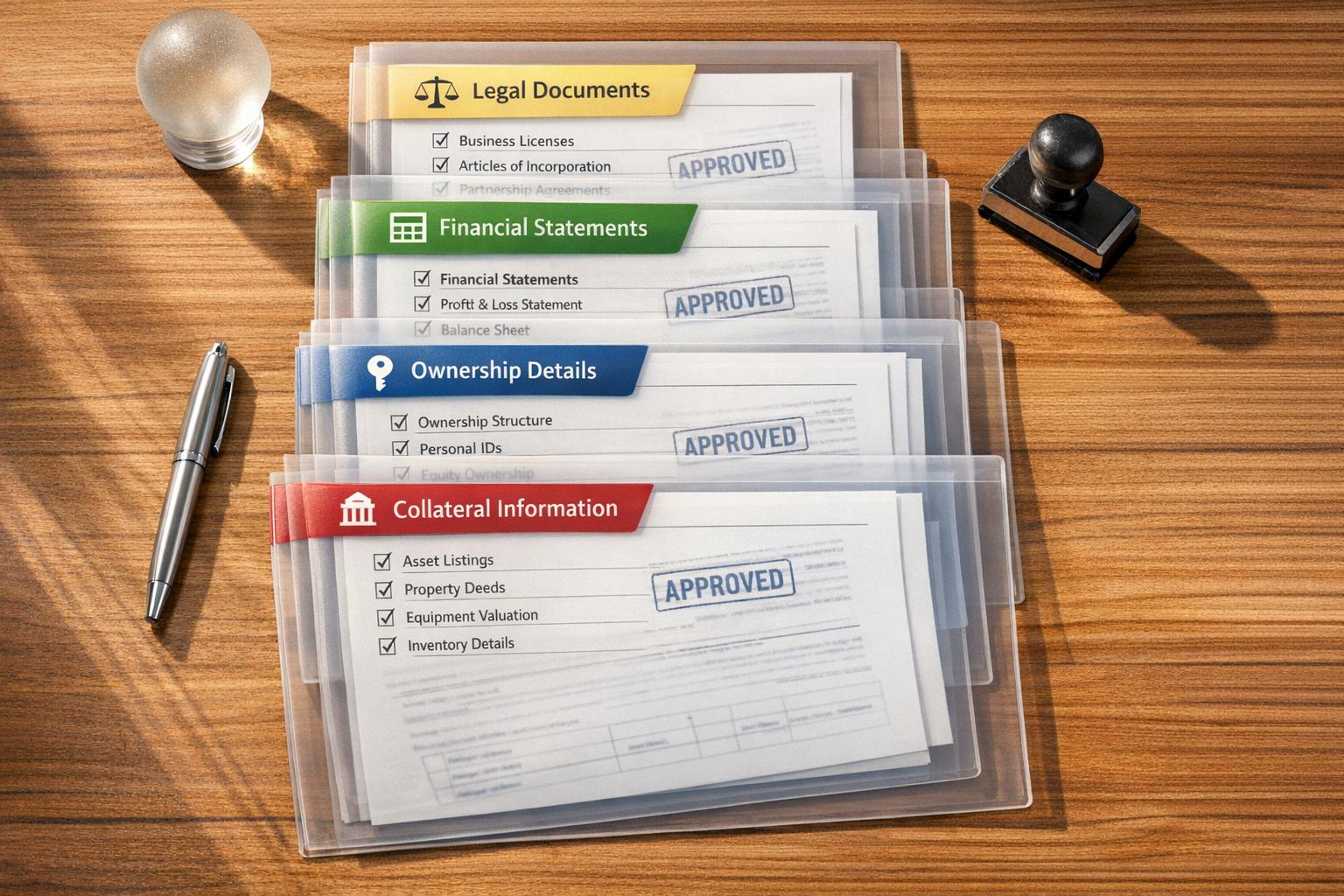

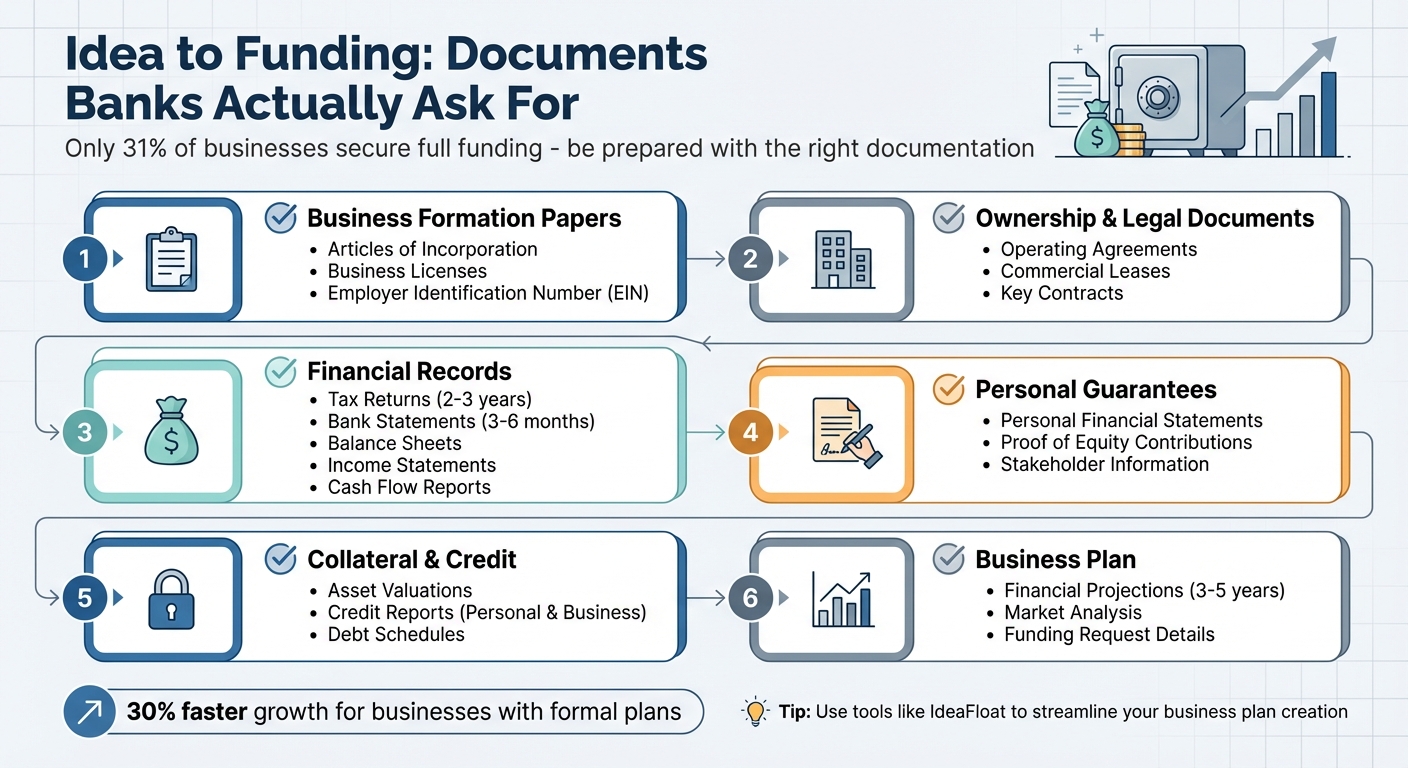

Walking into a bank for funding? Be prepared. Banks want proof that your business can repay the loan. Here's the bottom line: you need the right documents to show financial stability and credibility.

Key documents banks typically require include:

- Business formation papers: Articles of Incorporation, business licenses, and EIN.

- Ownership and legal documents: Operating agreements, commercial leases, and key contracts.

- Financial records: Tax returns, bank statements, balance sheets, income statements, and cash flow reports.

- Personal guarantees: Financial statements for stakeholders and proof of equity contributions.

- Collateral and credit verification: Asset valuations, credit reports, and debt schedules.

- Business plan: A clear roadmap with financial projections, market analysis, and funding requests.

Each document supports your case, showing lenders that you're organized, transparent, and capable of repayment. Banks assess factors like cash flow, debt ratios, and collateral value to minimize risk. Only 31% of businesses secure full funding, so thorough preparation is key.

Use tools like IdeaFloat to streamline your business plan creation and ensure every detail aligns with lender expectations. The better prepared you are, the stronger your loan application will be.

