Want to impress a bank with your business plan? Keep it short and clear. A 1-page business plan focuses on the essentials: what your business does, who your customers are, how you'll make money, and how you'll repay a loan. Banks don’t want to sift through long, jargon-filled documents - they need simple, actionable information.

Here’s what your 1-page plan should include:

- Business Summary: A clear, concise description of your business and what sets it apart.

- Market Analysis: Define your audience, highlight competitor gaps, and explain your market opportunity.

- Financial Overview: Outline revenue streams, expenses, and realistic projections.

- Funding Request: Specify the amount needed, how it’ll be used, and your repayment plan.

This format is faster to create (15–30 minutes) and more likely to be read by lenders. Plus, businesses that plan grow 30% faster. Use tools like templates or generators to ensure your plan is professional and easy to understand.

The bottom line: A 1-page business plan saves time, communicates effectively, and increases your chances of securing funding.

How to Write a One Page Business Plan

What Banks Want to See in Your 1-Page Business Plan

When it comes to securing a loan, banks are all about the numbers and your ability to repay. They’re not interested in flowery language or abstract ideas. Instead, your 1-page business plan needs to address four essential questions: What does your business do? Why will customers pay for it? How much money do you need? And how will you repay the loan? Every answer should be backed by solid research - bankers can easily spot unrealistic projections.

The format of your plan is just as important as the content. Stick to bullet points, short paragraphs, and simple visuals to make your case clear and easy to follow. Here's how to structure a bank-ready plan.

Business Summary

Think of your business summary as a quick, written elevator pitch. In just two or three sentences, explain your business model and the specific problem you’re solving . Avoid vague descriptions. Instead of saying, "We serve busy professionals", try something like this:

"Dual-income homeowners, ages 35–65, with household incomes over $150,000, need healthy lunch options with under 10-minute pickup times" .

"Think of it as your business's elevator pitch in written form. Instead of drowning readers in details, you're giving them the essential information they need to understand and believe in your business." - Homebase

Also, highlight what sets you apart from competitors. Whether it’s a unique product, better pricing, or specialized expertise, make it clear why your business stands out . Don’t forget to mention your management team’s relevant experience to show you have the skills to execute your plan.

Market Analysis and Opportunity

After the business summary, show that you’ve done your homework on the market. Define your target audience using specifics like age, income, location, and buying habits . Steer clear of claiming “everyone” as your market; a narrow, well-defined focus is far more credible.

For instance, if you’re opening a coffee shop, cite local foot traffic data or competitor sales figures. Keep your competitive analysis focused - highlight two or three direct competitors and their weaknesses. For example:

- "Competitor A closes at 3 PM, leaving no late-afternoon options."

- "Competitor B uses outdated ordering technology that frustrates customers."

"Start your pitch with the demand in your market, not how big the market is. It doesn't matter how big the market is if no one wants your product or service." - Sweta Patel, Forbes Business Council

Financial Overview and Projections

This section is where you build trust by showing you understand the numbers. Start by explaining your revenue streams - whether it’s product sales, services, or subscriptions - and outline your pricing structure . Then, break down your costs into fixed expenses (like rent and salaries) and variable expenses (like materials and marketing).

If your business is already up and running, include three years of financial statements, such as income statements, balance sheets, and cash flow statements. If you’re investing your own money, mention it - it shows you’re committed.

| Financial Metric | What to Include |

|---|---|

| Startup Costs | Total capital needed for equipment, inventory, and initial marketing |

| Revenue Projections | Estimated sales for Year 1, broken down by month or quarter |

| Monthly Expenses | Combined fixed and variable costs to keep operations running |

| Break-Even Point | Timeline or sales target to reach zero net loss |

| Monthly Cash Flow | Net income after expenses, showing repayment ability |

Funding Request and Repayment Plan

Once your financials are solid, explain exactly how much money you need and how you’ll use it. Be specific. For example:

"Requesting a $50,000 loan to purchase commercial kitchen equipment ($35,000) and fund initial inventory and marketing ($15,000)."

Your repayment plan should clearly outline how you’ll pay back the loan. Show how your projected cash flow supports repayment. For instance, if your net profit is $4,200 and your loan payment is $1,100, that leaves a comfortable margin. Add a timeline with key milestones, like:

"By June 2026, the lease will be signed and equipment installed; by September 2026, we'll reach $15,000 in monthly revenue."

This level of detail shows the bank you’ve thought through every step of your business model and can execute it effectively.

