Setting up your business legally in the U.S. is simpler than it seems. In just three steps, you can get your venture off the ground without unnecessary complexity or expense. Here's the process:

- Choose the Right Business Structure

Decide between sole proprietorship, partnership, LLC, or corporation based on liability, taxes, and growth plans. Most new entrepreneurs prefer LLCs for their balance of protection and simplicity. - Get an EIN (Employer Identification Number)

Apply on the IRS website for free. This number is essential for taxes, opening a business bank account, and hiring employees. - Understand and Register for Sales Tax

Determine where you need to collect sales tax based on your location, sales volume, and customer base. Rules vary by state, so research is crucial.

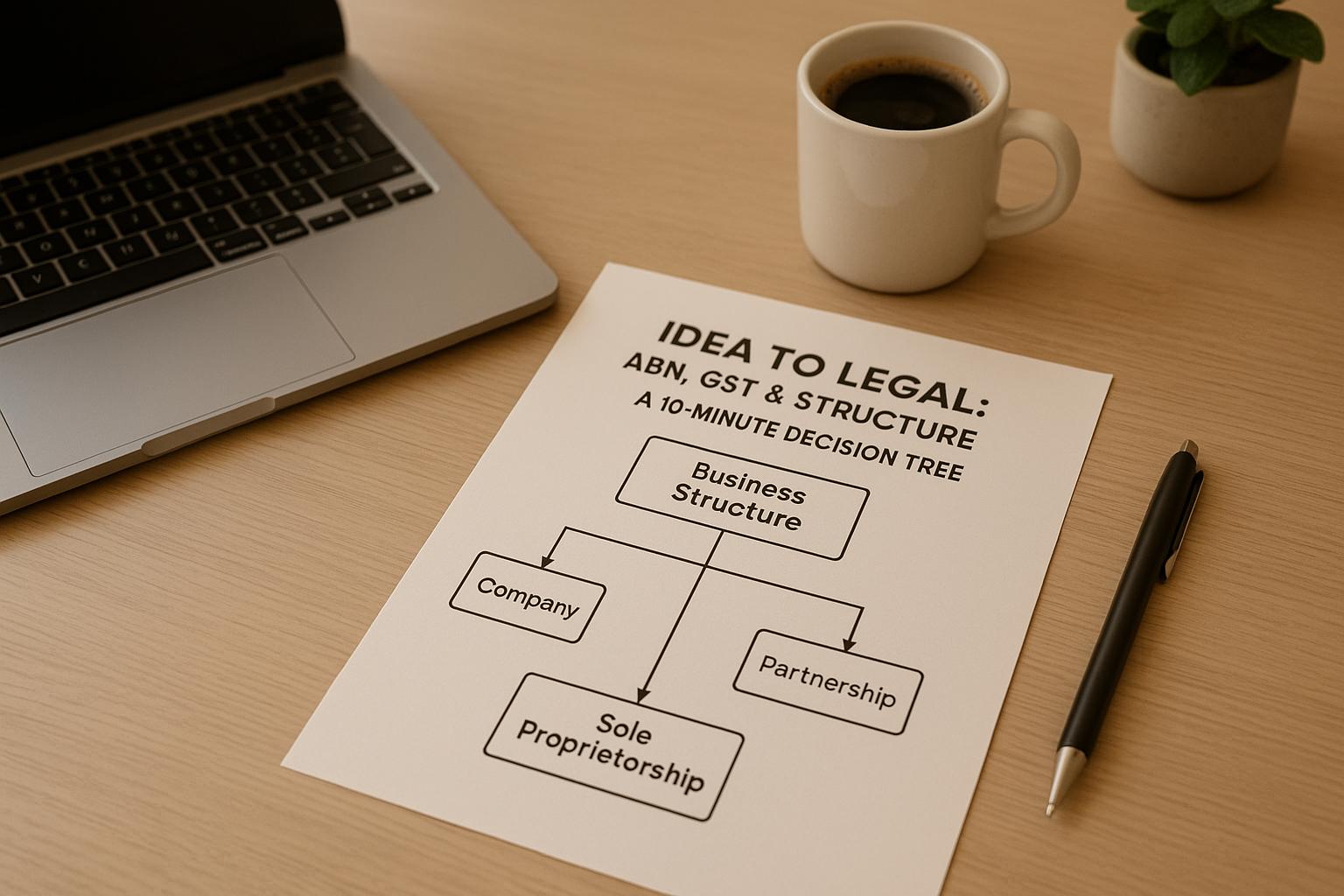

Choosing Your Business Structure: Expert CPA Advice on LLC, S-Corp, and More

Step 1: Pick Your Business Structure

The structure of your business plays a big role in determining your personal liability, tax obligations, and the paperwork you'll need to manage. To make the right choice, ask yourself three key questions: Do you need liability protection? Are you partnering with others? What are your plans for raising investment?