Essential Documents Banks Require for Business Loan Applications

Key documents you should prepare when you’re ready for a loan

Business Formation Documents

Before a bank even glances at your financials, they need to confirm that your business is legally established. These formation documents serve as proof that your business operates within the bounds of federal, state, and local laws. Without them, your loan application won't get off the ground. Take a moment to review these documents to ensure they meet the bank's requirements.

Articles of Incorporation and Business Licenses

Your Articles of Incorporation (or Articles of Organization for LLCs) are the cornerstone of your business's legal existence. Filed with your state's Secretary of State, this document includes essential details like your company name, business purpose, number and value of shares, and the names of directors and officers. It's a fundamental step in establishing your business's legitimacy.

Once your business is officially recognized, it's crucial to ensure all necessary licenses and permits are current. Banks require up-to-date business licenses and permits to confirm you're legally authorized to operate in your area. These are typically issued at the city or county level and are separate from your state registration. Expired licenses can raise red flags and derail your loan application, so double-check their validity.

If your business operates in states beyond where it was incorporated, you'll need a Certificate of Authority (also known as "foreign qualification") for each additional state. This document assures banks that you're compliant with regulations in all the states where you conduct business.

Employer Identification Number (EIN)

Think of your EIN as your business's equivalent of a Social Security number. This nine-digit federal tax ID, issued by the IRS, is used to verify your business identity and cross-check your tax returns. You'll need an EIN to open business bank accounts and to provide consistency across your financial records.

Banks rely on your EIN to ensure your tax returns match up with other financial documents, helping to prevent fraud. Keep your EIN confirmation letter from the IRS handy - it’s a key piece of documentation.

Operating Agreements or Franchise Agreements

For LLCs, banks will ask for operating agreements, and for partnerships, they’ll request partnership agreements. These documents outline ownership stakes, voting rights, and management structures - details that help banks evaluate who controls the business and who has the authority to apply for funding. This information plays a critical role in assessing your business's "Character" and "Capacity".

If you're part of a franchise, your franchise agreement is also essential. It details your relationship with the franchisor, including fee structures, operational guidelines, and contract terms. This helps banks gauge any external obligations that could impact your cash flow or loan repayment ability.

Make sure these agreements are up to date and accurately reflect your current ownership structure. Outdated documents can cause delays in the approval process. If you have multiple partners, you may also need to provide a letter stating who has the legal authority to enter into loan agreements on behalf of the business.

Legal and Ownership Documents

Once your business is legally established, banks will closely examine ownership and financial commitments to assess potential risks. These documents provide insights into your business’s structure and help lenders evaluate whether existing obligations could affect your ability to repay a loan.

Commercial Lease Agreements and Key Contracts

A commercial lease agreement confirms your business location and outlines fixed monthly expenses. Banks review these terms to understand how much of your cash flow is tied up in rent and to evaluate your ability to relocate if necessary. For home-based businesses or less formal setups, be sure to provide clear documentation of your arrangement.

Key contracts with major customers and suppliers are equally important. Customer contracts can sometimes be used as collateral, typically valued at 50% to 75% of their face value. Supplier agreements, on the other hand, can serve as credit references. Highlight any long-term contracts that guarantee consistent revenue, as they demonstrate financial stability and reduce perceived risk.

These documents, alongside proof of legal formation, give banks a clearer picture of your ongoing financial commitments. Additionally, the expertise and reliability of your team play a critical role in the bank's decision-making process.

Resumes of Owners and Key Personnel

Banks aren’t just investing in your business - they’re also investing in the people running it. Resumes of key personnel provide a window into the management team’s experience and reliability, which is especially important for startups with limited financial track records.

"Character reflects your credit history and reputation." - US Chamber of Commerce

Make sure your resume highlights industry-specific experience, notable achievements, and any qualifications that reinforce your credibility. If you or your team members hold specialized roles, include relevant certifications or training to strengthen your case.

Personal Guarantees for Major Stakeholders

In many cases, major stakeholders must sign a personal guarantee, making them personally responsible for the loan if the business cannot repay it. Banks view this as a sign of commitment to the venture; hesitance to pledge personal assets may raise concerns about the business’s risk level.

"If you don't believe in your business, then we don't, either." - Tim Berry, Founder, Palo Alto Software

Be prepared to submit personal financial statements showing your assets, liabilities, and income. In some instances, banks may request additional collateral, such as home equity, or require life insurance policies on key founders, naming the bank as the beneficiary. These measures help protect the lender in case of unforeseen circumstances.