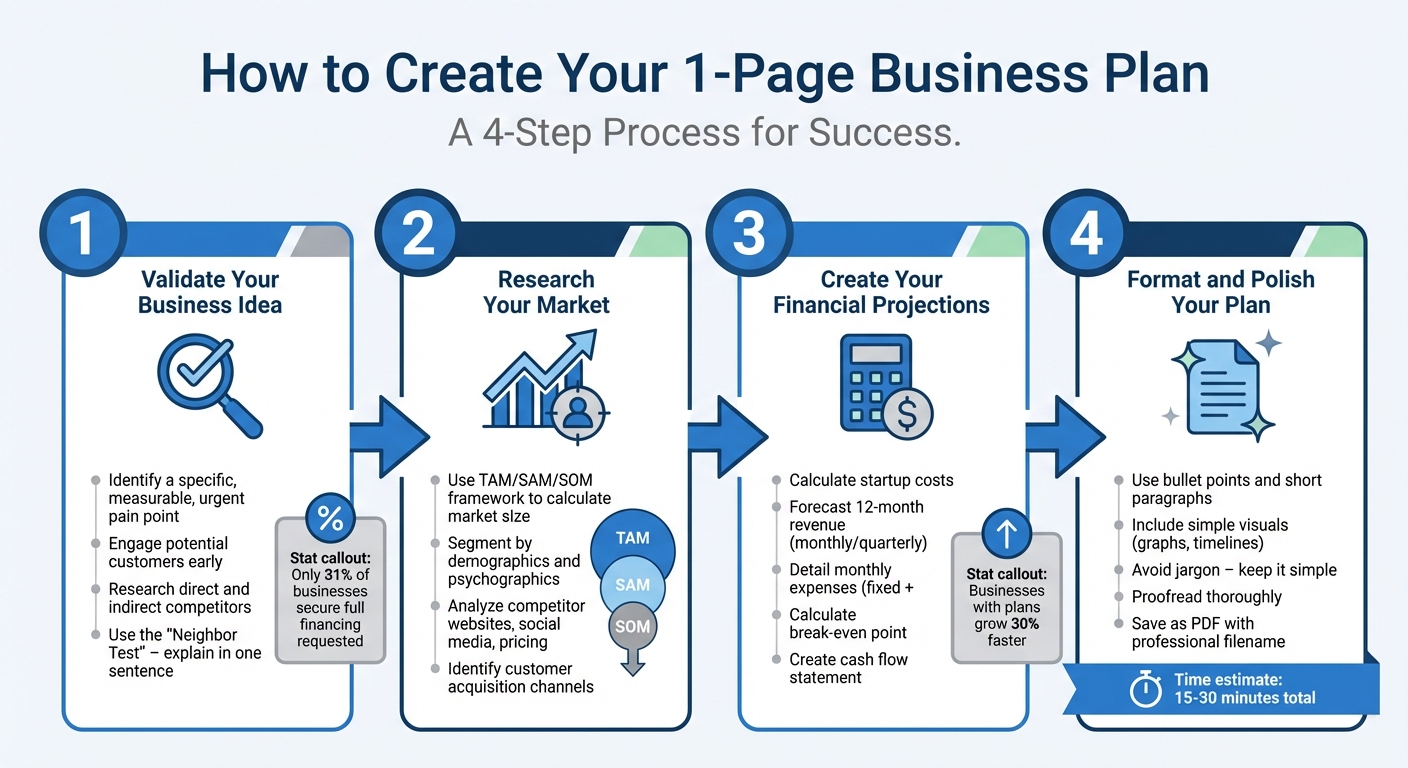

How to Create Your 1-Page Business Plan

4-Step Process to Create a Bank-Ready 1-Page Business Plan

To craft a 1-page business plan that meets lender expectations, follow a structured approach. Start by validating your idea, then dive into market research and financial planning, and finally, polish your document into a professional, concise plan. Each step builds on the last, so take your time to create a plan that stands out.

Step 1: Validate Your Business Idea

Before anything else, make sure your idea addresses a real and pressing problem. Banks can easily spot vague or untested ideas, and only 31% of businesses secure the full financing they request. Avoid becoming part of that statistic by thoroughly validating your concept.

Identify a specific, measurable, and urgent pain point. Broad issues like "saving time" won’t cut it. Instead, refine your problem. Take Perfect Lawns, for example. Initially, they thought their customers’ problem was "time wasted on yard work." After validation, they reframed it as "unkempt lawns reducing property value and creating HOA conflicts." This sharper focus allowed them to offer a targeted solution - a "curb appeal guarantee".

"The biggest mistake you can make when writing a business plan is creating one before the idea has been adequately researched and tested." - Bank of America

Engage potential customers early. Ask them about their challenges and whether they’d pay for your solution. Test your idea with a pilot program to confirm its viability.

