You can start a lawn care business for under $1,500 if you already have a vehicle, but a full setup can run past $15,000 fast.

If I were sizing up this business today, I’d focus on four cost buckets first: equipment, transport, monthly fuel and upkeep, and insurance. The biggest swing is usually your truck or trailer setup. And one of the most missed costs is insurance, which can run about $2,605 to $3,870 per year for a solo operator.

Here’s the short version:

- Bare-bones startup: about $755–$1,500 if I use gear I already own and skip a trailer

- Solo full-time setup: about $3,000–$10,000 before adding a truck I need to buy

- Truck cost: often $8,000–$20,000 for a used work vehicle

- Open trailer: about $300–$3,500

- Monthly fuel, upkeep, and supplies: about $275–$550

- A basic residential mowing price point: often $45–$55 for a 1/4-acre lot

What this means is simple: the business itself is not that expensive to start - unless I need to buy transport from scratch. Before spending money, I’d check whether local jobs can cover my hourly costs, fuel, and insurance.

Lawn Care Business Startup Costs: 3 Setup Tiers at a Glance

HOW MUCH does it COST to Start a Lawn Care Business? (NOT what you think!)

sbb-itb-08dd11e

Quick comparison

| Setup | Upfront Range | Best For | Main Catch |

|---|---|---|---|

| Side hustle | $755–$1,500 | Testing the market | Limited gear and slower job pace |

| Solo operator | $3,000–$10,000 | Full-time mowing route | Cost jumps if I need a truck |

| Pro setup | $15,000–$50,000+ | High-volume route or crew | Big cash outlay up front |

If I wanted one takeaway from this guide, it would be this: buy only the gear I need to start, keep transport lean, and price jobs based on overhead instead of guesswork.

Equipment Costs: Tools You Need and What They Cost

Equipment is where most of your startup budget usually goes. So it helps to get clear on what you need right away and what can wait until you’ve got jobs coming in.

Core Starter Equipment and Typical Price Ranges

On day one, start with the basics: a commercial 21-inch mower, string trimmer, backpack blower, and PPE like ear protection, safety glasses, gloves, and steel-toe boots. The right setup depends on the size of the route you plan to handle.

Skip residential-grade tools if you’ll be using them every day. They tend to wear out fast. Commercial-grade gear costs more up front, but it’s built for regular use.

Here’s what the core equipment usually costs:

- A commercial 21-inch mower costs $400–$800 new or $150–$400 used

- A commercial string trimmer runs $200–$350 new

- A backpack blower usually costs $200–$500 new

- PPE, including ear protection, safety glasses, gloves, and steel-toe boots, adds $100–$300

If you buy used commercial equipment from dealers or online marketplaces, you can cut your cost by 40%–50%.

One smart way to keep spending down: use a trimmer with an edger attachment instead of buying a separate edger. That can save you $100–$350 until you’ve got enough edging work to make the upgrade worth it.

Basic vs. Mid-Tier vs. Fully Equipped Setups

A zero-turn mower can save time compared to a standard walk-behind. But most operators should wait until they have at least 20 weekly accounts or are mowing 6+ lawns per day before buying one.

Here’s how the main setup tiers compare:

| Setup Tier | Equipment Included | Typical Cost Range | Best Fit |

|---|---|---|---|

| Basic (Bootstrap) | Used push mower, consumer trimmer, handheld blower, PPE: ear protection, safety glasses, gloves, and steel-toe boots | $600 – $2,000 | Part-time or market testing |

| Mid-Tier (Owner-Operator) | Commercial walk-behind mower, pro trimmer, backpack blower, full PPE | $3,000 – $13,000 | Full-time solo operators with 15–20 clients |

| Fully Equipped (Growth) | Commercial zero-turn mower, backup tools, specialized gear | $15,000 – $35,000+ | High-volume routes or multi-crew operations |

For tools you won’t use every day, renting or borrowing usually makes more sense. That includes aerators, dethatchers, and hedge trimmers, at least until customer demand makes ownership a smart move.

