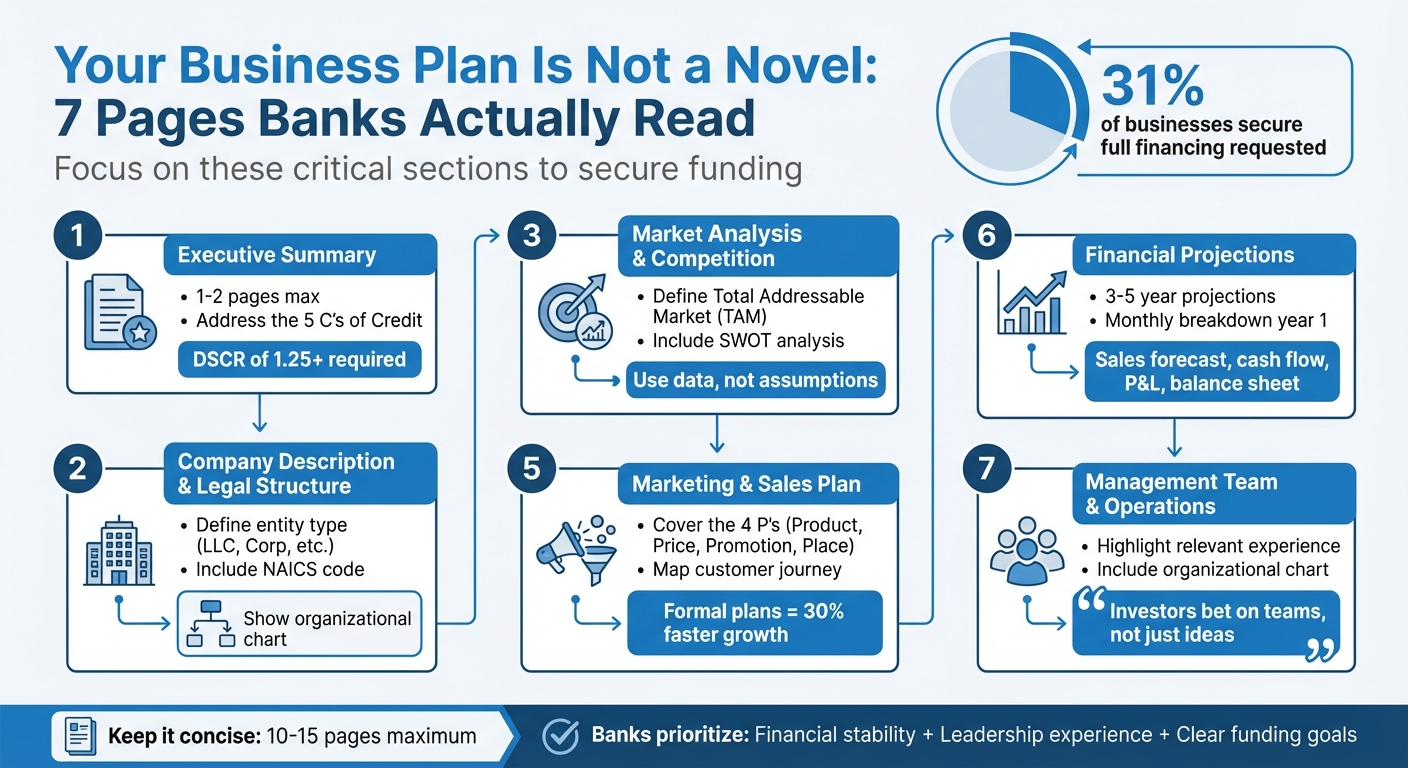

When applying for a loan, banks don’t read your entire business plan. They focus on seven critical sections to decide if your business is worth funding. Here’s what matters most:

- Executive Summary: A concise overview of your business, funding needs, and repayment ability.

- Company Description: Clear details about your business structure, mission, and leadership.