Look into your competition. Identify direct competitors offering similar products and indirect competitors solving the same problem differently. For example, a taco stand competes indirectly with a hot dog vendor because both address hunger.

Finally, focus on a specific customer group. Use the "Neighbor Test": if you can’t explain your problem and solution in one sentence to a neighbor, simplify it.

With a validated idea in hand, you’re ready to analyze your market.

Step 2: Research Your Market

Show lenders that your business has a solid market foundation. Combine primary research (talking to real customers) with secondary research (studying competitors and industry trends).

Use the TAM/SAM/SOM framework to calculate your market size:

- TAM (Total Addressable Market): The total revenue opportunity if you captured 100% of the market.

- SAM (Serviceable Addressable Market): The portion of TAM you can realistically reach based on your business model and resources.

- SOM (Serviceable Obtainable Market): The slice of SAM you can capture in your first year, factoring in competition and your marketing budget.

For example, if you’re opening a coffee shop in a city with 500,000 residents, your TAM might include all local coffee drinkers. Your SAM could be the 50,000 people within a 2-mile radius of your shop, and your SOM might be the 2,500 customers you expect to attract in your first year.

Segment your market by demographics and psychographics. Instead of saying "busy professionals", get specific: "dual-income homeowners, ages 35–65, earning over $150,000 annually, looking for healthy lunch options with under 10-minute pickup times".

Research competitors by analyzing their websites, social media, and pricing. Look for gaps in their offerings. For instance, if a competitor closes at 3 PM, position yourself as the late-afternoon option.

Also, outline how you’ll reach your customers. Identify where they spend their time - whether it’s Instagram, local events, or trade shows - and detail your plan to acquire them.

Step 3: Create Your Financial Projections

Build lender confidence by showing you’ve nailed down the numbers. Start by calculating your startup costs - everything from equipment and inventory to licenses and marketing. For example, Perfect Lawns estimated $10,000 in startup costs, covered by personal savings, for a commercial mower and trailer.

Forecast your revenue for the first 12 months, breaking it down monthly or quarterly. Use real data to back up your projections. For instance, if competitors charge $50 per hour for a similar service, use that as a baseline. Perfect Lawns projected $10,000 in monthly revenue based on 50 clients at $200 each.

Detail your monthly expenses, separating fixed costs (like rent and salaries) from variable ones (materials and marketing). Perfect Lawns listed monthly costs as follows: Labor $4,000; Equipment $1,000; Marketing $500; Insurance/Overhead $1,500.

Calculate your break-even point, the moment when your revenue matches your expenses. For example: "We’ll break even in Month 8 when we reach $7,000 in monthly revenue".

"A realistic guess beats a blank space every time." - Homebase Team

Create a cash flow statement showing your monthly bank balance over 12 months. This demonstrates your ability to repay a loan. For instance, if your monthly net profit is $3,000 and your loan payment is $1,100, you’re in good shape. Clearly state your assumptions, like "based on competitor pricing of $50/hour", to build credibility.

If you’re investing your own money, mention it. Lenders want to know you’re committed. Also, keep in mind that business founders who write a plan grow their companies 30% faster than those who don’t.

With your financials in order, it’s time to present your plan effectively.

Step 4: Format and Polish Your Plan

Make your plan easy to read and professional. Lenders review dozens of plans, so clarity is key.

Use bullet points and short paragraphs to present information clearly. Replace full spreadsheets with concise summaries that highlight key figures.

Include simple visuals like bar graphs for revenue projections or a timeline for milestones. For example, you could show a graph of your projected revenue growth over 12 months or a timeline noting milestones like "June 2026: Lease signed and equipment installed; September 2026: Reach $15,000 in monthly revenue".

Avoid jargon. If your neighbor wouldn’t understand a term, simplify it. Replace vague phrases like "We serve busy professionals" with specifics such as "We serve dual-income homeowners, ages 35–65, earning over $150,000 annually".

Proofread thoroughly to catch typos or formatting errors. Have someone with business or finance experience review it for additional feedback.

Save your plan as a PDF to preserve formatting when sending it to lenders. Use a professional file name like "YourBusinessName_BusinessPlan_Jan2026.pdf" to show you’re organized and serious about your venture.

sbb-itb-08dd11e

Free 1-Page Business Plan Template

The Business Plan Generator from IdeaFloat takes your market research, financial data, and strategy, and transforms them into a professional, lender-ready business plan. Forget the hassle of spreadsheets - the tool organizes verified data from your workspace into the five key sections banks prioritize. Below is a breakdown of what the template includes and how you can tailor it to fit your business.

