As a new business owner, you can legally reduce your taxes by leveraging IRS-approved strategies. Here's how:

- Claim Deductions: Write off business expenses like equipment, office costs, and even health insurance.

- Use Tax Credits: Take advantage of credits for hiring employees, research, or offering health coverage.

- Choose the Right Business Structure: Switching to an LLC or S-Corp could save you thousands in self-employment taxes.

- Plan Income and Expenses: Time your income and purchases to maximize tax savings.

- Invest in Retirement: Contributions to Solo 401(k)s or SEP IRAs can lower your taxable income.

💡 Quick Tip: A small business owner who tracks deductions and adjusts their structure can cut their tax rate by up to 20%.

Quick Comparison:

| Strategy | Benefit | Example |

|---|---|---|

| Deductions | Lowers taxable income | Write off $5,000 in startup costs |

| Tax Credits | Directly reduces taxes owed | $9,600 for hiring eligible employees |

| Business Structure | Reduces self-employment tax | S-Corp saves on distribution taxes |

| Income Timing | Shifts income to lower-tax years | Delay invoicing to next year |

| Retirement Contributions | Immediate tax deduction + savings | $70,000 Solo 401(k) contribution |

Remember: Tax evasion is illegal, but tax planning is smart. Keep records, consult experts, and follow the rules to grow your business while keeping more money in your pocket.

15 Biggest Tax Write Offs for Small Business! [What the Top 1 ...

Legal Tax Reduction vs. Tax Evasion

It’s important to understand the difference between legally reducing your taxes and committing tax evasion. Legal tax reduction involves using IRS-approved methods to lower your tax liability, while tax evasion is an illegal act of hiding or misrepresenting income.

Legal Ways to Lower Taxes

Legal tax reduction relies on strategies sanctioned by the IRS. As Wolters Kluwer puts it, "Tax avoidance lowers your tax bill by structuring your transactions so that you reap the largest tax benefits. Tax avoidance is completely legal - and extremely wise".

Here are some common ways to legally reduce your taxes:

| Strategy | Description | Benefit |

|---|---|---|

| Business Expense Deductions | Claim legitimate operating costs | Fully deductible |

| Section 179 Deduction | Deduct the cost of qualifying equipment | Up to IRS limits |

| QBI Deduction | Claim the Qualified Business Income deduction | Up to 20% of business income |

| Health Insurance Premiums | Deduct self-employed health insurance | Fully deductible |

| Retirement Contributions | Contribute to SEP IRA, SIMPLE IRA, or Solo 401(k) | Tax-deferred growth |

These strategies can help reduce your tax burden, but they must be implemented correctly. Missteps could unintentionally cross into illegal territory.

Consequences of Tax Evasion

Tax evasion happens when someone deliberately misrepresents or conceals information to lower their tax liability.

"Tax evasion is illegal and involves intentionally misrepresenting or concealing information on a tax return to reduce tax liability" – SBBL Law

For example, in 2023, an Illinois store owner was sentenced to 76 months in prison and ordered to pay over $5 million in restitution for underreporting $60 million in income.

The penalties for tax evasion are severe and may include:

- Fines of up to $250,000 for individuals and $500,000 for corporations

- Prison sentences of up to 5 years

- Full payment of evaded taxes, plus interest

- Prosecution costs

- A penalty of 20% on underpayment amounts

To minimize taxes without risking legal trouble, make sure to:

- Keep detailed records of income and expenses

- Consult qualified tax professionals

- Use legitimate deductions and credits

- File accurate and timely returns

- Stay updated on changes in tax laws

Pick the Right Business Structure

Your choice of business structure affects both your taxes and legal protections. Here's a quick comparison of common structures and how they differ in key areas:

| Structure | Tax Treatment | Self-Employment Tax | Liability Protection |

|---|---|---|---|

| Sole Proprietorship | Personal tax rate | 15.3% on all profits | Unlimited personal liability |

| LLC | Pass-through | 15.3% on all profits | Limited liability |

| S-Corporation | Pass-through | 15.3% only on salary | Limited liability |

Sole Proprietorship

Operating as a sole proprietorship means you pay self-employment tax (15.3%) on all profits. This tax covers both the employer and employee portions of Social Security and Medicare. However, there’s no separation between your personal and business liabilities, leaving your personal assets exposed.

LLC Benefits

LLCs offer pass-through taxation, meaning profits and losses are reported on the owner’s personal tax return. They also provide limited liability protection, shielding personal assets from business debts. Stephanie Sims explains:

"A partnership is a pass-through entity. That means that the profits or losses pass through to the individual partners and must be reported on their tax returns in that year."