- Market Analysis: Data-driven insights about your target audience and competition.

- Product/Service Description: What you offer, pricing strategy, and how it solves problems.

- Marketing and Sales Plan: How you’ll attract customers and generate revenue.

- Financial Projections: Realistic numbers showing revenue, expenses, and loan repayment plans.

- Management Team and Operations: Showcasing experienced leadership and operational efficiency.

Focus on clarity, data, and realistic projections. Keep your plan concise - 10 to 15 pages max - and ensure every section demonstrates how you’ll repay the loan. Banks prioritize financial stability, leadership experience, and clear funding goals. Skip the fluff; give them the information they need to say yes.

7 Critical Business Plan Sections Banks Review for Loan Approval

How to Write a Business Plan Banks Will Say Yes To

1. Executive Summary

Your executive summary is the gateway to your business plan - a quick, impactful overview designed to grab the attention of investors and lenders. Bank of America emphasizes its importance:

"The executive summary is your opportunity to make a great first impression on investors and bankers. It should be just as engaging as the enthusiastic pitch you might give if you bumped into a potential backer in an elevator."

A poorly crafted summary can lead to your proposal being overlooked. Here’s how to create one that stands out.

Conciseness and Relevance of Information

Stick to one or two pages, ideally three to five focused paragraphs . Banks don’t have the time or patience for lengthy narratives - get straight to the point. Cover the essentials: your business idea, target audience, competitive edge, management team’s expertise, and the exact funding amount you’re requesting. Use straightforward language that anyone, even a busy banking officer, can easily understand . Think of it as distilling your entire business concept into its most vital points.

Alignment with Lender Expectations

For lenders, the big question is simple: Can you repay the loan? Address this directly by focusing on the "Five C’s of Credit" - Character, Capacity, Capital, Conditions, and Collateral. Be precise about your funding needs. For instance, instead of a vague "$250,000+", specify "$247,500" to demonstrate you’ve done your homework. Break down how you’ll use the funds, whether it’s for delivery vehicles, inventory, or working capital. Lenders also look for a Debt Service Coverage Ratio (DSCR) of 1.25 or higher, which shows your business generates 25% more income than its debt obligations.

Clarity in Presenting Financial and Market Data

Numbers tell the story, so be specific. Replace general phrases like "a large market" with concrete figures such as "a $10 billion addressable market" . Include key metrics like projected revenue, profit margins, and your breakeven point. Highlight the experience and accomplishments of your management team, as lenders often place as much value on the team as they do on the business idea . Use bullet points and short sentences to make financial and market data easy to skim. Avoid inflating numbers - experienced bankers can spot unrealistic projections instantly, so stay conservative and realistic .

Credibility of Assumptions and Projections

Your projections need a solid foundation. Back them up with data from reliable sources like customer surveys, industry reports, or competitive analysis . As Pete from GrowthGrid puts it:

"A powerful, concise summary grabs their attention and convinces them your business model is worth their time; a weak one ensures your detailed plan gathers dust."

To ensure accuracy, write this section last. By doing so, you can align it with the final data and conclusions in your business plan . This ensures consistency and helps establish trust with your audience.

2. Company Description and Legal Structure

This section is your opportunity to establish your business's credibility while outlining a clear legal framework. A well-drafted company description not only defines roles and responsibilities but also reinforces the financial and strategic details presented in your executive summary.

Conciseness and Relevance of Information

Start by specifying your business entity type - whether it's a sole proprietorship, LLC, C corporation, or S corporation. Include the state of incorporation and the official incorporation date. Adding your NAICS code is a smart move, as it helps lenders evaluate your business and understand tax and insurance requirements. Keep your mission statement short and impactful - just one sentence that captures the essence of why your business exists. Stick to the essentials and avoid unnecessary details.

