions into numbers you can stand behind. That means a bottom-up market model, qualified demand signals, a clear cost structure, tested pricing, and a view of breakeven timing.

The goal is simple: move from "we think this works" to evidence investors can inspect rather than brush off.

If demand and economics hold up, the next thing investors want to know is whether the founder can execute with a clear edge.

sbb-itb-08dd11e

3. Team and differentiation: Why investors back capable founders with a clear edge

You can have a clear problem, decent unit economics, and proof that demand is there. A pitch can still stall if investors don't believe your team can deliver, or if the business feels easy to copy.

That’s the tension. Investors aren’t just asking whether the market is real. They’re asking who will win and why others won’t catch up fast. Those two risks - execution risk and competitive risk - often decide whether a deal moves forward or dies in the room.

Founder credibility comes from domain knowledge and execution proof

A Harvard Business Review study of 885 VCs found 95% rank the management team first because investors are backing execution, not just ideas.

What earns trust usually isn’t a résumé packed with famous logos. It’s direct contact with the problem and the customer. Investors want to see that you’ve lived this pain, know how buyers think, and understand the day-to-day work in a way outsiders don’t.

A founder who spent seven years in restaurant operations, interviewed 60 operators, shipped an MVP in eight weeks, and lifted activation from 30% to 62% shows both domain knowledge and the ability to get things done.

"It's important to show investors that there is not a concentration risk on one person and that a team has formed that is both complementary and efficient for assigning the right work."

Clear roles matter too. Investors want to know there’s coverage across product, sales, and operations. They also want to know who owns each area. A simple line like this helps right away: I lead product and data, my co-founder owns enterprise sales, and our third partner manages operations and forecasting. That cuts uncertainty fast.

Defensible differentiation must be specific, not generic

Claims like “better UX” or “we use AI” don’t do much. Anyone can say that. Anyone can copy that too.

What gets attention is something structural: an edge that becomes harder to match as the company grows. In plain English, investors want proof that your edge isn’t just marketing copy.

A good example looks like this: We trained our model on three years of proprietary transaction data from 50,000 small businesses, which reduces fraud losses by 22% - a dataset competitors can't buy or recreate quickly.

Here’s how weak claims stack up against the kind of proof investors actually test:

| Claim | Proof | Barrier to Entry |

|---|---|---|

| Our workflow cuts onboarding time by 60%, validated with 25 clinics | Quantified time savings from a real pilot | Medium-high - requires deep process knowledge and integrations |

| We trained on 3 years of proprietary data from 50,000 small businesses; fraud losses down 22% | Exclusive dataset with measurable outcome | High - data is unique and not replicable |

| Once customers integrate our tool into their approval workflow, switching takes months | Retention data and workflow dependency | High - structural lock-in with real switching costs |

The pattern is simple: tie every differentiation claim to a barrier. That barrier might come from data, relationships, workflow lock-in, time, or deep know-how. If a well-funded competitor could rebuild it in a few months, it’s not much of a moat.

Organize your story clearly with IdeaFloat

IdeaFloat helps keep the pitch, memo, and follow-up centered on the same edge.

- The Competitor Analysis tool maps direct and indirect competitors so founders can see where they actually win.

- The Unique Value Proposition tool turns that edge into one clear statement that can anchor the whole deck.

- The Lean Canvas puts the problem, solution, unfair advantage, and key metrics on one page, which makes weak spots easier to spot before investors do.

Used together, these tools keep the investor story lined up across the pitch, memo, and follow-up.

Once the team and edge are clear, investors want to see how you will reach customers efficiently.

4. Growth plan and final checklist: What makes a pitch feel ready now

After investors understand the problem, demand, economics, and your edge, they look for one last thing: a clear path to growth.

A believable go-to-market plan names channels, costs, and milestones

Once investors buy into your edge, they move to the next test: can you turn that edge into repeatable growth?

Product alone won't get a yes.

A stronger version sounds like this: "We're allocating $250,000 to test three paid acquisition channels, reach 1,000 trial users, and convert 8% to paid in 18 months." That works because it ties the growth story to three things investors can check: channel, cost, and milestone.

Your raise needs that same level of detail. Spell out how much you're raising, what the money will fund, when those results should show up, and what each budget line is meant to produce before the next raise.

Milestones matter because they show whether the company can hit the next proof point before cash runs out. Each one - whether it's a revenue target, customer count, retention goal, or product release - should be specific enough that an investor can review progress six to twelve months after investing without needing extra internal context.

For example, saying paid search generated leads at $18 each, converted 14% to paid, and paid back CAC in four months is the kind of channel-level, cost-based, milestone-linked claim that builds confidence.

Investor-readiness checklist to complete before fundraising

Use this as a final pass/fail check before you send the deck. If several of these points feel weak or unanswered, the pitch is probably too early. In most cases, tightening the proof first is a better use of time than booking investor meetings too soon.

Before sending a deck or taking a meeting, founders should be able to answer these clearly:

- Clear customer pain - Can you explain the problem in one sentence and say who feels it most?

- Demand proof - Do you have pilot results, paid trials, waitlist signups, or repeat usage data?

- Margins and CAC/LTV logic - Do the unit economics work at small scale, and do they still work as volume grows?

- Founder credibility - Can you show domain knowledge and proof that you can execute?

- Defensible differentiation - Does your edge help acquisition, retention, or pricing?

- Channel-specific growth plan - Do you know which channels you'll use, what each lead costs, and what conversion looks like?

Conclusion: The signals that make investors lean in

Investors back businesses that show demand, economics, execution, and a clear growth path.

IdeaFloat can help founders work through each of these signals before they walk into a room - testing assumptions, building investor-ready documents, and replacing guesswork with evidence that stands up under pressure.

FAQs

What if I don't have paying customers yet?

If you don't have paying customers yet, swap sales numbers for proof that people want this. Investors aren't looking for vague interest. They want hard signals that the problem is real and that people care enough to act.

That proof can come from pre-orders, beta users, customer research, manual workarounds, waitlist growth, feedback, or landing-page clicks that point to purchase intent. You should also show why your team is well suited to solve this problem, along with a clear plan backed by data.

How much traction is enough for a first investor meeting?

There’s no set revenue number you need before your first investor meeting. What matters more is clear proof that people want what you’re building and are willing to pay for it.

That proof can show up in a few different ways:

- Pre-orders

- Paid pilots

- Early customer acquisition

- User growth

- Retention

- Documented customer feedback

What investors want is tangible proof of commercial viability, not just an idea that sounds good on paper.

Which metric matters most at the pre-seed stage?

At the pre-seed stage, user growth and product adoption matter most. Early startups usually don't have much revenue history, so investors look at these numbers to check for market demand and see whether the idea has real commercial potential.

You should still be ready to talk about burn rate, customer acquisition cost, and gross margins. But in most cases, active user adoption is the clearest proof of concept.

Related Blog Posts

- What Sharks Look for Before Investing (Real Examples)

- What Really Makes a Business Plan Attractive to Investors

- Why Investors Rejected My First Pitch But Funded My Second

- I Analyzed 200 Successful Pitch Decks - Here's What Works