Financial Documents Banks Require

When applying for a business loan, banks don’t just rely on legal paperwork or personal guarantees - they need solid financial data to assess whether your business can realistically repay the loan. These documents provide insight into your financial health, cash flow, and existing obligations, offering a comprehensive snapshot of your business's financial standing.

Tax Returns and Bank Statements

Banks usually ask for 2–3 years of personal and business tax returns to confirm your income history and ensure consistency with IRS records. This helps verify your income trends and ensures that your financial reporting is accurate.

In addition, you’ll need to submit 3–6 months of business bank statements, though some lenders may require up to a year’s worth. These statements reveal how money flows in and out of your business, helping banks validate your reported revenue and spot potential red flags like overdrafts or irregular transactions. This is the first step in building a strong financial profile for your loan application.

Balance Sheets, Income Statements, and Cash Flow

Three critical financial statements form the foundation of your loan application:

- Balance Sheet: This provides a snapshot of your assets, liabilities, and net worth at a specific point in time. Lenders focus on ratios like your current ratio (to assess liquidity) and debt-to-equity ratio (to gauge solvency).

- Income Statement: Covering the past three years, this document shows your revenue trends and how well you manage expenses.

- Cash Flow Statement: This reveals how much cash you have on hand, which is crucial since even profitable businesses can struggle if they lack liquidity.

"There's no better way to gauge your financial health than a financial statement." - Kirsch CPA Group

For added credibility, consider having a CPA prepare reviewed or audited financial statements. While compiled statements are formatted correctly, reviewed ones provide limited assurance of their accuracy, and audited statements offer the highest level of verification. Stronger documentation can improve your chances of securing larger loans and demonstrates professionalism to lenders.

Debt Schedules and Accounts Receivable

Banks also require a debt schedule, which lists all your current and past loans, credit card accounts, and other financial obligations. This helps them calculate your total debt-to-income ratio and evaluate your ability to take on additional debt. Be sure to include all relevant accounts, such as bank accounts, investment accounts, and notes payable.

Your Accounts Receivable (AR) report is another key document. It outlines who owes you money and when payments are expected. Banks often review detailed aging reports, which break down invoices by how long they’ve been outstanding, to ensure your customers are reliable and likely to pay. If you’re using receivables as collateral, keep in mind that banks generally only accept 50% to 75% of their total value, excluding invoices tied to customers with poor credit or overdue balances.

"Banks look very carefully at these assets to make sure they reduce the risk." - Tim Berry, Founder, Palo Alto Software

Lastly, provide a clear monthly cash flow forecast for at least the next 12 months to show how you plan to manage future repayment. Since only 31% of businesses secure full financing, thorough and accurate documentation can make all the difference.

sbb-itb-08dd11e

Business Plan: A Required Document

Financial statements may show where your business stands today, but a solid business plan maps out where you're headed. A well-thought-out business plan not only demonstrates that your idea is feasible but also outlines the steps to make it successful. It connects your financial history with future projections, giving lenders a clear picture of your strategy and goals.

In fact, founders with formal business plans grow their businesses 30% faster. These plans show lenders that you understand your market, your competition, and how to use loan funds effectively to drive revenue growth. They also prove that you can repay the loan while maintaining key financial metrics. For banks, this document is a crucial tool to evaluate your ability to meet financial obligations.

"A business plan can also help you to attract potential lenders, investors and partners by providing them with evidence that your business has all the ingredients necessary for success." - Bank of America

Think of your business plan as a financial roadmap. It should tie your funding request to specific outcomes, like purchasing equipment or upgrading technology, which directly impact your operations and repayment ability. This level of detail is critical, especially when only 31% of businesses secure the full financing they request.

Key Components of a Bank-Ready Business Plan

A bank-ready business plan typically spans 15–20 pages and follows a structured format that lenders expect. Each section is designed to showcase your business as a reliable investment while complementing the financial and legal documents you provide.

- Executive Summary: A brief overview (3–5 paragraphs) that highlights your business concept, goals, products or services, and financial needs.

- Company Description: Explains your legal structure, business history, and the customer problems you aim to solve.

- Market Analysis: Includes industry trends, target market insights, and a SWOT analysis to show how you’ll outperform competitors.

- Organization and Management: Features an organizational chart and bios of key team members, emphasizing their relevant experience.

