Securing a small business loan in Australia can feel overwhelming, but preparation is key. Here’s what you need to know:

- Eligibility Basics: Have an active ABN or ACN, at least 6–12 months of trading history, and a monthly revenue of $10,000+.

- Key Documents: Be ready with bank statements, profit and loss reports, balance sheets, and Business Activity Statements. Ensure they’re accurate and free of red flags.

- Credit Score: A score of 400+ is typically required, but higher scores (550–625+) improve approval odds and lower interest rates.

- Loan Purpose: Clearly explain why you need the loan and how it will benefit your business. Specificity matters.

- Lender Options: Choose between banks (lower rates, slower process), online lenders (faster approvals, higher rates), or government programs (specialized support).

Pro Tip: Avoid common pitfalls like incomplete documentation or unclear financial plans. Proper preparation can save you time and improve your chances of approval.

Want to dive deeper into the loan process, lender types, or credit score tips? Keep reading for a full breakdown.

Preparing for an Unsecured Business Loan: A Guide for Small Australian Businesses

Basic Eligibility Requirements

Before you start gathering documents for an Australian small business loan in 2025, it’s important to understand the key eligibility criteria. These requirements are the foundation of the application process, acting as an initial filter. If you don’t meet them, your application might not even make it to the underwriting stage. Thankfully, these criteria are fairly straightforward for established businesses.

Business Registration and Legal Status

Lenders will always verify that your business is legally registered and operating within Australia. A valid Australian Business Number (ABN) is essential to confirm your business's legitimacy. Additionally, you’ll need to provide proof of your business structure - whether you're a sole trader, a partnership, or a company. For companies, an Australian Company Number (ACN) and evidence of GST registration (if applicable) are typically required.

The applicant, whether a business owner or the primary contact, must generally be an Australian citizen or permanent resident. If the application is on behalf of a corporation, all directors and guarantors will need to provide valid, government-issued photo identification, like an Australian driver’s license or passport. Be sure that the names on your ID match exactly with those on your business registration documents to avoid delays in processing.

Business Age and Revenue Requirements

Lenders often want to see that your business has a track record of stability and revenue generation. Most traditional lenders require your business to have been operating for at least 6 to 12 months to demonstrate that your business model is viable and capable of generating consistent income. For larger loans or better terms, some banks might ask for over two years of trading history.

Revenue is just as important as trading history. Typically, lenders expect a minimum of 6–12 months of trading history with monthly sales of at least $10,000. For higher loan amounts or secured loans, the bar is often set higher, with annual sales requirements of $500,000 or more. To support your application, you may need to provide additional documentation, such as detailed cash-flow projections, a solid business plan, and proof of contracts or purchase orders that indicate future revenue.

Once you’ve confirmed that you meet these basic requirements, you can start compiling the necessary documents to strengthen your application.

Required Documents Checklist

Once you've confirmed your eligibility, it's time to gather the essential documents needed for your loan application. This step often trips up many applicants - 61% of Australian SMEs abandon loan applications because of documentation issues. To avoid delays, ensure you have everything ready, especially if you're applying to multiple lenders.

Personal and Business Identification

Lenders need to confirm both your identity and the legitimacy of your business. Start by providing a valid government-issued photo ID, such as an Australian driver's license or passport. If your business has multiple directors or partners, each individual must submit their own identification documents.

For your business, you'll need an active Australian Business Number (ABN) or Australian Company Number (ACN). Additionally, provide proof of your business structure, whether you're operating as a sole trader, partnership, or company, along with any necessary business licenses. If your annual turnover exceeds $75,000, most traditional lenders will also require proof of GST registration.

Once these identification requirements are squared away, move on to your financial records to show the stability of your business.

Financial Records

Your financial records paint a clear picture of your business's cash flow and revenue trends. Most lenders will ask for 3 to 12 months of business bank statements to assess deposits, withdrawals, and overall liquidity. Before submitting, review these statements for any potential red flags, like missed payments or irregular cash flow, that could raise concerns during the underwriting process.

"Understanding what your bank statements are going to look like to the lender is a big thing. You've got to be ready to answer questions about the incomings and outgoings. If you're not, you could get caught out." - Andrew Beckett, Head of Broker and Third Party Distribution

You’ll also need to provide Business Activity Statements (BAS) for the past 12 months and business tax returns covering 1 to 3 years. These documents help demonstrate tax compliance and historical earnings. Lenders often check for any outstanding tax debts with the Australian Taxation Office (ATO), so make sure your tax portal is clear or that you have a formal payment plan in place. These records are crucial for proving your business's operational consistency and can significantly improve your chances of approval.

