Did you know poor financial planning is a top reason 20% of small businesses fail in their first year? Calculating start-up costs accurately is key to avoiding this pitfall and ensuring your business is set up for success. Here's a quick overview of how to estimate your start-up costs:

- List All Expenses: Include one-time costs (e.g., equipment, permits) and recurring costs (e.g., rent, salaries).

- Categorize Costs: Break them into fixed (e.g., office rent), variable (e.g., inventory), mandatory (e.g., licenses), and optional (e.g., extra software).

- Estimate Accurately: Use tools like start-up cost calculators, industry benchmarks, or consult experts.

- Add a Buffer: Reserve 15-20% of your budget for unexpected expenses.

- Calculate Total Costs: Combine one-time and first-year recurring costs to determine funding needs.

Pro Tip: Many start-up costs are tax-deductible, so consult a tax professional to maximize savings.

This guide will walk you through each step, helping you create a solid financial plan for your business.

How To Calculate Startup Costs

Step 1: Listing Your Start-Up Expenses

Making a detailed list of start-up expenses is a key part of financial planning. This step helps you estimate costs accurately and ensures you don’t miss anything important.

Sorting Expenses

Break down your expenses into two main categories to prioritize spending and maintain financial stability:

| Expense Type | Examples | Typical Timing |

|---|---|---|

| One-Time Costs | Equipment, logo design, permits | Before or at launch |

| Recurring Costs | Salaries, utilities, marketing | Monthly/ongoing |

Using an expense tracking system can keep your financial records organized and ensure you don’t overlook important costs [5].

Key Expense Categories

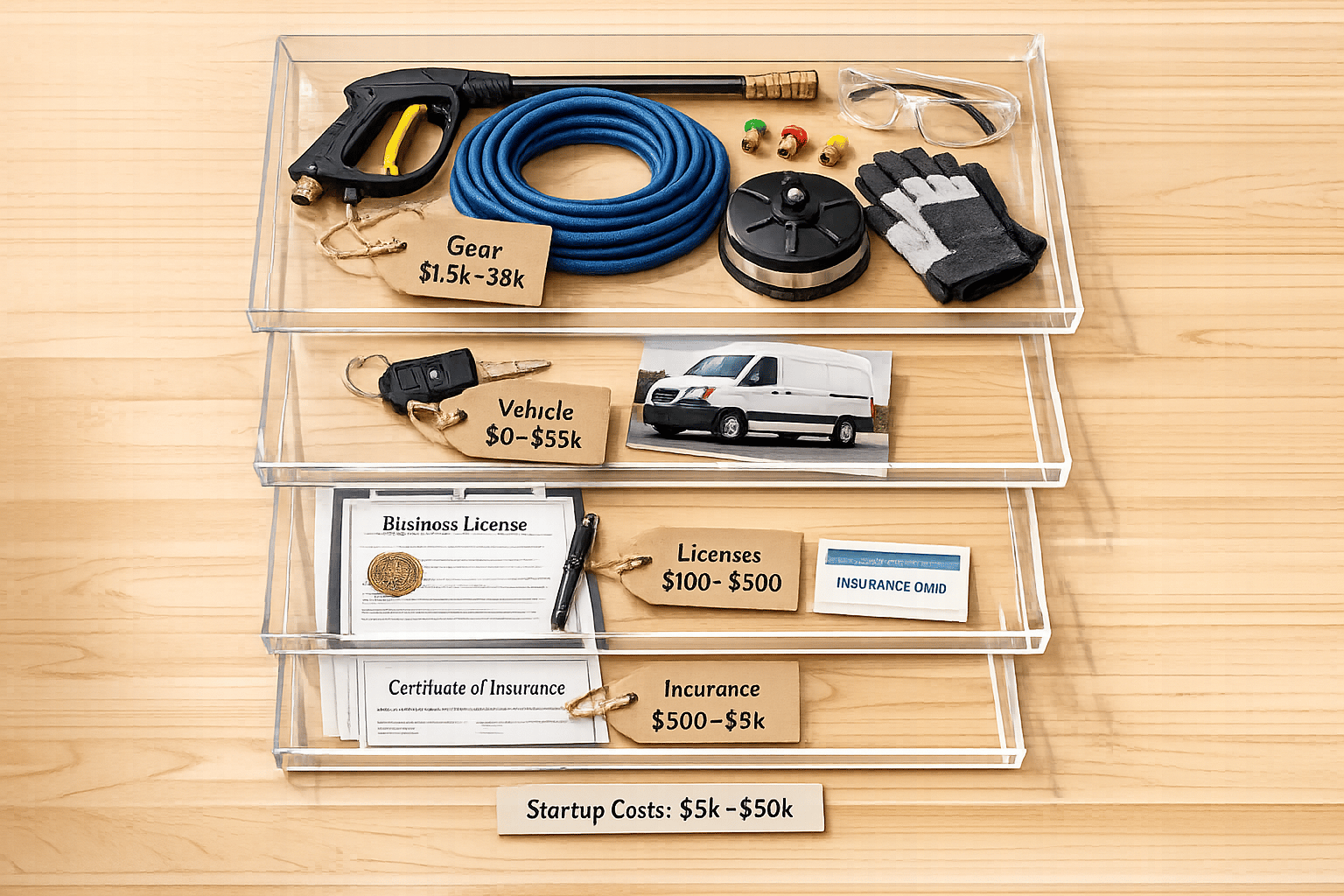

Start-up costs often fall into these categories:

| Category | Common Expenses | Estimated Range |

|---|---|---|

| Equipment & Assets | Machinery, computers, furniture | $2,000 - $50,000 |

| Legal & Permits | Business licenses, registrations | $500 - $5,000 |

| Marketing | Website, advertising, branding | $1,000 - $10,000 |

| Operations | Rent, utilities, insurance | $1,500 - $15,000/month |

| Staffing | Salaries, training, benefits | $3,000 - $20,000/month |

These ranges can vary widely depending on your industry, location, and the size of your business [5].

Research and Expert Advice

To make accurate estimates, research industry standards, consult professionals, and check local prices for key services and supplies. The Small Business Administration (SBA) offers helpful tools and guides to identify expenses specific to your industry [3].

Once your expenses are listed and categorized, the next step is estimating and organizing them to get a clearer financial overview.

Step 2: Estimating and Sorting Costs

Once you've listed your expenses in Step 1, it's time to estimate and organize them. Digital tools can make this process smoother by providing templates and benchmarks to refine your financial projections.

Using Start-Up Cost Calculators

Start-up cost calculators are handy for streamlining your estimates. Here's how they help:

| Feature | How It Helps |

|---|---|

| Cost Templates | Ensures no important expenses are missed |

| Industry Benchmarks | Validates your estimates against standards |

| Financial Projections | Guides planning for growth and scaling |

For instance, IdeaFloat uses AI to provide insights for cost analysis. Meanwhile, Upwork's Startup Cost Calculator offers templates tailored to freelancers and small businesses [1].

Sorting Costs into Categories

Organizing your costs into categories makes tracking easier. Keep these categories in mind and update your estimates as new data or market changes occur:

| Cost Type | Examples |

|---|---|

| Fixed Costs | Office rent, equipment leases |

| Variable Costs | Inventory, marketing campaigns |

| Mandatory Expenses | Licenses, permits, insurance |

| Optional Expenses | Premium office furniture, additional software |

Avoiding Overlooked Costs

Some costs are easy to miss. Here’s how to stay prepared:

- Account for recurring expenses like insurance premiums and tax filings, which continue after your business is set up.

- Reserve 15-20% of your budget for unexpected costs.

- Don’t forget about website hosting, software subscriptions, and maintenance fees [1][2].

With your costs estimated and sorted, you're ready to calculate the total and make room for any surprises.

Step 3: Calculating Total Start-Up Costs

With your expenses organized, it's time to figure out your total start-up costs. This step helps you understand how much funding you'll need and allows you to build a realistic budget for your business.

Combining One-Time and Recurring Costs

Start by adding up all one-time expenses, such as equipment or legal fees, and then include recurring costs like rent, utilities, and salaries. For recurring expenses, multiply the monthly amount by 12 to estimate your first-year budget. Here's a simple breakdown:

| Cost Type | Time Frame | Examples |

|---|---|---|

| One-Time Costs | Initial Investment | Equipment, legal fees |

| Recurring Costs | First 12 Months | Rent, utilities, salaries |

| Operating Costs | Monthly Average | Marketing, inventory |

This structure ensures you don’t miss any key expenses.

Accounting for Unexpected Costs

It’s smart to prepare for surprises. Set aside 15-20% of your total budget for unexpected expenses, like equipment repairs, sudden market opportunities, or emergency needs. This cushion can save you from financial stress later.

Identifying Funding Needs

Once you know your total costs, compare them to your available resources. If there’s a gap, consider funding options based on your budget:

- Under $50,000: Personal savings or loans from friends and family might be enough.

- Over $250,000: You might need to explore small business loans, angel investors, or venture capital.

Keep in mind that many start-up expenses are tax-deductible. For larger purchases like equipment, deductions may need to be spread out over time rather than taken all at once [4].

With your total costs calculated, you’re ready to look into tools and resources that can help streamline this process and refine your estimates further.

sbb-itb-08dd11e

Step 4: Using Tools and Resources

Estimating start-up costs can be made much easier with the right technology. Once you've calculated your total costs, using tools can help fine-tune your estimates and simplify financial planning.

IdeaFloat: AI-Powered Start-Up Cost Tools

IdeaFloat provides AI-driven tools designed specifically for start-up cost analysis. It includes features like a cost generator, validation score, and business plan integration. These tools help ensure no expenses are missed, refine financial projections, and streamline planning.

| Feature | Purpose | Benefit |

|---|---|---|

| Cost Generator | Breaks down expenses in detail | Reduces the risk of missing costs |

| Validation Score | Evaluates financial projections | Highlights potential weak points |

| Business Plan Integration | Merges cost data with planning | Simplifies creating financial plans |

The platform offers a free version with basic features, while paid plans unlock advanced options.