- Service or Product Line: Describes the product lifecycle, customer benefits, and any intellectual property like patents or trademarks.

- Marketing and Sales Strategy: Details how you’ll acquire customers - via social media, partnerships, retail channels, etc. - along with specific costs.

- Funding Request: Clearly states the amount of funding needed over the next five years, breaking down how the funds will be used.

- Financial Projections: Provides 3–5 years of projections, with monthly or quarterly details for the first year. Include forecasted income statements, balance sheets, and cash flow statements. Be realistic - lenders can spot overly optimistic figures.

- Appendix: Includes supporting documents such as credit histories, licenses, permits, letters of reference, and key customer contracts.

"If you don't believe in your business, then we don't, either." - Bank representative to Tim Berry, Founder of Palo Alto Software

Using IdeaFloat to Create Your Business Plan

If creating a business plan feels overwhelming, IdeaFloat’s Business Plan Generator simplifies the process with step-by-step instructions and AI-powered tips.

- Smart Market Sizing: Calculates your Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) with reliable data, speeding up your research.

- Financial Projections & Breakeven Analysis: Generates accurate, month-by-month revenue and cost projections. Interactive graphs help you visualize when your business will reach profitability.

- Advanced Pricing Research: Uses AI to analyze market pricing and recommend strategies, ensuring your revenue forecasts are realistic and aligned with market conditions.

- Export Options: Produces a polished, professional business plan in PDF, Word, or PowerPoint formats. It can also create a Lean Canvas - a concise, one-page summary perfect for early-stage discussions.

IdeaFloat’s AI even adjusts the tone of your writing to match lender expectations, whether you need a professional, persuasive, or academic style. It ensures your business plan speaks the language banks want to hear while keeping your voice intact. Plus, the platform may suggest additional revenue opportunities, helping you craft more robust financial forecasts.

With tools like these, you can create a business plan that not only supports your funding application but also positions your business for long-term success.

Collateral and Credit Verification Documents

When applying for a business loan, banks need assurance that they can recover their investment if your business faces financial trouble. This is where collateral and credit verification documents come into play. These materials help lenders evaluate their risk by examining what assets you can offer as security and your credit history. Together, they provide a clearer financial picture, complementing the details in your business plan and formation documents.

Collateral Valuation and Proof of Ownership

Collateral can include a variety of assets such as real estate, equipment, inventory, accounts receivable, and liquid assets like cash, stocks, or bonds. Banks use a Loan-to-Value (LTV) ratio to determine how much they’re willing to lend against these assets, often capping loans at 75% or less of the appraised value. For accounts receivable, lenders might only finance 50% to 75% of the verified amount.

To support your application, you’ll need to provide documentation like property tax assessments, mortgage statements, vehicle titles, business licenses, or articles of incorporation. Liquid assets are especially attractive to lenders since they’re easier to convert into cash. On the other hand, specialized equipment or outdated inventory may be appraised at a lower value. When you use collateral, you’ll typically sign a lien agreement, often filed as a Uniform Commercial Code (UCC) filing, which gives the lender the right to seize the asset if you default.

"The valuation also considers how easy it is to liquidate an asset. For example, a lender can quickly sell off stocks or bonds while selling a specific type of inventory may take longer to offload."

Personal and Business Credit Reports

Lenders rely heavily on credit reports to gauge whether you’re likely to repay your loan. Both personal and business credit histories are reviewed. Personal credit scores fall between 300 and 850, while business credit scores range from 0 to 100. Unlike personal credit reports, business credit reports are publicly accessible for a fee. These credit evaluations play a key role in the overall risk analysis, complementing your financial documents and business plan.

Be mindful when submitting applications. Each full application results in a "hard pull" on your credit, which can lower your score slightly. To avoid unnecessary hits to your credit, research lenders carefully and apply only to two or three that align with your profile. Additionally, ask whether the lender uses a hard or soft pull during the initial stages. Even if you operate as a corporation, banks may require significant stakeholders to sign personal guarantees, linking their personal assets to the business loan.

"Good credit won't just make getting a loan easier - it can help you secure better financing rates, better insurance rates and better terms from vendors."

- Baylee Patel, Author, OnDeck

Equity Contribution and Loan Applications

Banks also expect you to contribute equity directly to the business as a sign of your commitment and to reduce their risk. Alongside your financial statements, a verified equity contribution strengthens your application by showing you have a personal stake in the venture.

