Starting a consulting business involves managing costs that go beyond your expertise. Key expenses include insurance, software tools, and taxes. Here’s what you need to know:

- Insurance: General liability costs $22–$29/month, professional liability $55–$107/month, and a business owner’s policy $32–$42/month. Bundling can reduce costs.

- Software & Tools: CRM, analytics, and productivity software range from $20 to $150/month. Keep records for tax deductions.

- Taxes: Self-employment tax (15.3%) applies if net earnings exceed $400. Quarterly estimated payments are needed if you owe $1,000+ annually.

- Startup Costs: Deduct up to $5,000 in first-year expenses like legal fees and market research. Plan for a cash buffer to cover at least one year of operations.

Organize your expenses into one-time startup costs and recurring monthly overhead to calculate your breakeven point and ensure financial stability. Let’s dive into the details.

STOP Wasting Money on Unnecessary Startup Expenses for Your Consulting Business

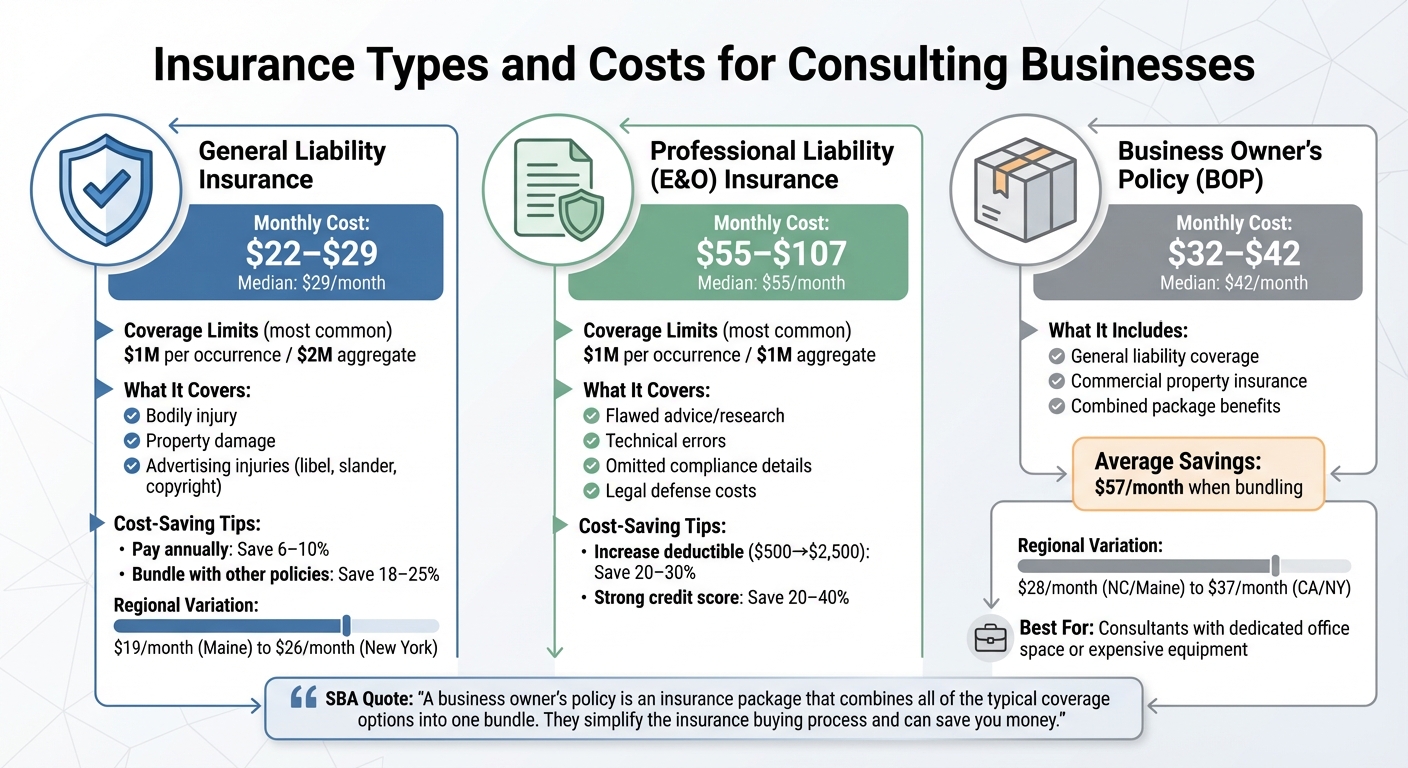

Insurance Types and Costs for Consulting Businesses

Consulting Business Insurance Costs Comparison: GL, E&O, and BOP Coverage

Insurance is a critical safeguard for consulting businesses, providing protection that an LLC alone can't offer. It shields you from claims and lawsuits tied to risks like giving flawed advice or causing accidental property damage.

Three key policies - general liability, professional liability (also called errors and omissions), and a business owner's policy - are worth considering. Each serves a specific purpose, and knowing their coverage and costs can help you plan your budget effectively. Here's a closer look at these policies and their typical price ranges.

General Liability Insurance

General liability (GL) insurance covers injuries or property damage caused by your business activities. For example, if a client trips over your laptop bag during a meeting, GL insurance can help cover medical expenses, legal fees, or settlements. It also protects against advertising-related issues like libel, slander, or copyright infringement.

GL insurance is relatively affordable, with median costs around $29 per month. Some providers even offer rates as low as $22 per month. Most consultants opt for policies with $1 million per occurrence and $2 million aggregate limits - a structure chosen by about 89% of policyholders. Rates can vary depending on location: consultants in New York may pay about $26/month, while those in Maine might pay closer to $19/month. Paying annually instead of monthly can save you 6–10% by avoiding processing fees, and bundling GL with other policies could reduce costs by 18–25%.

Professional Liability Insurance