To further strengthen your case, include detailed financial statements.

Financial Statements

Financial statements give lenders a comprehensive view of your business's financial health and repayment ability. The three primary documents you'll need are:

- Profit and Loss (P&L) Statement: Highlights your business's profitability over time.

- Balance Sheet: Lists your assets and liabilities, providing a snapshot of your financial position.

- Cash Flow Statement: Demonstrates your ability to manage liquidity and meet financial obligations.

Using accounting software to generate accurate and timely reports can make this process smoother. For small businesses, lenders may also request personal tax returns and statements of personal assets and liabilities from directors or owners. Additionally, providing signed contracts, service agreements, or outstanding invoices (accounts receivable) can help showcase future earning potential and a reliable revenue pipeline.

Together, these documents provide a complete picture of your business’s financial stability and repayment capacity, helping you make a strong case for loan approval.

How to Improve Your Credit Score

Your credit score plays a big role in whether lenders approve your applications and the interest rates they offer. A higher score not only boosts your chances of approval but can also save you money by securing lower rates. In Australia, both personal and business credit histories matter - especially since small business loans often require personal guarantees, making the director's credit score a key factor in the approval process.

Minimum Credit Score Requirements

In Australia, the minimum credit score for business loans is typically around 400. However, major banks generally look for scores of 625 or higher for automated approvals, while online lenders often accept applicants with scores of 550 or above. Credit score ranges vary by bureau, so it’s important to check your standing across the three major bureaus:

| Bureau | Score Range | Good Threshold | Average Range |

|---|---|---|---|

| Equifax | 0–1,200 | 622–725 | 510–621 |

| Experian | 0–1,000 | 625–699 | 550–624 |

| Illion | 0–1,000 | 625–699 | 550–624 |

Your credit score doesn’t just determine approval - it also impacts the interest rate you’ll pay. For example, on a US$30,000 car loan over five years, someone with an excellent score (800+) might get a 6.5% rate, paying around US$5,195 in total interest. On the other hand, a below-average score (under 600) could lead to an 18% rate, with total interest ballooning to roughly US$15,593. As Andrew Beckett, Head of Broker and Third Party Distribution, explains:

"Understanding your credit score... is also going to set your expectations on what your rate's going to be".

Credit Score Improvement Tips

Improving your credit score takes effort, but some actions can deliver quicker results. Since payment history makes up 35% of your score, missing even one payment can have a big impact. Setting up automatic payments for utilities and loans can help avoid late payments, which are typically reported when overdue by 14–60 days.

Another tip: keep your credit utilization below 30%. If your balances exceed 75% of your available credit, your score could drop by 20–50 points. Paying down high balances can lead to noticeable improvements within a few months. Avoid maxing out credit lines, as it signals financial overextension.

Errors on credit reports can cost you 50–100 points, so regularly request free reports from Equifax, Experian, and Illion, and dispute any inaccuracies promptly.

It’s also wise to limit new credit inquiries before applying for a major loan. Having five or more inquiries in just three months can lower your score by 40–60 points and trigger a "credit hungry" flag for lenders. If you’re rate shopping, use the 14-day rule - multiple inquiries for the same type of credit within a 14-day period count as a single inquiry.

Diversifying your credit mix can also help. For instance, using a mix of credit types, like a business credit card and a term loan, shows lenders you can manage different financial obligations. Lastly, avoid closing old accounts, even if unused, as this can shorten your credit history and temporarily lower your score. If your score still falls short of traditional benchmarks, don’t worry - alternative lending options might be the solution.

Alternative Lenders for Lower Credit Scores

If your credit score doesn’t meet the criteria of traditional lenders, online and alternative lenders can be a lifeline. Many of these lenders are more flexible, accepting scores as low as 550 or even lower. In fact, 15% of small and medium enterprises (SMEs) turn to alternative lenders because they’re willing to work with borrowers who have poor credit histories.

These lenders focus more on your current business performance - such as steady revenue and cash flow - rather than past credit issues. They also tend to process approvals much faster, often within hours or a single business day, compared to the longer timelines of traditional banks. However, this convenience comes with trade-offs: higher interest rates, shorter repayment terms, and risk-based pricing. On the bright side, the application process is simpler, often requiring just three to six months of bank statements.

If you go this route, make sure you’re prepared for the higher costs, but also use the opportunity to strengthen your overall credit profile. This can improve your chances with traditional lenders in the future.

sbb-itb-08dd11e

Preparing Your Business for Loan Applications

Getting ready to apply for a loan involves careful financial planning and showing lenders that you have the means to repay the borrowed money. Lenders want to see that you’ve clearly identified your financial needs and can handle the responsibility of repayment. A well-prepared application signals that you’re serious about your business and understand how the loan will support your growth plans.