Alignment with Lender Expectations

Lenders value clarity and accountability, so your legal structure should reflect both. Highlight how your business structure aligns with lender expectations, particularly in terms of Character and Capacity. For instance, explain why you chose your specific legal structure (e.g., LLC vs. sole proprietorship) and include an organizational chart that showcases key leadership roles and their expertise. Experienced management is a big plus - identify principal team members, their roles, and their relevant experience. If you work with external consultants, such as an outsourced CFO, mention them to emphasize professional support. Be sure to include an appendix with important legal documents like permits, licenses, deeds, contracts, and resumes for key team members.

Credibility of Assumptions and Projections

Use a concise SWOT analysis to highlight your business's strengths and acknowledge potential weaknesses. As LendingTree wisely notes:

"Lenders and investors may be more nervous going into business with an owner wearing rose-colored glasses compared to one who understands the potential risks."

If your business operates in a specialized field, take the time to define any industry-specific terms so lenders can grasp your operations without confusion. Ensure that the legal structure described in your company profile aligns perfectly with the documents in your appendix - any inconsistencies could hurt your credibility. Finally, if you plan to hire for specific roles, outline these staffing needs to show you've thought ahead and are prepared for growth.

3. Market Analysis and Competition

Your market analysis is your chance to prove to lenders that your target audience isn’t just theoretical - it’s real, reachable, and willing to pay for what you offer. Banks and investors sift through countless business plans, so this section needs to lean heavily on data, not vague promises of untapped potential. Start by defining your total addressable market (TAM) and break it down into specific segments by demographics and psychographics. Be precise - include your NAICS code for clarity. Then, identify realistic customer segments and provide sales projections grounded in audiences you can actually reach. From there, dive into your competition to show how your business stands out.

Conciseness and Relevance of Information

When discussing competitors, name both direct and indirect players and consider including a SWOT table to pinpoint market gaps and highlight your strengths. Look for underserved customer groups or recurring complaints about existing services - these can be golden opportunities. If your business is local, keep the focus on your immediate geographic market rather than national trends. Avoid drowning in industry jargon, and make sure any specialized terms are clearly explained.

Alignment with Lender Expectations

Lenders want a balanced view, not just optimism. As LendingTree points out:

"Lenders and investors may be more nervous going into business with an owner wearing rose-colored glasses compared to one who understands the potential risks."

Be upfront about weaknesses in your SWOT analysis and explain how you plan to tackle those challenges. This kind of honesty can make you appear more prepared and trustworthy.

Clarity in Presenting Financial and Market Data

Graphs and charts can be your best friend here. Use them to clearly show trends, growth projections, and how these align with your sales forecasts. Back up your claims with primary research, like customer surveys, interviews, or product testing, to prove there’s genuine demand for your offering. Visual aids like these help connect the dots between your market analysis and financial projections.

Credibility of Assumptions and Projections

Support your projections with data from reliable sources, such as industry reports, government statistics, or trade publications. If possible, use historical financial data or benchmarks from similar companies to ground your estimates in reality. Highlighting eco-friendly practices can also give you a competitive edge. Keep in mind that only 31% of businesses secure the full financing they request, so making your market analysis as credible and data-driven as possible can significantly boost your chances of success.

4. Product or Service Description with Pricing Strategy

Banks want a clear picture of what you're offering, who your customers are, and whether your financials hold up. This section should explain the problem your product or service solves and what benefits it delivers to customers. Lay out the typical buying process so lenders can see how revenue flows into your business. If you're requesting funding for equipment or inventory, provide a detailed list of what’s essential. Also, mention any patents, trademarks, or copyrights that give your business an edge. This detailed breakdown sets the stage for discussing your pricing strategy and builds lender confidence.

Conciseness and Relevance of Information

Stick to simple, clear language that anyone can follow. If you need to include industry-specific terms, define them right away. Show how your product or service stands out from competitors and why customers will choose you. Emily Heaslip from the U.S. Chamber of Commerce emphasizes:

"Your product or service is the crux of your business idea, so you want to make a strong case for its purpose and role in the market."