Professional liability insurance, also known as errors and omissions (E&O), focuses on claims related to financial losses caused by your professional advice or services. Unlike general liability, which covers physical accidents, this policy addresses intellectual risks.

Common claims include providing flawed research that leads to poor investment decisions, making a technical error that disrupts a client’s system, or omitting compliance details that result in penalties. Even if you're not at fault, legal defense costs can be steep. The median cost for E&O insurance is about $55 per month, but rates can go as high as $107 per month based on your specialty and location. Around 70% of consultants choose policies with $1 million per occurrence and $1 million aggregate limits. Increasing your deductible - for instance, from $500 to $2,500 - can reduce your annual premium by 20–30%, and a strong credit score could lead to discounts of 20–40%.

Business Owner's Policy (BOP)

A business owner's policy combines general liability and commercial property insurance into a single package, making coverage simpler and often more cost-effective. According to the U.S. Small Business Administration:

"A business owner's policy is an insurance package that combines all of the typical coverage options into one bundle. They simplify the insurance buying process and can save you money." - U.S. Small Business Administration

For consultants, a BOP typically costs around $42 per month. This bundled coverage includes property protection for a modest additional fee. Bundling policies can save an average of $57 per month. Costs vary by state: consultants in California or New York might pay about $37 per month, while those in North Carolina or Maine could pay closer to $28 per month. If you work from a home office with minimal equipment, a BOP may not be necessary. However, if you have a dedicated office space or expensive hardware, the added coverage could be worth it.

| Policy Type | Avg. Monthly Cost | What It Covers |

|---|---|---|

| General Liability | $22 – $29 | Bodily injury, property damage, advertising injuries |

| Professional Liability | $55 – $107 | Negligence, errors, omissions in professional services |

| Business Owner's Policy | $32 – $42 | Combined general liability and property insurance |

Next, we'll dive into the essential tools and software you'll need to keep your consulting business running smoothly.

Tools and Software Expenses

Running a consulting business means relying on technology to keep things running smoothly. From managing client relationships to tracking finances and delivering results, the tools you use can make or break your operations. These tools generally fall into three key areas: client relationship management, market research and analytics, and daily operations hardware and software. Together, they help keep your business organized and professional, setting the stage for growth.