S-Corporation Advantage

An S-Corporation allows you to pay yourself a reasonable salary (taxed as employment income) while taking additional profits as distributions. These distributions are not subject to self-employment tax, potentially lowering your tax obligations. Like LLCs, S-Corps also provide limited liability protection.

Signs You Need a New Business Structure

Here are some reasons to consider changing your business structure:

- Excess Profits Over Reasonable Salary: If your business profits consistently exceed what qualifies as a reasonable salary, switching to an S-Corp could help reduce self-employment taxes.

- Increasing Liability Risks: As your business grows, protecting your personal assets becomes more important. Mark J. Kohler highlights this importance:

"Your business entity can be the most valuable player on your team. It's critical to wisely choose the entity that's best for your business, make changes when necessary, and take advantage of the benefits of your business structure."

- Tax Savings Opportunities: If your profits are high enough to offset the administrative costs of an S-Corp, restructuring might save you money on self-employment taxes.

sbb-itb-08dd11e

Tax Deductions and Credits Guide

First-Year Business Deductions

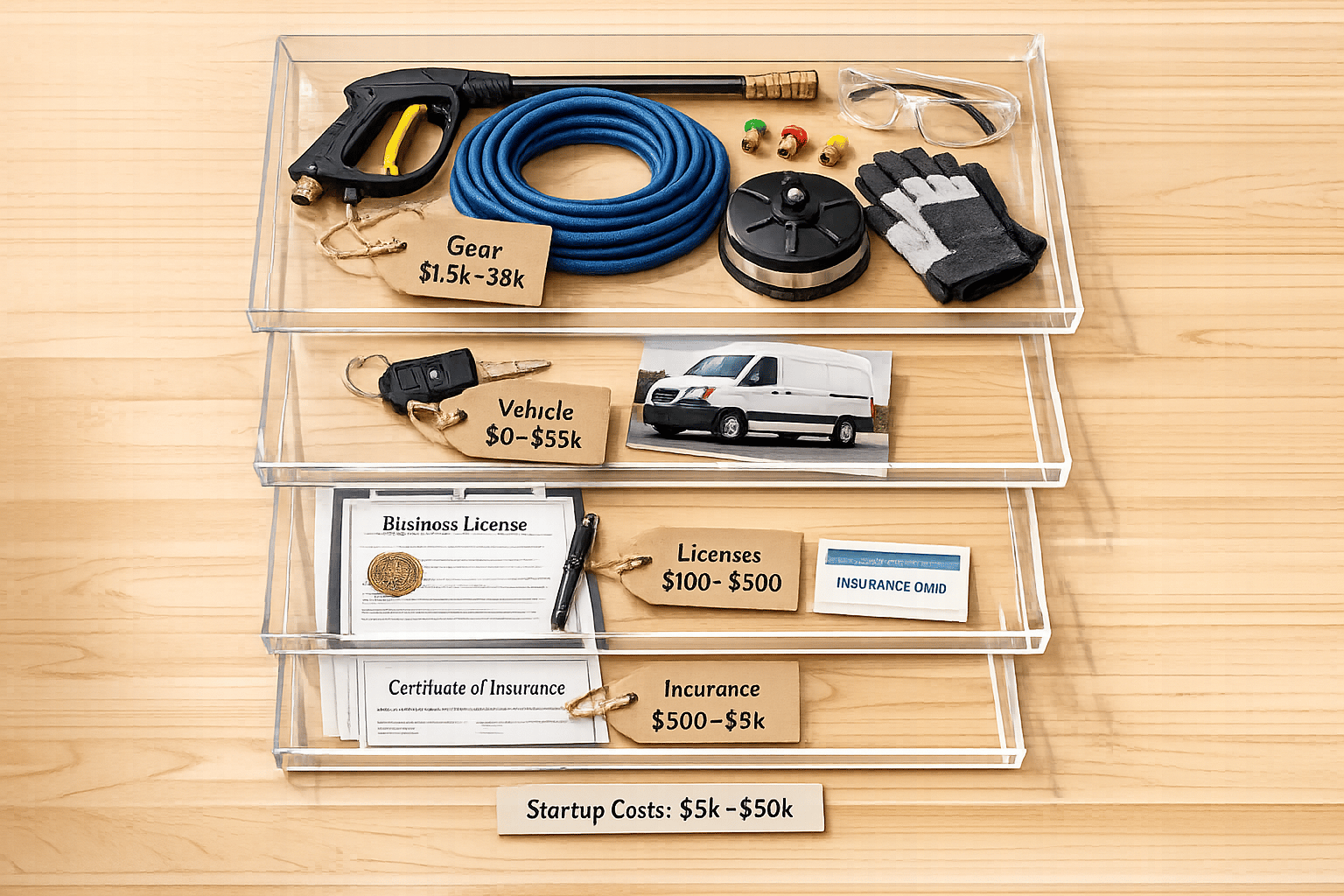

If you're starting a business, you can deduct up to $5,000 in startup costs and $5,000 in organizational costs, as long as your total startup expenses are under $50,000. If your expenses exceed $50,000, the deduction is reduced by the excess amount. For costs over $55,000, you'll need to spread them out (amortize) over 15 years.