Start by defining your loan purpose clearly, as it sets the tone for the rest of your application.

Define Your Loan Purpose

Lenders need to understand exactly why you’re borrowing money and how it will help your business generate enough cash flow to repay the loan. Common reasons for borrowing include covering seasonal cash flow gaps, buying equipment, purchasing bulk inventory, or hiring additional staff. A vague explanation, like “I need US$50,000 for business expenses,” can indicate poor planning.

Instead, be specific. For example: “US$50,000 will purchase inventory projected to generate US$120,000 in revenue within six months, ensuring repayment within 12 months.” This level of detail demonstrates that you’ve thought through the financial impact of the loan.

Show Consistent Revenue

To assess your ability to repay, lenders will look for proof of steady income. Be prepared to provide at least six months of bank statements to verify your cash flow. If your business has been operating for over a year, include two to three years of financial statements, such as profit and loss reports and balance sheets, to showcase your long-term performance. Additionally, up-to-date Business Activity Statements and Australian Taxation Office records can serve as official income verification.

Make sure your financial documents support the revenue trends you outline, as this will strengthen your application.

Business Plans and Financial Projections

"Your lender doesn't know your business like you do. A business plan is a great way of helping them understand your business and goals."

A solid business plan is key to helping lenders see your vision. Include an executive summary, market analysis (preferably with a SWOT breakdown), product details, and an organizational chart. Financial projections are just as critical - they should cover the entire loan term or at least three years. Work with your accountant to prepare a sensitivity analysis that accounts for 10% variations in turnover.

If you’re a startup with less than 12 months of trading history, a business plan and cash flow projections are non-negotiable. For instance, Westpac offers startup loans ranging from US$10,000 to US$50,000, but approval depends on showing the business’s future potential through detailed projections.

Collateral and Security Options

Offering collateral can help you secure better loan terms and borrow larger amounts. Secured loans, backed by assets like property, equipment, or inventory, often come with higher borrowing limits and lower interest rates since they reduce the lender’s risk. On the flip side, unsecured loans - relying on your business’s cash flow - are usually capped at US$250,000 or less and carry higher interest rates.

If property isn’t an option, some lenders accept alternative forms of collateral, such as accounts receivable (unpaid invoices) or inventory. For example, invoice financing allows businesses to access up to 85% of the value of approved unpaid invoices, often within 24 hours. It’s also worth noting that in Australia, lenders commonly require personal guarantees from all company directors, even for incorporated businesses, pledging personal assets as additional security.

These steps, combined with well-organized financial records, can make your loan application more compelling to lenders.

Understanding Lender Types and Government Programs

Australian Small Business Loan Requirements: Banks vs Online Lenders vs Government Programs