Once you’ve priced out the tools, the next big piece is transportation.

Trailer and Transport Costs: Moving Your Equipment

Once you have the tools, you still need a way to move them from job to job. And this part can swing your startup budget by $10,000 to $20,000 depending on what you buy. In plain terms, your transport setup can either keep costs lean or push your startup total up fast.

Open Utility Trailers, Enclosed Trailers, and Vehicle Use

If you already own a pickup truck or SUV with towing capacity, your day-one transport cost can be $0. For a solo operator in a first season, a truck bed with a ramp is the bare-minimum setup that can still get the job done.

When you need to haul a zero-turn or bring more gear, a 6x12 open utility trailer is usually the next step. It gives you space for a zero-turn mower, fuel cans, and other gear. New trailers often cost $1,500–$3,500, while used ones usually fall between $300–$1,500.

You should also plan for the small add-ons that sneak into the bill:

- Trailer hitch and wiring: $150–$400

- Tie-downs, ramps, and a lockbox: $100–$300

Open trailers are cheaper, but they leave everything out in the open. That means rain, theft, and road grime are all part of the deal, so locks and solid tie-downs are money well spent.

An enclosed trailer gives you more security and keeps equipment out of bad weather, but it costs more up front. Prices usually land between $3,000–$8,000. For many operators, that makes more sense in year two, after income is steadier. It also burns more fuel and can be a pain to back into tight driveways or narrow streets.

You’ll also need to account for fixed transport costs beyond the trailer itself. Commercial auto coverage matters here, and trailer registration adds another line item. Annual trailer registration and plates can add $100–$400 per year.

Transport Cost Comparison by Setup Type

| Transport Option | Typical Use Case | Upfront Cost Range | Tradeoffs |

|---|---|---|---|

| Existing Truck/SUV | Solo starter, small residential lots | $0 (if owned) | Limited space; high wear on personal vehicle; difficult to haul large mowers |

| Personal Vehicle + Small Trailer | Bootstrap or side-hustle; testing the market | $300–$2,000 | Low entry cost; requires hitch installation; gear is exposed to weather and theft |

| Open Utility Trailer (6x12) | Standard solo setup; hauling zero-turns | $300–$3,500 | Versatile and easy to load; no protection from rain; needs tie-downs and locks |

| Used Work Truck | Solo operator needing dedicated hauling capacity | $8,000–$20,000 | Better reliability than older personal cars; higher upfront cost |

| Enclosed Trailer | Established operator; high-security needs | $3,000–$8,000 | Added security and weather protection; heavier to tow; higher fuel costs |

That one decision also changes your monthly fuel bill and upkeep. After transport, the next costs to watch are fuel, maintenance, and insurance.

Fuel, Maintenance, and Insurance Costs

Once you start working, the meter is always on. Fuel, upkeep, and insurance show up month after month, so they need a place in your budget from day one.

Monthly Fuel and Maintenance Budgets

A solo operator typically spends $275–$550 per month on fuel, maintenance, and consumables. That usually means regular gas for the truck and mower, plus 2-cycle fuel mix for trimmers and blowers.

| Expense Item | Startup Reserve (One-Time) | Ongoing Monthly Cost |

|---|---|---|

| Truck Fuel | $50–$100 | $150–$250 |

| Equipment Fuel | $30–$50 | $50–$150 |

| Maintenance | $0 | $50–$100 |

| Consumables (Trimmer Line, Spark Plugs) | $100–$200 | $25–$50 |

| Total | $180–$350 | $275–$550 |

It also helps to set aside $1–$2 per equipment hour for repairs. That small habit can save you when a belt snaps, a spark plug fails, or a trimmer head wears out in the middle of a busy week.

Those costs are usually easy to see coming. Insurance is different. You may not need it every day, but when something goes wrong, it can protect the money you put into the business.

Liability, Commercial Auto, and Equipment Insurance

Insurance is one of the most missed startup costs.