Alignment with Lender Expectations

Beyond defining your product, lenders want to understand the reasoning behind your pricing. They’ll assess your product using the "5 C's of Credit", focusing on conditions (like market demand and trends) and capacity (your ability to generate cash flow). Don’t just state your price - explain it. Compare your pricing to competitors, show why it appeals to your target audience, and include a detailed cost-to-profit breakdown. For example, compare your cost of goods sold (COGS) to your selling price to highlight profitability.

Clarity in Presenting Financial and Market Data

Numbers are key to building trust. Your pricing strategy should clearly show whether you're targeting a budget-conscious audience or positioning yourself as a premium option - and how that approach gives you a competitive edge. Back this up with a break-even analysis using the formula: Fixed Costs ÷ (Sales Price per Unit – Variable Cost per Unit). This calculation helps lenders see when you expect to turn a profit. If you have multiple revenue streams, such as direct sales, subscriptions, or advertising, break down the pricing structure for each.

Credibility of Assumptions and Projections

Base your projections on solid data. As Bank of America advises:

"Seasoned bankers and investors will quickly spot overly optimistic numbers."

Use reliable sources like the U.S. Census Bureau or industry trade groups to back up your pricing models and demand forecasts. Factor in real-world challenges, such as seasonal fluctuations or the time it takes to ramp up operations, to ensure your projections feel realistic. This level of detail and accuracy will reassure lenders that your business is built on sound assumptions.

sbb-itb-08dd11e

5. Marketing and Sales Plan with Go-to-Market Strategy

Banks want to know exactly how you plan to attract customers and generate revenue. This section should outline the journey from customer discovery to purchase. Highlight the channels you'll target - like paid search or TikTok - and explain why they align with your audience. Lay out specific tactics such as lead scoring, free trials, or referral programs. By building on the foundational business details covered earlier, this section sets the stage to back up your revenue forecasts.

Conciseness and Relevance of Information

Focus your marketing plan on the "Four Ps": Product (what makes you stand out), Price (how your pricing reflects value), Promotion (how you'll capture attention), and Place (where you'll sell). As the U.S. Small Business Administration notes:

"Your goal in this section is to describe how you'll attract and retain customers. You'll also describe how a sale will actually happen."

Use concrete examples to bring your plan to life. For instance, detail your online advertising strategy or describe targeted influencer collaborations. If your business is already up and running, include real-world data to showcase what's working and why.

Alignment with Lender Expectations

Lenders often assess your plan using the "Five C's of Credit", with a strong focus on conditions. They’ll want to see evidence of product demand, an understanding of your competition, and alignment with industry trends. Break down your total addressable market into specific customer segments and explain why your approach resonates with them. Your marketing strategy should directly support your financial projections, particularly in terms of sales forecasts and expense budgets. This connection assures lenders that your business can generate the cash flow needed to repay loans, addressing their concerns about financial stability.

Clarity in Presenting Financial and Market Data

Map out a clear sales funnel with steps, timelines, and key tactics - like interactive demos or targeted email campaigns - to illustrate how you’ll convert leads into customers. Include details about distribution and fulfillment processes, such as how orders will be manufactured, packaged, and delivered. If you have multiple revenue streams, like direct sales, subscriptions, or licensing, break down the customer acquisition strategies for each. This detailed marketing strategy ties directly to the financial projections discussed in the next section.

Credibility of Assumptions and Projections

Keep your projections grounded in reality. As LendingTree points out:

"Lenders and investors may be more nervous going into business with an owner wearing rose-colored glasses compared to one who understands the potential risks."

Conduct a focused SWOT analysis to address marketing risks like seasonal demand changes or long sales cycles. Use reliable sources - such as industry research, customer interviews, or pilot campaign data - to back your assumptions about market size and growth. This level of detail strengthens the credibility of your financial projections and demonstrates that your plan is both thoughtful and data-driven. After all, founders who create formal business plans grow 30% faster than those who don’t.