To verify your equity contribution, provide documents such as personal financial statements, bank statements, and income tax returns for both personal and business finances. You’ll also need to disclose any existing loans and provide proof of where your equity originated, such as savings account records or 401(k) withdrawal statements. This transparency allows lenders to calculate your debt service coverage ratio (DSCR) accurately. For instance, if your debt-to-income ratio exceeds 43%, lenders may view you as high-risk. Ownership and legal documents, such as shareholder or partnership agreements, further clarify each owner’s financial stake.

"In the case of startups, the financial standing of the owner or owners is especially important. You should be prepared to provide detailed personal financial statements, including assets, liabilities, and sources of income."

Conclusion: Preparing Your Loan Application

Getting approved for bank funding requires more than just filling out forms - it’s about presenting a well-organized, accurate picture of your business’s potential. Lenders sift through hundreds of applications, and only 31% of businesses secure the full amount they request. To stand out, your documentation must be complete and well-prepared. Every piece, from business formation papers and financial statements to collateral valuations and credit reports, plays a role in telling your story. The way you present this information can make or break your application.

Start by grouping your documents into three main categories:

- Personal: Includes items like government-issued ID and personal tax returns.

- Business: Covers essentials such as your EIN, articles of incorporation, and licenses.

- Financial: Includes profit and loss statements, financial projections, and similar records.

It’s crucial to ensure all details are consistent across documents. If you have existing debts, tax liens, or legal issues, disclose them upfront. Surprises during underwriting can derail your application, as lenders may see omissions as red flags.

"Being transparent, organized, and realistic about your finances not only helps you make a stronger case but also signals to lenders that you're a responsible and strategic business owner."

- US Chamber of Commerce

Your business plan is the cornerstone of your application. To make it impactful, keep it focused. Begin with a concise executive summary (one to two pages) and move detailed data to an appendix. Back up your financial forecasts with solid market research, and ensure your projections are achievable, not overly ambitious. Tools like IdeaFloat simplify this process, offering a Business Plan Generator that creates lender-ready documents with accurate financial projections, market insights, and professional formatting. You can export these as PDF, Word, or PowerPoint files, saving hours of formatting work.

When applying for loans, limit yourself to 2–3 lenders to avoid multiple hard credit checks, which can lower your credit score. Always ask for the Annual Percentage Rate (APR) to compare the total cost of different loan options, including fees. Additionally, review loan covenants carefully to understand any financial ratios or requirements you’ll need to maintain after funding. By preparing thoroughly and using the right tools, you’ll be ready to submit a polished, complete application that meets every bank’s expectations.

FAQs

What financial documents do banks usually require when applying for a business loan?

When you're applying for a business loan, banks usually require a handful of important financial documents. These often include complete financial statements, such as profit and loss statements and balance sheets. Ideally, these should be audited or reviewed for added credibility. Lenders will also typically ask for business tax returns from the past two to three years. Additionally, you may need to submit a debt schedule that details any current loans or financial obligations your business has.

To make your application stand out, ensure that all documents are accurate, current, and professionally organized. This not only reflects your business’s financial stability but can also boost your chances of getting the funding you need.

What should I include in my business plan to meet bank requirements?

To secure a loan from a bank, your business plan needs to clearly highlight your company’s financial stability, growth prospects, and repayment ability. Include key financial documents such as balance sheets, income statements, and cash flow reports to showcase your company’s performance and reliability.

Additionally, provide a concise summary of your business operations, market strategy, and a detailed explanation of how the loan will be used. If collateral is required, make sure to include relevant documentation. Focus on presenting realistic financial projections and emphasizing your company’s strengths to make a compelling case and improve your chances of approval.

How does your personal credit impact your chances of getting a business loan?

Your personal credit is a key factor when it comes to getting approved for a business loan. Banks and lenders look at your credit score and history to evaluate how financially reliable you are and to determine the risk of lending to you. A solid credit profile can signal responsible financial habits, boosting your chances of approval.

For newer businesses or those without a credit history, lenders tend to place even more weight on your personal credit. To strengthen your position, make sure your credit report is free of errors, pay off any outstanding debts, and keep your credit utilization ratio at a healthy level.

Related Blog Posts

Get the newest tips and tricks of starting your business!