What's Included in the Template

This template focuses on the critical components lenders evaluate when assessing loan applications:

- Business Summary: Highlights your business identity, the problem you're tackling, and your solution.

- Market Validation: Details your target customer demographics, market size (TAM/SAM/SOM), and a competitive analysis.

- Go-to-Market Strategy: Explains your customer acquisition channels, marketing methods, and conversion plans.

- Financial Overview: Provides a snapshot of your revenue streams, key expenses, and profit margins.

- Funding Request: Specifies the amount you’re seeking, how it will be allocated, and your repayment plan.

These sections align with the bank requirements discussed earlier, making it easy for lenders to review your plan efficiently.

How to Customize the Template

Once you’ve created your 1-page plan, you can personalize it further to align with your business. Start by reviewing the auto-filled sections to ensure the data matches your business model. Replace placeholder text with specific details about your company, including an updated problem statement that reflects your validated market insights.

For the Financial Overview, adjust the figures to reflect your actual startup costs and monthly expenses. If you’re seeking a loan, include interest as an expense in your profit and loss statement, and list the loan as a liability on your balance sheet. Update revenue projections based on your latest sales forecasts and double-check break-even analyses for accuracy.

Make the template visually appealing by incorporating your brand. Add your company logo, tweak the color scheme, and select professional fonts. When you’re done, export your plan as a PDF to maintain its formatting when sharing with lenders.

"Lean startup business plans... focus on summarizing only the most important points of the key elements of your plan. They can take as little as one hour to make and are typically only one page." - U.S. Small Business Administration

If your lender requests additional documentation, prepare an appendix with supplementary materials like credit histories, resumes, product images, letters of reference, or legal agreements.

Conclusion

Bringing together all the insights from your planning process, a 1-page business plan is your secret weapon when it comes to impressing lenders. Why? Because banks and investors are far more likely to review a concise, well-organized plan than sift through a 25- to 50-page document. This streamlined approach increases your chances of securing funding. By focusing on the essentials - like a sharp business summary, a clear market analysis, a practical financial outlook, and a specific funding request - you show lenders exactly what they need to see.

"Angel Investors are significantly more likely to read this one-page plan than they are a 25-page business plan." - Nikki Roser, President, My First Bank

This quote highlights the importance of clarity and precision. The way you present your business can make all the difference. A professional, lender-ready plan signals that you've done your homework, understand your audience, and have a feasible strategy to achieve profitability.

To make this process even easier, tools like IdeaFloat's Business Plan Generator can take your data and turn it into a polished, lender-friendly document in under 30 minutes. No need to wrestle with complex spreadsheets or formatting - this tool delivers profit and loss statements, cash flow forecasts, and balance sheets in SBA-approved formats.

Download the customizable template and get started. A focused, professional 1-page plan isn’t just a document - it’s your ticket to funding. Your idea deserves the spotlight, and this is how you make it shine.

FAQs

How can I make sure my business idea is solid before creating a 1-page plan?

Before jumping into your 1-page business plan, it’s smart to make sure your idea has real potential. Here’s how you can validate it:

- Assess feasibility: Estimate your target market size and figure out how many paying customers you’d need to break even. This will give you a sense of whether your idea can support a lasting business.

- Measure interest: Speak directly to potential customers through surveys, interviews, or social media polls. Ask about their pain points, how your solution could address them, and if they’d actually pay for it.

- Test the waters: Build a simple prototype or landing page and launch a small-scale test, such as pre-orders or ads. Monitor how many people show interest or make purchases to see if there’s genuine demand.

Taking these steps will give you a clearer picture of your market, customer interest, and potential sales. With this information in hand, you’ll be better prepared to create a polished, professional 1-page business plan that stands up to scrutiny.

What financial details should I include in my 1-page business plan to impress banks?

When crafting a 1-page business plan for banks, make sure to include straightforward financial projections. This means outlining your expected revenue, expenses, cash flow, and profit in a way that's easy to understand. Alongside this, add a clear funding request that details the loan amount you’re seeking, how you plan to use the money, and your proposed repayment terms.

Present this information in a professional and concise manner to show the viability of your business and instill confidence in potential lenders.

How can I make my 1-page business plan stand out by showcasing my market opportunity?

To make your 1-page business plan shine, focus on presenting a clear and engaging overview of your market opportunity. Emphasize the size of your target market, the specific problem your business addresses, and how your solution effectively meets this need in a way others don’t. Use concise, data-backed insights, and include a short statement about what sets your business apart to show why it’s primed for success. Keeping it straightforward yet impactful will appeal to banks and lenders who value clarity and practicality.

Related Blog Posts

Get the newest tips and tricks of starting your business!