6. Financial Projections and Capital Requirements

Once you’ve laid out your marketing strategy, it’s time to back it up with solid numbers. This section translates your plan into financial terms that lenders will scrutinize. You’ll need to include key financial documents: Sales Forecast, Expenses Budget, Cash Flow Statement, Income Projection (Profit and Loss), and a Projected Balance Sheet. Plan for three to five years, breaking down the first year by month, and summarizing the following years quarterly or annually. As Linda Pinson, author of Anatomy of a Business Plan, says:

"This is what will tell you whether the business will be viable or whether you are wasting your time and/or money".

This step connects your strategic ideas to concrete financial data.

Conciseness and Relevance of Information

Stick to the core financial statements that demonstrate your business’s ability to meet its obligations and repay loans. The cash flow statement is especially important - it shows whether you’ll have enough cash each month to cover expenses. Be sure to include a breakeven analysis to pinpoint when your revenue will match your expenses, marking the moment your business becomes self-sustaining. Clearly state the total funding you need, how you’ll use it, and your repayment plan.

Alignment with Lender Expectations

Lenders will measure your projections against the "Five C's of Credit", particularly focusing on your capacity to manage debt. They’ll calculate debt coverage ratios to confirm you’ll have enough leftover cash after expenses to make loan payments. Make sure your financials reflect the loan in three key areas: list it as a liability on the balance sheet, include interest expenses on the profit and loss statement, and show repayment installments in the cash flow statement. Every number should tie back to your marketing strategy and revenue assumptions for a cohesive presentation.

Clarity in Presenting Financial and Market Data

Break down your revenue forecast into clear, verifiable parts - whether by sales channel, customer segment, or product line. Separate fixed costs (like rent and payroll) from variable costs (such as advertising and materials). These numbers should directly reflect the market trends and sales strategies you’ve outlined earlier. Tim Berry, founder of Palo Alto Software, cautions:

"There is a tremendous problem with the hockey-stick forecast... They really aren't credible".

Avoid unrealistic projections that show flat sales followed by sudden, steep growth. Instead, use visual aids like bar graphs or pie charts to illustrate steady, achievable growth trends. This makes it easier for lenders to quickly understand your business’s trajectory.

Credibility of Assumptions and Projections

Support your numbers with a "Notes to Financials" section explaining the assumptions behind them. For instance, detail your invoice collection rates (e.g., 80% paid within 30 days) or customer acquisition costs based on pilot campaigns. Use conservative estimates for factors like interest rates and taxes - lenders value realistic, grounded goals over overly optimistic ones. Cite reliable sources, such as industry research, customer interviews, or historical data from your operations. Also, demonstrate your commitment by mentioning any personal funds you’re investing. Showing that you have a financial stake in the business can significantly boost lender confidence. Keep your projections realistic and backed by verifiable data to build trust.

7. Management Team and Operations Plan

Lenders want to know who's steering the ship and whether they have what it takes to make the business thrive. As Bank of America puts it:

"Many investors say they bet on the team behind a business more than the business idea, trusting that talented and experienced people will be capable of bringing sound business concepts to life."

This section is your chance to prove you’ve assembled the right team to execute your plan and meet loan repayment expectations.

Focused and Relevant Details

When presenting your team, keep it concise. Highlight only the experience and skills directly relevant to their roles. Include an organizational chart that clearly outlines each person’s responsibilities. On the operations side, explain the essentials: why your location is strategic, the tools or software critical to your processes, and how you handle orders from start to finish.