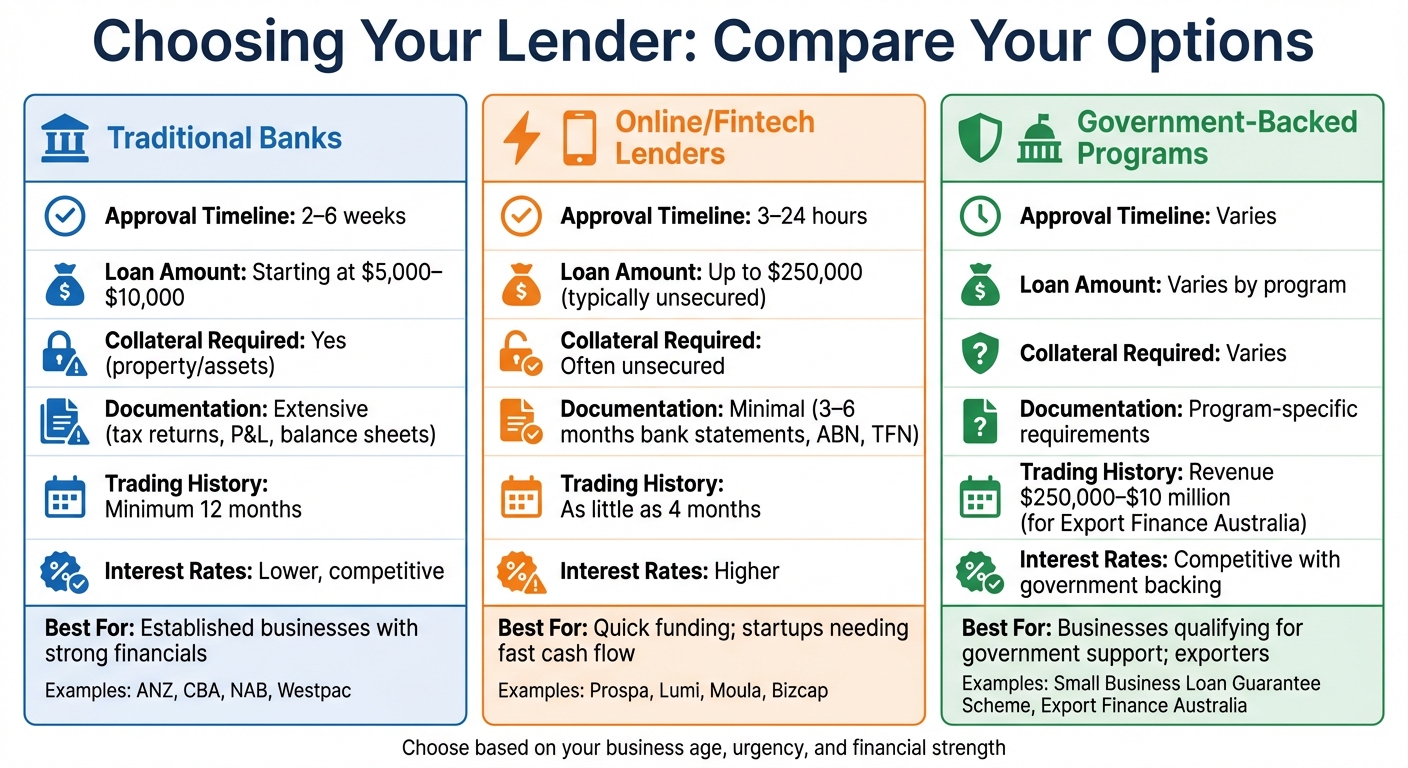

Choosing the right lender is crucial when seeking funding. In Australia, there are four main types of lenders: major banks (like ANZ, CBA, NAB, and Westpac), online fintech lenders (such as Prospa, Lumi, Moula, and Bizcap), specialist lenders for unique market needs, and government-supported programs. Each option comes with its own set of requirements, approval times, and interest rates.

Major banks typically require 1–2 years of financial statements and physical collateral, like real estate. While the process may take longer, they often offer lower interest rates and more competitive terms.

Online lenders focus on speed and convenience, using technology to review bank statements and transaction data. They can provide unsecured loans within hours or days, but their interest rates are usually higher.

Specialist lenders are designed for borrowers with specific needs or those facing credit challenges. These lenders often charge higher rates to account for the increased risk.

Additionally, government programs offer funding opportunities for businesses that meet certain criteria, providing an alternative to traditional lending.

Government-Backed Loan Programs

The Australian Government supports small businesses through various loan initiatives. One example is the Small Business Loan Guarantee Scheme, which backs a portion of eligible loans. This allows lenders to offer more flexible financing options, particularly for businesses that might not qualify under standard lending criteria. Another key program is Export Finance Australia, which provides targeted assistance to businesses involved in international trade. This includes working capital guarantees and export credit insurance. To qualify, businesses often need to demonstrate a solid trading history and meet revenue thresholds, such as annual revenue between $250,000 and $10 million.

Export Finance Australia

Export Finance Australia plays a critical role in supporting businesses engaged in international trade. By offering tools like export credit insurance and direct loans, it helps companies manage cash flow challenges caused by extended international payment cycles. This program is especially beneficial for exporters looking to bridge market gaps.

Traditional Bank Loan Requirements

When applying for a loan from a major bank, businesses typically need to meet strict requirements. Loans generally start at US$5,000–US$10,000 and require extensive documentation, including tax returns, profit and loss statements, and balance sheets. A minimum of 12 months of trading history is also necessary, along with collateral such as property or other assets. Approval timelines can range from 2 to 6 weeks.

| Lender Type | Approval Timeline | Collateral Required? | Best For |

|---|---|---|---|

| Traditional Banks | 2–6 weeks | Usually (property/assets) | Established businesses with strong financials |

| Online/Fintech Lenders | 3–24 hours | Often unsecured | Quick funding; startups needing fast cash flow |

| Government-Backed Programs | Varies | Varies | Businesses qualifying for government support |

Unsecured Loan Application Timeline

For businesses needing funds urgently, unsecured loans from online lenders can be a lifesaver. Providers like Bizcap can approve applications in as little as 3 hours, provided the necessary documents are ready. Typically, this includes 3–6 months of bank statements, a valid Tax File Number (TFN), and an Australian Business Number (ABN). While these loans come with higher interest rates due to the lack of collateral, they are perfect for short-term needs like purchasing inventory or covering payroll.