Here are some common first-year deductible expenses:

| Expense Category | Deductible Items | Limits/Notes |

|---|---|---|

| Equipment | Computers, printers, furniture | Up to $1,250,000 under Section 179 |

| Professional Services | Legal fees, accounting services | Fully deductible |

| Market Research | Surveys, analysis | Must be incurred before opening |

| Training | Employee training wages | Counted as startup expenses |

| Marketing | Opening advertisements | Counted as startup expenses |

Office and Operating Expense Deductions

Deductions lower your taxable income by accounting for qualifying expenses. For 2024, some key deductions include:

- Vehicle Expenses: $0.67 per mile for business use.

- Business Meals: Deduct 50% of qualifying food and beverage costs.

- Home Office: Deduct a portion of your rent or mortgage and utilities based on the percentage of your home used for business.

- Communications: Business phone and internet costs are deductible.

For example, a self-employed writer in early 2024 reduced their self-employment tax from $8,478 to $7,630 and their income tax from $4,865 to $4,200 by claiming $6,000 in contractor expenses.

While deductions reduce taxable income, tax credits provide a direct reduction in the taxes you owe.

Small Business Tax Credits

Tax credits directly reduce your tax bill dollar-for-dollar. Here are some key credits to consider:

| Tax Credit | Maximum Benefit | Key Requirements |

|---|---|---|

| Health Insurance | 50% of premiums paid | Fewer than 25 full-time employees |

| Work Opportunity | Up to $9,600 per employee | Must hire from eligible groups |

| R&D Activities | 10% of qualifying expenses | Must document research activities |

| Disabled Access | Up to $5,000 | Applies after the first $250 in expenses |

For instance, in 2023, GreenTech Solutions, a company with 20 employees, earned a credit worth 50% of health premiums by covering 60% of those costs.

To make the most of these credits:

- Keep detailed records of all expenses and activities.

- Document research activities with notes and diagrams.

- Work with a tax professional to identify all eligible credits.

- Review qualification requirements annually, as they may change.

Income and Expense Planning

Income Timing Strategies

Adjusting when you receive income or pay expenses can help lower your tax bill. For cash-basis taxpayers, the timing of payments and expenses directly affects your annual tax liability.

Here are some practical timing strategies:

| Timing Strategy | Tax Impact | Tips for Implementation |

|---|---|---|

| Late-Year Invoicing | Shifts income to the next tax year | Send invoices after December 15 |

| Early Expense Payment | Boosts current-year deductions | Pay expenses by December 29–30 |

| Service Prepayment | Adds to current-year deductions | Buy annual subscriptions in December |

| Repair Acceleration | Increases current-year write-offs | Complete repairs by December 31 |

For instance, if you expect to earn $120,000 in December 2025, invoicing on December 28 instead of December 1 moves that income into 2026. This can be particularly helpful if you expect to be in a lower tax bracket next year.

"As the end of the year approaches, it's time for small business owners to put tax planning on their radar. You have until December 31 to make some strategic moves that can help you take advantage of more tax breaks, maximize your tax deductions, and minimize the amount you'll owe when tax filing time comes." - Oregon Small Business Development Center Network

Using tax planning software with real-time projections and AI-driven recommendations can simplify these strategies. Additionally, pairing income timing with equipment purchase planning can further reduce your tax obligations.

Equipment Depreciation Tax Savings

Timing equipment purchases effectively can lead to major tax benefits. When investing in business equipment, you have two key options to maximize savings:

Section 179 Deduction

- Lets you immediately deduct equipment costs.

- Applies to both new and used equipment.

- Requires the equipment to be in service during the tax year.

- Deduction depends on the percentage of business use.

Bonus Depreciation

- Kicks in after Section 179 limits are met.

- Covers long-term capital investments.

- Can be applied to qualified improvement property.

- Lowers your current-year tax liability.

Expense management tools can simplify tracking these purchases and help identify potential depreciation benefits.