Meeting Lender Expectations

At this stage, lenders are assessing whether your team has the expertise to execute the business plan effectively. Banks often evaluate this under the "Character" component of the Five C's of Credit, looking for proven experience and results. To build confidence, emphasize any industry recognition, awards, or specialized skills your team brings to the table. Use professional headshots and a well-designed organizational chart to make the section visually engaging. Tailor each team member’s bio to explain why they’re a perfect fit for their role - don’t just copy and paste their LinkedIn profiles. This tailored approach reinforces the credibility you’ve established in earlier sections.

Grounding Assumptions and Projections

Support your plan with specific milestones, like completing a prototype or hitting monthly sales goals, that show how funding will translate into measurable results. Break down staffing costs, such as salaries or contractor fees, and use a brief SWOT analysis to address potential operational challenges. If you’re running a home-based business to save on overhead, explain this strategy and outline plans for future expansion into a commercial space. These details show lenders that your projections are grounded in reality and that you’ve thought through every aspect of your operations.

Conclusion

When crafting your business plan, focus on what lenders truly need to make informed decisions. It doesn’t have to be a masterpiece of storytelling. What matters most is demonstrating a clear market opportunity and the ability to turn that opportunity into results. As Tim Berry, Founder of Palo Alto Software, wisely states:

"Banks don't just fund great business plans. They fund businesses that have a plan, have clearly identified a market opportunity and demonstrate the ability to execute on that opportunity".

The numbers tell a sobering story: only 31% of businesses secure the full financing they request from lenders. Often, the key to success lies in giving loan officers exactly what they need to make a fast, confident decision.

Stick to the essentials by focusing on the seven critical sections discussed earlier. Any extra materials - like resumes, permits, or technical details - should be moved to an appendix. This keeps your plan streamlined and easy to navigate.

When it comes to financial projections, aim for realism over flair. Experienced bankers can spot overly optimistic numbers in an instant, and nothing erodes trust faster. Show that you understand your market, have the right team in place, and know exactly how you’ll repay the loan. That’s what earns their confidence.

Finally, use clean, professional formatting with ample white space. Remember, clarity always trumps creativity when you’re asking someone to invest in your vision. By following these strategies, you’ll create a business plan that not only meets lender expectations but also sets your business on the path to success.

FAQs

Why do banks focus on specific sections of a business plan?

Banks pay close attention to specific parts of a business plan because these sections reveal the most essential details about your business’s potential. They’re particularly interested in your financial projections, market analysis, and executive summary, as these elements help them gauge your business’s viability and your ability to repay a loan.

By presenting these sections clearly and effectively, you make it easier for lenders to evaluate your business’s strengths, identify potential risks, and understand its growth potential - key factors in their decision-making process.

What’s the best way to make my financial projections realistic and trustworthy?

When building financial projections that stand up to scrutiny, start with solid data sources such as past performance, current market trends, and industry standards. Be sure to base your assumptions on realistic expectations and explain them clearly - steering clear of overly ambitious or unclear estimates.

It's also important to keep your projections updated to align with real business performance and shifting market conditions. This proactive approach signals to lenders that you're staying on top of things and adjusting as needed. By keeping your projections straightforward, well-researched, and grounded in facts, you'll make a stronger case to banks and financial institutions.

What should I include in the executive summary to make a strong impression on a bank?

To catch a bank's eye, your executive summary needs to be short, sharp, and packed with essential details. Here’s what to include:

- A quick snapshot of your business idea and objectives.

- Key financial highlights, like expected sales, profits, and cash flow figures.

- A summary of the funding you’re seeking and exactly how you’ll use it.

- Major accomplishments or milestones that showcase your business’s promise.

Aim to keep it between half a page and one page. Make it easy to skim while emphasizing your business's strengths and financial potential.

Related Blog Posts

- I Analyzed 1,000 Business Plans - Here's What The Successful Ones Had

- IdeaFloat: How to Create a Business Plan That Banks Can't Resist

- I Asked 20 Bank Loan Officers What They Look for in Business Plans - Here's What They Said

- Idea to Plan: The 1-Page Business Plan Banks Don’t Hate (Template)