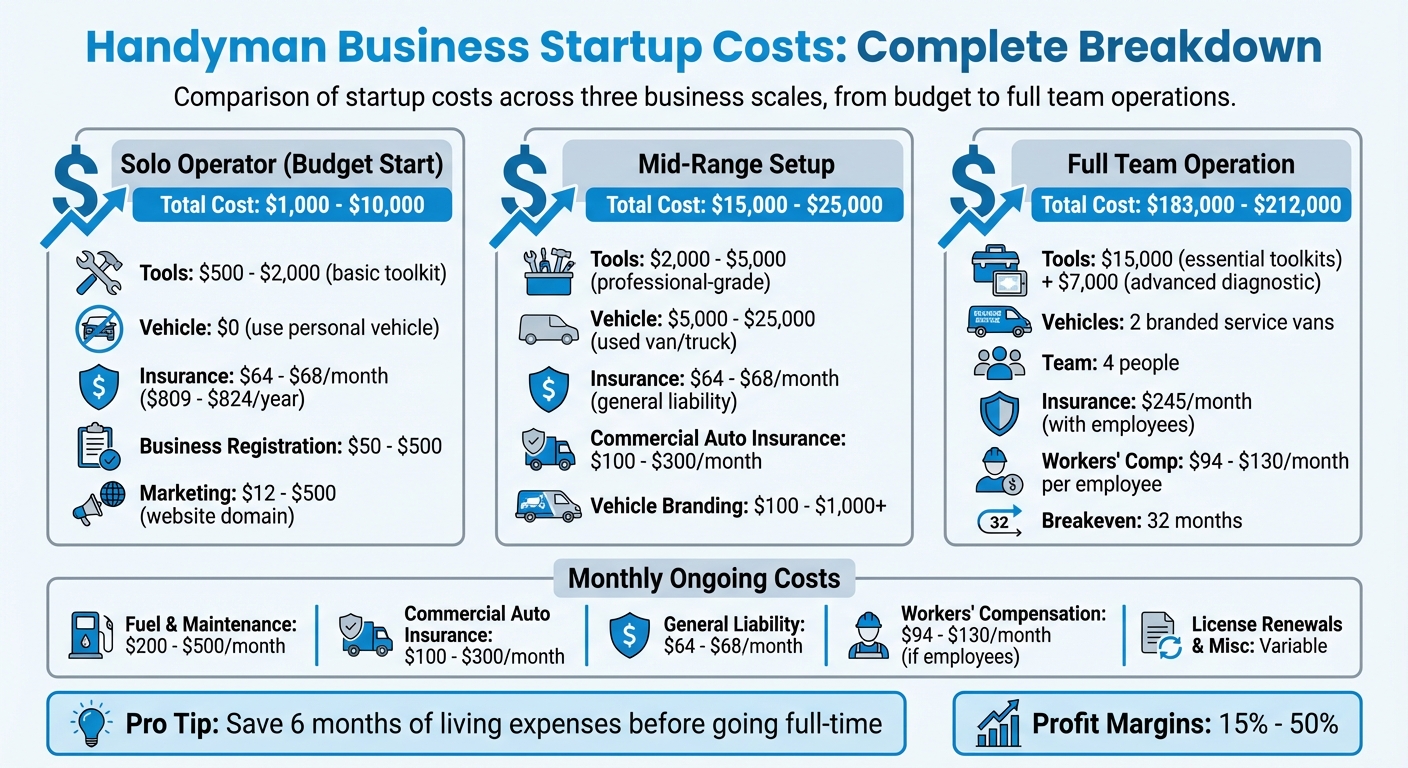

Starting a handyman business can cost anywhere from $1,000 to $10,000 for solo operators, or up to $212,000 for larger setups. The main expenses include tools, a reliable vehicle, and insurance. Here's a quick breakdown:

- Tools: Basic kits start at $2,000, while advanced setups can reach $15,000 or more. Start small and expand as needed.

- Vehicle: A used van or truck costs between $5,000 and $25,000. Branding and maintenance add to the budget.

- Insurance: General liability insurance costs $64–$68 monthly; other policies like workers' compensation or inland marine insurance may be required as your business grows.

Plan carefully to avoid overspending. Use your current vehicle, buy tools gradually, and budget for ongoing costs like fuel, insurance, and maintenance. A savings buffer of six months' living expenses can also ease the transition into full-time operations.