To get the most out of these deductions:

- Buy and install equipment by December 31.

- Document the percentage of business use.

- Keep thorough records of purchase dates and costs.

- Align financing terms with your overall tax strategy.

Retirement and Benefits Tax Savings

Solo 401(k) and SEP IRA Tax Benefits

Retirement planning is a smart way to lower taxes while building your financial future. In 2025, business owners can benefit from increased contribution limits and tax perks through Solo 401(k) plans and SEP IRAs.

With a Solo 401(k), you can contribute both as an employee (up to $23,500) and as an employer (up to 25% of your compensation, capped at $70,000). If you're between 60 and 63 years old, the Secure 2.0 Act allows an additional $11,250 catch-up contribution starting in 2025.

Here’s a breakdown of the 2025 contribution limits and tax benefits:

| Retirement Plan Type | 2025 Contribution Limit | Tax Benefit |

|---|---|---|

| Solo 401(k) Basic | $23,500 | Immediate tax deduction |

| Solo 401(k) with Enhanced Catch-up (60–63) | $34,750 | Reduced taxable income |

| Solo 401(k) Employer Portion | Up to $70,000 | Business tax deduction |

| SEP IRA | 25% of compensation | Immediate tax write-off |

If you're setting up a 401(k) plan for the first time, you could qualify for up to $16,500 in tax credits to cover startup costs. Providers like ShareBuilder 401k offer services at rates up to 68% lower than the industry average.

Additionally, other benefit options like Health Savings Accounts (HSAs) can further reduce your tax obligations.

HSA Tax Advantages

HSAs offer a powerful triple tax benefit: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified expenses are also tax-free. For 2025, the contribution limits are $4,300 for individual coverage, $8,550 for family coverage, with an extra $1,000 allowed for those aged 55 and older.

To get the most out of an HSA, consider these steps:

- Enroll in an HSA-eligible high-deductible health plan.

- Set up pre-tax payroll contributions.

- Keep detailed records of expenses.

- Deposit contributions within 90 days.

The tax treatment of HSA contributions depends on your business structure. For example:

- C Corporations: Owners are treated as employees, allowing for pre-tax contributions.

- S Corporations: Owners with 2% or more ownership face restrictions on tax-free contributions.

- LLCs: Pre-tax HSA contributions can be offered through a cafeteria plan.

Employers can also save roughly 15.3% in FICA taxes when contributions are made as both employer and employee.

Providers like Fidelity HSA® make it easier to implement these strategies, offering $0 account fees and no minimum balance requirements. This approach not only helps reduce taxable income but also aligns well with broader tax planning goals.

Summary and Next Steps

Reducing your tax burden requires careful planning and attention to detail. According to research, 90% of business owners overpay taxes due to overlooked write-offs. Here are some key strategies to help you avoid that mistake:

The Small Business Administration reports that the average effective tax rate for small businesses is 19.8%. To lower this percentage, consider the following:

- Reassess Your Business Structure

Evaluate whether your current structure is tax-efficient. For example, switching from a sole proprietorship to an S corporation can reduce self-employment taxes. A tax professional can guide you through this process legally and effectively. - Track Deductions and Credits

Keep detailed records of all business expenses to ensure you're maximizing deductions."Make sure you're deducting all the legitimate business expenses available to you and keeping thorough records of them. If in doubt, consult your CPA."

- Plan Ahead for 2026

Prepare for upcoming changes in estate and gift tax exemptions after December 31, 2025."With changes in estate and gift tax exemptions coming after December 31, 2025, you may also want to consider ways of transferring more of your business out of your estate."

| Action Item | Deadline | Potential Benefit |

|---|---|---|

| File Form 8850 | Within 28 days of hiring | Work Opportunity Tax Credit |

| Asset placement for depreciation | December 31, 2025 | Current year tax deduction |

| Estimate net income | Quarterly | Optimize deductions and credits |

| Bad debt write-offs | End of fiscal year | Reduced taxable income |

These practical steps can significantly reduce your tax obligations. To refine your approach, seek expert advice tailored to your business.

Professional Support

In addition to internal strategies, professional expertise can amplify your savings. On average, small businesses spend over 40 hours annually on federal taxes alone. Tax professionals offer valuable services, such as:

- Designing tax-efficient employee benefits

- Pinpointing deductions specific to your industry

- Staying on top of complex tax law changes

- Structuring transactions to minimize tax impact

Start implementing these strategies today to ensure a leaner tax bill in the next fiscal year.

Related Blog Posts

Get the newest tips and tricks of starting your business!