One of the perks of consulting is its relatively low startup costs. As Stripe notes:

"Service-based businesses, such as freelance design, writing, consulting, and virtual assistance, usually need only a computer, software, and a solid internet connection to begin".

This means you avoid the hefty infrastructure expenses that brick-and-mortar businesses face. Most consulting tools are subscription-based, making it easier to adjust your expenses as your business evolves.

To manage your budget effectively, separate one-time expenses (like buying a laptop or designing a website) from recurring ones (like monthly software subscriptions). Keeping digital records of your income, expenses, and deductions is a must - not just for bookkeeping but also to ensure you're taking full advantage of tax-deductible expenses. Tools for communication, market research, and building a professional website are also essential investments that can directly affect your financial planning.

CRM and Project Management Tools

CRM (Client Relationship Management) and project management tools are essential for staying on top of your business. These platforms let you track leads, organize workflows, and manage client communications. CRMs help with tasks like scheduling meetings and automating reminders, while project management tools break down deliverables, assign tasks, and monitor progress. Some platforms even combine both features, offering a streamlined experience. These tools often operate on a subscription basis, with costs varying depending on the number of users and available features.

When picking a tool, think about your specific needs. A solo consultant might find a basic plan sufficient, while someone managing a team or multiple clients may need a more advanced option. Many platforms offer free trials or startup credits. For instance, Stripe Atlas provides up to $50,000 in credits for essential tools. To manage cash flow, it’s smart to plan your subscriptions on a monthly or annual basis. If you’re tight on funds, consider bartering your consulting services in exchange for things like website hosting or graphic design.

Data Analytics and Market Research Platforms

Data analytics and market research tools are critical for backing up your strategies with solid evidence. Whether you're identifying trends or validating client recommendations, these tools enhance your credibility. For consulting startups, market research is often a key expense when launching and promoting services. Some platforms charge on a per-project basis, while others operate on a subscription model. Either way, the investment pays off, as clients expect data-driven advice.

Choosing the right platform depends on your niche. For example, a marketing consultant might need tools for social media analytics, while a financial consultant might prioritize access to economic data and industry benchmarks. Keep detailed records of these purchases, as they’re generally tax-deductible. If you’re pitching to investors or applying for loans, a detailed report of your software expenses can demonstrate how these tools align with your revenue goals.

Office Hardware and Productivity Software

Your daily operations also depend on reliable hardware and productivity software. At a minimum, you’ll need a dependable laptop or computer, a strong internet connection, and basic tools like word processing, spreadsheets, and presentation software.

Hardware is a key asset, and protecting it with business property insurance is a smart move. If you work from home, be aware that standard homeowner’s insurance often doesn’t cover business equipment. You might need a separate policy or rider to ensure your tools are protected.

For productivity software, look for tools that simplify your workflow and help you deliver polished results. For example, IdeaFloat’s Pro plan costs $40/month and bundles tools for planning, market research, and strategy development. As your business grows, review your hardware and software needs annually. Upgrading equipment or adding new tools may also require updating your insurance coverage. Keep thorough electronic records of all purchases, as the IRS accepts digital receipts for tax purposes as long as they include daily and monthly summaries of transactions.

| Tool Category | Purpose | Cost Type |

|---|---|---|

| CRM & Project Management | Track clients and organize workflows | Monthly subscription |

| Data Analytics & Research | Validate strategies and gather insights | Monthly or per-project |

| Office Hardware | Laptops, computers, and furniture | One-time purchase |

| Productivity Software | Daily operations and client deliverables | Monthly subscription |

Next, we’ll dive into the tax requirements and deductions every consulting business owner should know.

sbb-itb-08dd11e

Tax Requirements and Deductions

Running your own consulting business means you're in charge of managing taxes - no employer is withholding them for you. To stay on top of your obligations and avoid penalties, focus on three key areas: self-employment taxes, startup cost deductions, and quarterly estimated payments.