Handyman Business Startup Costs Breakdown by Business Size

The Freedom of being a Handyman and WHAT IT COSTS / Handyman Startup

Tools and Equipment Costs

The tools you invest in play a big role in shaping the services you can provide and how quickly your business can grow. If you're starting out as a solo handyman, you can kick things off with a basic toolset for less than $2,000. On the other hand, if you're managing a team of technicians, you might need to allocate around $15,000 for essential toolkits and an additional $7,000 for advanced diagnostic tools.

"I think that you could buy enough tools to get started for less than $2,000 and then buy new tools as you go."

– Dan Perry, Founder, Handyman Startup

A practical way to start is by focusing on the essentials - items like a drill, impact driver, tape measure, level, stud finder, and hammer. From there, adopt a "buy as you go" strategy, only purchasing additional tools when a specific job requires them. This approach keeps your upfront costs manageable and ensures you’re not wasting money on tools that gather dust.

Basic Tool List and Prices

Beyond the core tools, there are other essentials you’ll need to handle a variety of jobs. For instance, a 3-step aluminum ladder costs around $289, while a basic drywall kit - including a T-square and knives ranging from 2 to 12 inches - will set you back a bit more. Plumbing tools like pipe wrenches and a toilet auger are also must-haves. Don’t forget soft tools like drop cloths, moving blankets, and cleaning supplies to keep job sites tidy.

Here’s a breakdown of typical tool costs:

- Hammer: About $49

- Wrench sets: Around $79

- Cordless drills: Approximately $159

- Nail guns: Close to $264

- Air tool starter kits with compressor: Roughly $209

- Basic power sanders: Around $59

You’ll also need consumables like WD40, PVC glue, wood glue, and other maintenance supplies to keep your tools and projects running smoothly.

| Tool Category | Essential Items | Estimated Cost |

|---|---|---|

| Core Power Tools | Drill, impact driver, power sander | $159 - $264 each |

| Hand Tools | Hammer, wrench set, pliers, tape measure | $15 - $79 |

| Ladders | 3-step aluminum, telescoping extension | $289+ |

| Drywall Kit | T-square, knives (2"-12"), mud pan, texture hopper | $100 - $300 |

| Specialized Gear | Airless sprayer, tile saw, diagnostic sensors | $7,000 for advanced kits |

When to Buy Professional-Grade Equipment

Investing in professional-grade tools is worth it for items you’ll use frequently, like power drills, impact drivers, and precision tools such as levels. These tools directly impact the quality and durability of your work.

"Investing in high-quality instruments is always a good idea since they will perform better and last longer... especially when purchasing a power drill or other gear you will use on practically every task."

– Lily Bridgers

For tools you’ll use less often, renting or opting for budget-friendly versions can save you money. However, some professionals, like Bruce Williams of Northern Lights Renovations, prefer owning tools to avoid the hassle of renting:

"Personally I would rather buy a tool than rent it, primarily because the time needed to run around and find one for rent is often excessive."

– Bruce Williams, Northern Lights Renovations and Handyman Services

For bulky or rarely used equipment, such as gypsum board lifters, renting is a smarter option unless you find yourself needing them regularly.

How to Budget for Tools

Your tool budget should align with your niche - whether it’s plumbing, electrical work, carpentry, or general repairs. Start with the basics that allow you to take on your first jobs and expand your collection as your revenue grows.

Consider buying used equipment for tools that aren’t critical and negotiating bulk discounts if you’re outfitting a team. Don’t overlook storage solutions like tool cabinets, buckets, and plastic containers to keep your gear organized and easy to transport. Once you’ve planned your tool budget, the next step is choosing a reliable vehicle for your operations.

Vehicle Costs and Requirements

Your work vehicle isn't just a means of transportation - it's also a rolling advertisement for your business. It helps you keep tools organized, stay on schedule, and make a professional impression when parked in a client's driveway.

Picking the Right Vehicle

Trucks and vans are popular choices because they provide plenty of space for everything you need - hand tools, bulky equipment like water heaters or AC units, ladders, safety gear, and materials. Plus, they allow for better organization, so you can grab what you need without wasting time searching. When selecting a vehicle, reliability is key. A breakdown doesn't just mean repair costs; it can also lead to missed appointments and lost income.

If a van isn't an option right away, consider a 7x14' enclosed trailer. It offers extra standing room and storage but can be tricky to navigate in tight residential areas.

"I would recommend starting with whatever vehicle you have right now, get up and running, and if things are going well then get a truck."

– Dan Perry, Founder, Handyman Startup

For startups, a used work vehicle is usually the smarter choice, costing between $5,000 and $25,000. It avoids the high monthly payments of a new truck, which can strain a fledgling business. If a van or truck is out of reach, pairing your current vehicle with a cargo trailer can be a budget-friendly solution for securing and transporting tools.