In lawn care, a single property damage claim averages $8,000–$25,000. That’s a hard hit for any solo operator. Most of the risk is covered by three core policies.

- General liability covers third-party injury and property damage, like a rock breaking a window.

- Commercial auto covers business-use driving; personal auto policies usually exclude paid hauling.

- Inland marine - also called equipment or tools coverage - covers your mowers and trimmers if they’re stolen off the trailer or damaged in transit.

Fuel and maintenance keep the business moving each month. Insurance helps protect the whole startup budget if one bad day turns expensive.

| Policy Type | What It Covers | Monthly Range | Annual Range |

|---|---|---|---|

| General Liability | Property damage & third-party injury | $38–$73 | $450–$870 |

| Commercial Auto | Business vehicle & trailer accidents | $167–$208 | $2,000–$2,500 |

| Inland Marine | Theft/damage of mowers & tools | $13–$42 | $155–$500 |

| Total Solo Bundle | Comprehensive protection | $218–$323 | $2,605–$3,870 |

Bundling all three policies with one insurer can cut your total premium by 18% to 25% compared to buying each separately.

Startup Budgets and Final Takeaways

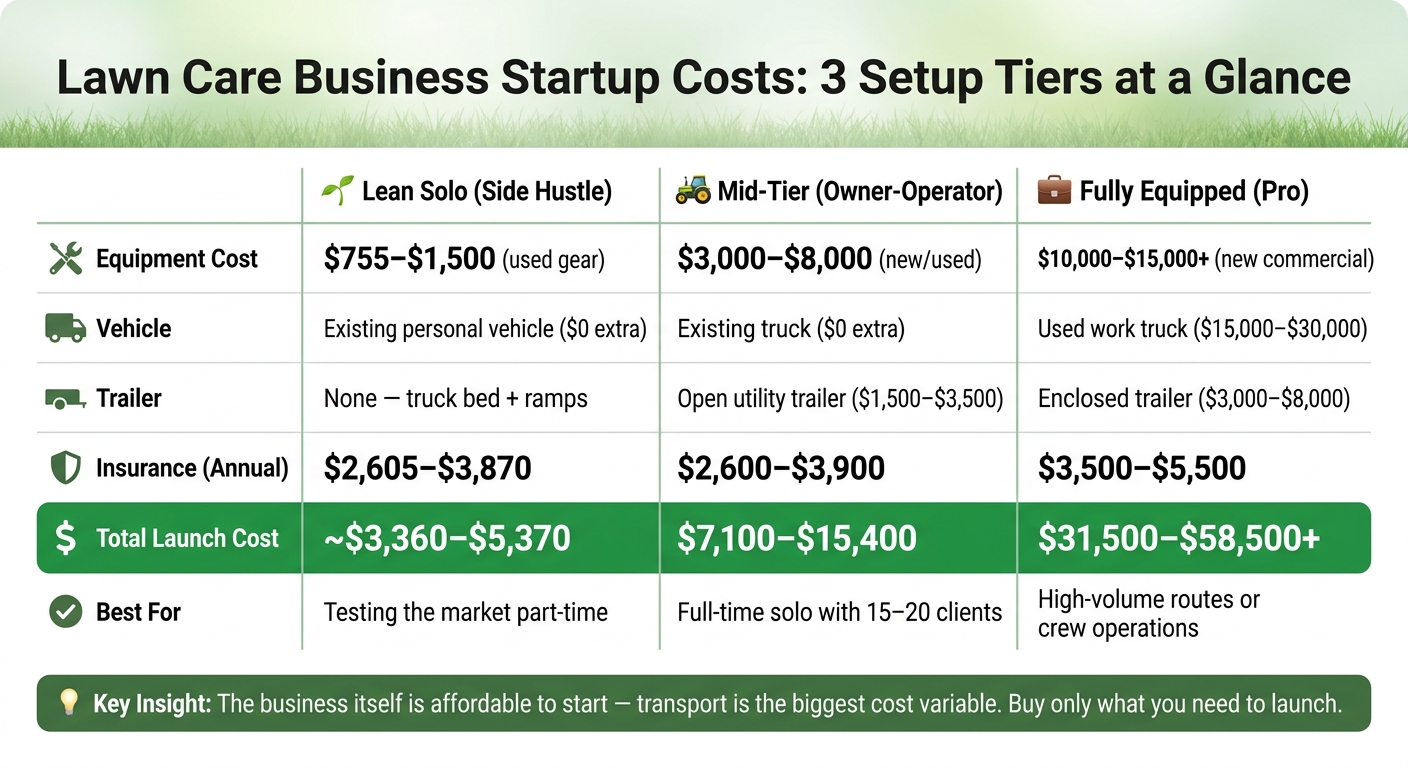

3 Sample Startup Budgets

Here are three sample launch budgets based on the cost ranges above. They roll together equipment, trailer, fuel, and insurance so you can see what a starting setup might look like.

| Category | Lean Solo (Side Hustle) | Mid-Tier (Owner-Operator) | Fully Equipped (Pro) |

|---|---|---|---|

| Equipment | $755–$1,500 (used) | $3,000–$8,000 (new/used) | $10,000–$15,000+ (new) |

| Vehicle | Existing personal vehicle | Existing truck | $15,000–$30,000 (used truck) |

| Trailer | None (truck bed/ramps) | $1,500–$3,500 (open) | $3,000–$8,000 (enclosed) |

| Insurance (Annual) | $2,605–$3,870 (full bundle) | $2,600–$3,900 (full bundle) | $3,500–$5,500 (full bundle) |

| Total Launch Cost | ~$3,360–$5,370 | $7,100–$15,400 | $31,500–$58,500+ |

Set aside extra cash for the first 30 to 90 days.

These launch totals work best as a starting point. After that, stack them up against what local routes in your area can earn.

How to Check Your Numbers Before You Buy

Next, pressure-test these totals against local route pricing before you spend a dollar.