Self-Employment Taxes

As a consultant, you're responsible for self-employment (SE) tax, which covers Social Security and Medicare. Unlike traditional employees, you pay both the employee and employer portions, which totals 15.3% (12.4% for Social Security and 2.9% for Medicare).

To calculate your SE tax, start by subtracting necessary expenses from your gross income to get your net earnings. Then, 92.35% of that amount is subject to SE tax. For 2024, Social Security tax applies only to the first $168,600 of combined wages and net earnings, but Medicare tax applies to all net earnings. If your income exceeds $200,000 (single filers) or $250,000 (married filing jointly), you’ll also owe an additional 0.9% Medicare tax on the amount above those thresholds.

You must pay SE tax if your net earnings from self-employment are $400 or more. Here’s a silver lining: you can deduct half of your SE tax when calculating your adjusted gross income. While this deduction doesn’t lower the SE tax itself, it reduces your taxable income, giving you some relief. Plus, paying SE tax ensures you're eligible for Social Security benefits like retirement, disability, survivor benefits, and Medicare.

Startup Cost Deductions

The IRS allows you to deduct up to $5,000 in startup costs during your first year of business. These costs might include market research, legal fees, business registration, and initial advertising - essentially, anything spent before officially launching. However, if your startup costs exceed $50,000, the $5,000 deduction phases out dollar for dollar.

For expenses beyond the $5,000 limit, you’ll need to amortize them over 15 years, spreading the deduction over time. The IRS accepts digital receipts as long as they include detailed transaction summaries. Keeping thorough records not only helps maximize deductions but also provides clarity if you’re applying for funding or loans.

Quarterly Estimated Taxes

The U.S. tax system operates on a pay-as-you-go basis, meaning you’re expected to pay taxes throughout the year as you earn income. Since no employer is withholding taxes from your consulting income, you’re in charge of making quarterly estimated tax payments, which cover both federal income tax and self-employment tax.

You need to make estimated payments if you expect to owe $1,000 or more when filing your annual return. To avoid penalties, aim to pay at least 90% of your current year’s tax liability or 100% of the prior year’s tax - whichever is less. Use Form 1040-ES to calculate your payments, and adjust quarterly if your income varies.

| Payment Period | Period Dates | Due Date |

|---|---|---|

| 1st Payment | Jan 1 – March 31 | April 15 |

| 2nd Payment | April 1 – May 31 | June 15 |

| 3rd Payment | June 1 – Aug 31 | Sept 15 |

| 4th Payment | Sept 1 – Dec 31 | Jan 15 (following year) |

If a due date falls on a weekend or holiday, payments are due the next business day.

The easiest payment methods include IRS Direct Pay, a Business Tax Account, or the IRS2Go app, which also provides a record of your payment history. Don’t forget to check your state’s tax rules, as many states have their own estimated payment requirements. Staying consistent with quarterly payments helps you avoid penalties and keeps your finances manageable.

Total Cost Breakdown and Cash Buffer Planning

Once you've factored in insurance, tools, and taxes, it's time to calculate your total launch and operating costs. According to the SBA, most home-based businesses can get started with an investment of $2,000 to $5,000. However, setting aside $3,000 to $5,000 provides room for professional branding and legal protections. These costs are divided into one-time startup expenses and ongoing monthly overhead.

Initial Startup Costs

Startup costs cover all one-time expenses you incur before launching your business. This includes things like market research, legal fees for incorporation, logo design, initial website setup, and equipment purchases like laptops or office furniture. The IRS classifies these as capital expenditures, allowing you to deduct up to $5,000 in startup costs during your first year. However, if your total startup costs exceed $50,000, the $5,000 deduction is reduced dollar-for-dollar by the amount exceeding $50,000. Any additional expenses must be amortized over 15 years.

For larger purchases, such as computers or furniture, Section 179 expensing allows you to deduct the full cost immediately - up to $2,500,000 for 2025. Additionally, thanks to the "One Big Beautiful Bill" signed in July 2025, 100% bonus depreciation was permanently reinstated for qualified assets placed in service after January 19, 2025. Be meticulous in tracking pre-launch expenses, including travel to meet suppliers or consultant fees, as many of these qualify as deductible startup costs.