Once you have your vehicle, it's time to factor in the ongoing costs that will impact your monthly budget.

Purchase Price and Monthly Expenses

The costs of owning and operating a work vehicle don't stop at the purchase price. Commercial auto insurance is a must, as personal policies typically don’t cover accidents that occur while hauling tools or driving between job sites. On average, this type of insurance costs $179 per month, though rates vary by state - Texas averages about $57 per month, while California tends to be closer to $72.

Fuel and maintenance are other major expenses. If you’re driving 15,000 miles annually in a pickup truck, expect to spend approximately $2,676 on fuel and $1,703 on maintenance and repairs each year. Monthly, this typically adds up to $200 to $500. Tracking your mileage is also crucial for maximizing tax deductions.

To turn your vehicle into a marketing tool, consider branding it with your business name and contact information. A full vehicle wrap can cost over $1,000, but you can start small with decals or magnetic signs for as little as $100. Keep the design simple and easy to read from a distance, making sure your phone number stands out. A branded vehicle not only builds local recognition but also makes it easy for potential clients to reach out after seeing your work.

| Expense Category | Initial Cost | Monthly Cost |

|---|---|---|

| Used Work Vehicle | $5,000 – $25,000 | - |

| Commercial Auto Insurance | - | $100 – $300 |

| Fuel & Maintenance | - | $200 – $500 |

| Vehicle Branding | $100 – $1,000+ | - |

sbb-itb-08dd11e

Insurance Costs and Coverage

Insurance is your safety net, shielding your business from unexpected accidents and lawsuits. For most commercial clients and property managers, having proof of insurance isn’t just a bonus - it’s a requirement before any work begins. That means insurance should be part of your startup budget from day one.

General Liability Insurance

General liability insurance is a must-have for any handyman. It protects you from third-party claims, like bodily injuries, property damage, or even defamation. For example, if a ladder accidentally damages a client’s property or someone gets injured on-site, this policy covers legal fees and settlements.

Most clients expect a coverage limit of $1 million per occurrence. If you’re a solo operator, you can expect to pay between $64 and $68 per month (about $809 to $824 annually). However, as your business grows - for instance, if you add two employees and generate $300,000 in revenue - your monthly premium might jump to around $245. Factors like the type of work you do (riskier jobs like roofing or electrical work cost more), your location, claims history, and team size all influence your premium. For instance, in states like California and New York, monthly premiums can average $273 and $286, respectively.

Other Insurance You May Need

In addition to general liability, you might need other policies to fully protect your business:

- Workers' compensation: If you hire employees, most states require this coverage. It pays for medical bills and lost wages for work-related injuries. Not having it can result in fines of up to $10,000 per employee, criminal charges, or even license suspension. Monthly costs typically range between $94 and $130.

- Inland marine insurance: This covers your tools against theft or damage while in transit or at a job site. For smaller handyman businesses, monthly premiums usually fall between $14 and $17. Choosing replacement cost coverage ensures you can replace tools at their full value.

- Professional liability insurance: Also known as errors and omissions insurance, this covers claims of poor workmanship or mistakes that lead to a client’s financial loss. This policy averages around $54 per month. Many handymen bundle it with commercial property insurance in a Business Owner’s Policy (BOP), which costs between $90 and $93 per month. Bundling policies can save you 17% to 25% compared to purchasing them individually.

"Handymen transporting tools to job sites must carry commercial auto insurance or face fines, license suspension and personal liability for all accident costs."

– MoneyGeek

Total Costs and Budget Planning

Now that we've covered tools, vehicles, and insurance, let’s bring it all together by outlining your total startup costs and how to plan your budget effectively.

Total Startup Cost Estimate

If you're a solo operator using your personal vehicle and a basic toolkit, your startup costs will likely fall between $1,000 and $10,000. This range includes key expenses like:

- Business registration: Approximately $50 to $500

- General liability insurance: Around $300 to $1,000 annually

- Initial toolkit: Between $500 and $2,000

- Basic marketing efforts: Securing a website domain can cost $12 to $500

For those aiming for a mid-range setup with a used service vehicle and professional-grade tools, expect to spend $15,000 to $25,000. On the higher end, launching a more robust operation - such as a four-person team with two branded service vans and custom mobile apps - can cost $183,000 to $212,000, with a breakeven point typically around 32 months.

If you're starting out solo, there are several ways to keep your initial costs in check.

How to Cut Costs as a Solo Operator

Begin by using your personal vehicle instead of rushing to purchase a service van, which could cost $35,000 or more. Invest in essential tools you'll use frequently, and consider renting specialized equipment for occasional jobs.