Other Useful Platforms

If you're looking for alternatives, simple tools like spreadsheets can also be effective for tracking and managing costs:

- Spreadsheet Templates: Tools like Google Sheets and Excel allow manual tracking and customization, making them a good choice for businesses with straightforward expenses [5].

- Centralized Procurement Systems: These systems help manage and track expenses methodically, ensuring accurate records across vendors and categories [5].

When selecting tools, consider:

- Ease of use: Pick something that matches your comfort level with technology.

- Integration options: Check if the tool works with your current software.

- Affordability: Explore both free and paid solutions to find what fits your budget.

Once you've fine-tuned your cost estimates, you can incorporate them into your business plan to guide your operations and attract investors.

Step 5: Integrating Start-Up Cost Estimates into Your Business Plan

Now that you've fine-tuned your cost estimates using various tools and resources, it's time to incorporate these numbers into your business plan. This step is crucial for creating a clear financial framework that guides your business decisions.

Building a Clear Business Plan

Your start-up cost estimates are the financial backbone of your business plan. They show stakeholders that you've carefully planned for all necessary expenses. Break down your costs into categories like one-time expenses, recurring costs, and variable expenses, and outline these in your plan with specific considerations. Don't forget to account for taxes and include a buffer for unexpected costs.

| Cost Category | Planning Consideration |

|---|---|

| One-Time Expenses | Add to initial funding requirements |

| Recurring Costs | Incorporate into monthly cash flow planning |

| Variable Expenses | Adjust based on projected sales performance |

Developing Financial Projections

These cost estimates also serve as the foundation for your financial projections. Use them to create essential documents like cash flow forecasts, break-even analyses, and profit and loss statements. These tools will help you map out your business's financial path.

If projections feel complex, consider using financial software or consulting with a professional advisor. This ensures your numbers align with industry norms and meet regulatory expectations. Update these projections regularly to stay accurate as market conditions shift.

Keep your projections grounded in reality. While optimism has its place, conservative estimates often resonate better with investors and lenders. Back up your numbers with market research, industry data, and the detailed cost breakdowns from your earlier work [5].

Conclusion: Turning Cost Estimates into Action

With the right tools and resources in place, the next step is to turn your cost estimates into actionable strategies that drive your business forward.

Key Takeaways and Steps to Follow

Accurate cost estimation lays the groundwork for smart business decisions and financial health. According to the U.S. Small Business Administration, businesses with detailed cost estimates are 40% more likely to secure funding and grow successfully [3].

Research also shows that companies keeping their cost projections up to date are three times more likely to maintain a steady cash flow during their first year [5]. This highlights the need to treat your estimates as evolving documents that grow with your business.

Here’s how to get the most out of your cost estimates:

- Document every expense carefully. Missing details can throw off your entire budget.

- Include a contingency buffer. This helps you prepare for unexpected costs (as discussed earlier).

- Consult professionals. Validation from experts can strengthen your estimates.

- Review and update quarterly. Adjust for market changes and stay on track.

Your cost estimates are more than just a budgeting tool. They can:

- Inform strategic decisions

- Boost investor confidence

- Strengthen funding applications

- Help you stay ahead of financial challenges

Regularly reviewing and adjusting your estimates is essential. Entrepreneurs who update their projections every quarter are better prepared to adapt to shifts in the market and maintain financial stability. Use these estimates to guide your decisions and secure the resources you need.

As you move forward, focus on turning these numbers into actionable steps. Start small, but keep your long-term goals in mind. Treat your cost estimates as dynamic tools that help you navigate the challenges of running and growing your business.

FAQs

How do I calculate start-up costs?

The U.S. Small Business Administration suggests following these steps to calculate your start-up costs:

- List all necessary expenses, such as rent, equipment, legal fees, inventory, salaries, and marketing.

- Separate these expenses into one-time costs (e.g., equipment) and recurring costs (e.g., rent).

- Refine your estimates using industry reports, local market research, and online tools.

It's smart to add a 15-20% buffer for unexpected costs.

What start-up costs are often overlooked?

Some start-up expenses can slip through the cracks, including:

- Employee training programs

- Professional services like accounting or legal help

- Insurance policies

- Software subscriptions

- Website hosting and upkeep

- Business permits and licenses

- Utility setup fees or deposits

How much should I set aside for start-up costs?

The amount you'll need depends on your business type [5]:

- Small service-based business: $2,000 - $10,000

- Retail store: $50,000 - $150,000

- Tech startup: $150,000 - $500,000

Certain start-up expenses, such as capital investments, might qualify for federal tax deductions over time [4]. Check with a tax expert to see which costs are eligible.

For more detailed guidance and tools to help calculate your start-up costs, revisit earlier sections of this guide.

Related Blog Posts

Get the newest tips and tricks of starting your business!