Once you’ve nailed down your startup costs, it’s time to assess your ongoing monthly expenses to identify your breakeven point.

Monthly Overhead and Breakeven Point

Recurring monthly costs are a critical part of your financial planning. These include expenses like rent, utilities, software subscriptions, insurance, and payroll. For example, business insurance typically costs between $1,750 and $2,575 annually, while software subscriptions can range from $20 to $150 per month. If you’re hiring employees, keep in mind that the actual cost of an employee is 1.25 to 1.4 times their base salary once you factor in taxes, insurance, and benefits. This means a $40,000 salary will actually cost between $50,000 and $56,000.

To determine your breakeven point, match your monthly expenses to your projected revenue. It’s wise to calculate at least one year’s worth of monthly expenses as a minimum cash buffer, though planning for five years can provide more stability. Additionally, set aside an extra 10–20% of your startup costs to cover unexpected expenses. Finally, open a dedicated business bank account right away - keeping personal and business finances separate is crucial and helps you avoid scrutiny from tax authorities.

Conclusion

Starting a consulting business involves careful planning for expenses like insurance, tools, and taxes. For instance, liability insurance typically costs between $1,000 and $1,350 annually, while software subscriptions range from $20 to $150 per month.

Taxes are another crucial factor. If your net earnings exceed $400, self-employment tax kicks in. Plus, if you anticipate owing $1,000 or more in taxes, you'll need to make quarterly estimated payments. Staying on top of these obligations requires disciplined cash flow management.

Speaking of cash flow, it’s important to prepare for the delays that often come with consulting contracts, which can have 60-day payment terms. Building a cash reserve to cover a few months of expenses can help you weather these gaps.

To keep costs low in the beginning, consider starting lean. Set up a home office, shop around for competitive insurance rates, invest in only the essential tools, secure an EIN, open a dedicated business bank account, and keep detailed records of your startup costs. These steps can help you stretch your resources and set a solid foundation for your business.

FAQs

What types of insurance do I need for my consulting business, and how can I save money on coverage?

For a consulting business, having general liability insurance and professional liability insurance is a must. General liability helps cover claims like property damage or bodily injury, while professional liability protects you if errors or negligence in your services lead to financial loss for a client.

To cut down on insurance costs, shop around and compare quotes from different providers to find the best fit for your needs. You can also lower premiums by bundling policies or opting for higher deductibles - just make sure these choices match your financial situation and comfort level with risk.

What’s the best way to track and manage expenses for tax deductions in my consulting business?

To handle your consulting business expenses for tax deductions effectively, start by keeping thorough and well-organized records of all business-related costs. These might include things like insurance premiums, software subscriptions, office supplies, and travel expenses. Using accounting tools or software can make tracking and categorizing these expenses much simpler and more consistent.

Make sure to review IRS guidelines to understand what qualifies as a deductible expense. Common examples include self-employment taxes, home office costs, and mileage. If you’re unsure or want to ensure you’re not missing any opportunities, consulting a tax professional can be a smart move. Accurate documentation is essential, so be diligent about saving receipts and invoices to support your claims.

How can I maintain financial stability while starting my consulting business?

To keep your finances steady when launching a consulting business, start by putting together a detailed budget. Include important expenses like insurance, essential tools (think project management or accounting software), and tax obligations. A clear budget helps you anticipate costs and sidestep surprises.

Get the right insurance in place - consider options like general liability or professional liability insurance to safeguard yourself from risks such as lawsuits or accidents. At the same time, opt for cost-effective tools to streamline your operations. Financial software can help you track expenses, while project management tools keep your workflow on track.

Don’t overlook taxes. Learn about self-employment taxes, keep tabs on potential deductions, and maintain accurate financial records. By budgeting carefully, securing proper insurance, and managing your finances wisely, you can set a solid foundation for your business.

Related Blog Posts

Get the newest tips and tricks of starting your business!