Working out of a home office or garage can save you from paying commercial rents, which can reach up to $2,500 per month. For marketing, stick to free platforms like Google My Business, Yelp, and word-of-mouth referrals. You can also find quality used tools on online marketplaces, significantly reducing your upfront equipment costs.

Planning for Future Expenses

As your business grows, having a contingency fund is crucial for unexpected expenses like emergency vehicle repairs or sudden equipment price hikes. You’ll also need to budget for recurring costs, such as:

- License renewals, insurance, and vehicle maintenance: Typically $200 to $500 monthly

- Taxes: Set aside 15% of every payment for state and federal taxes

Instead of buying all your tools at once, upgrade your equipment gradually based on demand. Before transitioning to full-time operations, aim to have at least six months’ worth of living expenses in savings. Using accounting software can also make a big difference - it helps you track cash flow, manage expenses, and spot areas where you can save money without compromising service quality.

Conclusion

What You Need to Remember

Let’s wrap up with the most important points from our cost breakdown. Every expense - whether it’s for tools, vehicles, or insurance - plays a crucial part in shaping your startup budget. Depending on the scale of your operation, initial costs can range from around $2,000 for a solo entrepreneur to over $180,000 for a larger setup with a fleet and a mobile app. Align your spending with your business model to keep your finances on solid ground.

Insurance is a must-have safety net. With general liability coverage costing between $361 and $792 annually, it protects your business from hefty financial risks. As the ZenBusiness Editorial Team puts it, "Insurance isn't just an added expense for small business owners - it's a vital shield against unforeseen mishaps".

Your vehicle will likely be your biggest investment. Taking a phased approach to this purchase can help you conserve cash during those critical early months when you’re still building a steady client base.

"The primary reason for most businesses' failure isn't their lack of hands-on skill, but rather the inability to make sound business decisions." - TRUiC

Lastly, think beyond day one. Budget for ongoing costs, unexpected repairs, and make sure to keep your business finances separate. With profit margins typically falling between 15% and 50%, careful financial planning is key to long-term success. Focus on making smart, step-by-step investments to set your business up for steady growth.

FAQs

What tools do I need to start a handyman business?

To kick off a handyman business, having the right tools is key to tackling a variety of repair and maintenance jobs. Here's an overview of the must-haves:

- Hand tools: Stock up on essentials like a hammer, flat and Phillips-head screwdrivers, pliers, adjustable wrenches, a 25-foot tape measure, a level, and a utility knife. These will handle most basic tasks.

- Power tools: Equip yourself with a cordless drill and bits, a circular saw, a reciprocating saw, and a jigsaw. These tools are great for cutting through materials like wood and drywall.

- Plumbing tools: For plumbing repairs, you'll need a pipe wrench, pipe cutter, plumber’s snake, and basin wrenches to handle tasks like fixing faucets or unclogging drains.

- Electrical tools: Keep a voltage tester, wire strippers, a multimeter, and insulated screwdrivers on hand for electrical work.

- Finishing supplies: For touch-ups and finishing, have paintbrushes, rollers, drop cloths, sandpaper, and a putty knife ready to go.

Starting with durable, high-quality tools will not only help you handle a wide range of client requests but also set the foundation for a reliable and efficient business.

How can I minimize vehicle expenses when starting my handyman business?

To keep your vehicle expenses in check, start with a realistic budget. For a handyman business, transportation costs typically fall between $3,000 and $15,000, but sticking to the lower end of that range can free up funds for other essentials like tools and insurance.

Opt for a dependable, fuel-efficient vehicle that suits the type of jobs you’ll be handling. You don’t need to splurge on a brand-new truck or van - well-maintained used models can do the job just as effectively. When it comes to insurance, start with the basic liability coverage required and think about upgrading your policy only as your business begins to grow. By prioritizing practicality and focusing on what’s essential, you can keep your startup costs under control while ensuring you have a reliable vehicle to get the job done.

Why is having insurance important when starting a handyman business?

Insurance plays a crucial role in running a handyman business, offering protection against unexpected expenses that can arise from accidents or damages. Imagine accidentally damaging a client’s property during a job or someone getting injured - insurance steps in to cover those costs, sparing your business from potentially overwhelming financial setbacks.

Beyond financial protection, having the right policies, like general liability insurance or coverage for tools and equipment, boosts client confidence and ensures your business meets legal and professional standards. It’s a practical way to safeguard your livelihood while giving you the confidence to focus on growing your business.

Related Blog Posts

Get the newest tips and tricks of starting your business!