Key Takeaways for Loan Approval

When it comes to securing a small business loan in Australia, preparation and attention to detail can make all the difference. Beyond meeting basic eligibility requirements, focusing on the finer points of your application can significantly improve your chances of success.

To qualify, you’ll need an active ABN or ACN, a trading history of 6–12 months (or as little as 4 months for some online lenders), and a minimum monthly revenue of $10,000–$12,000. Both personal and business credit scores are important, with many lenders requiring a minimum score of 400.

Surprisingly, 61% of small businesses abandon their loan applications due to documentation errors. To avoid this, ensure you have the necessary paperwork ready, including 6–12 months of bank statements, profit and loss statements, balance sheets, and Business Activity Statements. It’s also wise to review your bank statements for any red flags, such as irregular transactions or large cash withdrawals, which may raise concerns about your financial habits. Be prepared to explain these transactions if needed, as lenders often look for clarity and financial discipline.

Choosing the right lender is equally critical. Traditional banks may offer competitive interest rates but often require a strong financial history and collateral. On the other hand, online lenders provide faster approvals with fewer documentation requirements, making them a good option for businesses seeking quick access to working capital. For larger loan amounts, keep in mind that nearly half of small business loans in Australia are secured with residential mortgages. If you’re looking for unsecured loans under $250,000, fintech lenders can be a quicker alternative, though their interest rates tend to be higher.

Another important factor is clearly defining your loan purpose. Lenders are wary of businesses heavily reliant on just one or two customers, as this concentration of revenue can signal risk. A detailed business plan, complete with cash flow projections, can go a long way in demonstrating professionalism and improving your credibility - even for smaller loan amounts.

FAQs

What’s the difference between getting a small business loan from a bank versus an online lender?

When it comes to small business loans, the choice between traditional banks and online lenders boils down to differences in their application processes, approval standards, and overall flexibility.

Traditional banks often have stricter requirements. They’ll typically ask for detailed financial records, collateral, and a solid credit score. The application process can feel old-school - think in-person visits, stacks of paperwork, and waiting weeks for a decision. While this route might work for established businesses with strong financials, it’s not always ideal if you're short on time or lack certain documentation.

On the other hand, online lenders streamline the process. Applications are completed entirely online, and in some cases, you might receive approval within a day. These lenders tend to be more flexible, focusing on cash flow and business performance rather than just your credit score or collateral. They also offer a broader range of loan options, like short-term loans or invoice financing. That said, the convenience often comes with a tradeoff - expect higher interest rates or fees.

Ultimately, the right choice depends on your business’s unique needs, how quickly you need funding, and your financial situation.

What steps can I take to improve my credit score for better loan approval chances?

Improving your credit score can significantly boost your chances of getting a loan. Start by checking your business credit report regularly to ensure all the details are accurate and current. If you spot any errors, address them promptly to avoid unnecessary hits to your score.

Paying your bills on time is another critical step. This includes supplier invoices, loans, and credit accounts. Consistent, timely payments demonstrate reliability and strengthen your creditworthiness. Also, keep your debt levels low in relation to your credit limits. High credit utilization can negatively impact your score, so aim to use only a small portion of your available credit.

By sticking to these practices, you can build a healthier credit profile, making your business more attractive to lenders and improving your odds of loan approval.

What documents should I prepare to avoid delays when applying for a small business loan?

To keep the process of applying for a small business loan as smooth and efficient as possible, it’s important to have all the required documents prepared in advance. Start with your financial statements from the past year - these help show your business’s financial stability and ability to repay the loan. Additionally, include bank statements from the last 3–6 months to give the lender a clear picture of your cash flow.

You’ll also need to provide proof of your business registration, such as an Australian Business Number (ABN) or Australian Company Number (ACN), along with valid identification for all business owners or directors. Some lenders may ask for extra paperwork, like a business plan, a loan purpose statement, or details about any collateral you’re offering. By keeping these documents well-organized and readily available, you can avoid delays and improve your chances of getting approved.

Related Blog Posts

- The Truth About Business Loans in 2025

- IdeaFloat: The Tool That Made My Bank Say "Yes" to My Business Loan

- 50 Small Business Ideas in Australia for 2025 (Sorted by Start-Up Cost)

- Idea to Funding: The Documents Banks Actually Ask For