Start with a simple route estimate. A standard residential cut on a 1/4-acre lot usually brings in $45–$55. So if your goal is 15 weekly accounts at $50 each, that puts you at $750 per week in gross revenue. Then comes the part people tend to gloss over: fuel, insurance, and your own time. That's what tells you what you're actually making.

Then figure out your break-even rate. Add your overhead cost per hour - usually $8–$15 for a solo operator - to the wage you want to take home. That total is your pricing floor. If a job comes in below that number, you're not making money on it. You're paying to do the work.

FAQs

How many clients do I need to break even?

There’s no single number here. Your break-even point comes down to three things: startup costs, overhead, and pricing.

Some operators hit break-even in 3 to 6 months by keeping costs low and staying lean early on. If your annual costs land around $17,400 to $32,000 before paying yourself, the number of clients you need will depend on how much profit you keep from each lawn after fuel, maintenance, insurance, and equipment costs.

Should I buy used equipment or start new?

It comes down to cash flow and how much risk you can live with.

Used equipment can cut your upfront cost by 50% or more, which is a big deal when you're trying to keep spending under control. The trade-off is pretty simple: older gear can mean more repairs, more maintenance, and more downtime when you least need it. If you go the used route, buy from reputable dealers that inspect and service trade-ins.

New equipment gives you better reliability and warranty coverage, which can save a lot of stress early on. That said, don't pour money into top-tier gear before you have a steady client base. And one rule shouldn't budge: always buy safety gear new.

Do I need insurance before my first job?

Yes. You should have insurance before taking your first job.

General liability and commercial auto insurance help protect you if you cause property damage or someone is injured. A personal auto policy often won’t cover business use, especially if you’re towing a trailer. Without the right coverage, a single accident or theft can lead to major financial loss.

Related Blog Posts

- How to Start a Pressure Washing Business With Under $1,000

- How to Start a Profitable Lawn Care Business: Complete Guide

- Handyman Startup Costs: Tools, Vehicle, Insurance

- Lawn Care Startup Costs in Australia: Equipment, Pricing, Profit