Business Structure Options

Sole Proprietorship is the easiest and most straightforward option. It doesn’t require formal registration, and you and your business are considered the same legal entity. However, this also means you’re personally responsible for any debts or legal issues tied to the business. Income is reported on your personal tax return using Schedule C. This setup is ideal for freelancers, consultants, and small service providers who aren’t worried about liability risks.

Partnership is for businesses owned by two or more people. Partners share personal liability for the business’s debts. While the business itself files an informational tax return, profits and losses are reported on the partners’ personal tax returns. General partnerships form automatically when two or more people do business together, even without formal agreements. That said, drafting a partnership agreement is always a smart move.

Limited Liability Company (LLC) offers liability protection while keeping the tax benefits of a partnership. Your personal assets are generally safe from business debts and legal claims. Most states allow single-member LLCs, making this a great option for solo entrepreneurs who want liability protection without too much complexity.

Corporation creates a separate legal entity distinct from its owners. Shareholders benefit from strong liability protection, but corporations come with more complex tax rules and regulatory requirements. C-Corporations pay corporate income taxes, and shareholders are taxed again on dividends (double taxation). S-Corporations, on the other hand, avoid double taxation by passing profits directly to shareholders’ personal returns. However, S-Corps are limited to 100 shareholders and cannot include foreign investors.

How to Choose the Right Structure

Start by considering liability. If your business involves high financial risks or the potential for lawsuits, an LLC or corporation is the safer choice. For example, software companies, manufacturers, or businesses handling sensitive customer data often need liability protection. On the other hand, service providers with low risk may find a sole proprietorship sufficient at first.

Next, think about taxes. S-Corporations can help reduce self-employment taxes by allowing owners to take part of their income as distributions instead of wages - but you’ll need to pay yourself a reasonable salary first.

Finally, evaluate your growth and funding plans. Corporations are better suited for attracting investors, offering stock options, and eventually going public. Venture capital firms often prefer C-Corporations for these reasons. If you’re building a smaller, self-funded business, an LLC typically offers more flexibility and fewer operational demands.

If you’re working with business partners, LLCs provide more flexibility than partnerships when it comes to profit sharing, management responsibilities, and adding new members. Corporations, while more structured, require formal governance like boards of directors and regular meetings. These decisions will also influence your EIN application and compliance down the road.

Business Structure Comparison

| Structure | Liability Protection | Tax Treatment | Setup Complexity |

|---|---|---|---|

| Sole Proprietorship | None - personal liability | Personal tax return | Minimal |

| Partnership | None - personal liability | Pass-through to partners | Low |

| LLC | Strong protection | Pass-through (or corporate) | Moderate |

| S-Corporation | Strong protection | Pass-through | High |

| C-Corporation | Strong protection | Double taxation | High |

For most new entrepreneurs, an LLC strikes the right balance between protection, flexibility, and simplicity. If your business grows and you need to raise capital or offer equity to employees, you can convert to a corporation later. This process is straightforward and won’t disrupt your operations.

Step 2: Get Your EIN (Employer Identification Number)

Once you've decided on your business structure, the next step is to secure an Employer Identification Number (EIN) from the IRS. Think of it as your business's version of a Social Security number. This nine-digit number is essential for opening bank accounts, filing taxes, and more. Let’s break down why you need it and how to get it done quickly.

Why You Need an EIN

An EIN is vital for identifying your business with the IRS, banks, and other organizations. Even if you're a sole proprietor, having an EIN offers significant benefits. For starters, it separates your personal Social Security number from your business activities, protecting your privacy and reducing the risk of identity theft.

You'll also need an EIN to open a business bank account. Without one, you’ll end up mixing personal and business finances, which can lead to headaches during tax season. Plus, it makes your business appear more professional to vendors and clients.

If you plan to hire employees, work with contractors, or bring on business partners, an EIN is non-negotiable. The IRS requires it for managing payroll taxes, unemployment insurance, and worker's compensation. Even if you’re paying a freelancer more than $600 a year, you’ll need an EIN to file 1099 forms.

For LLCs, corporations, and partnerships, an EIN is a must-have. The IRS treats these entities as separate from their owners for tax purposes, so an EIN is required even if you don’t have employees.

How to Apply for an EIN Online

Now that you know why an EIN is important, here’s how to get one quickly. The fastest and easiest way is through the IRS website at irs.gov. The online application takes about 15 minutes, and you’ll receive your EIN immediately upon approval - no waiting for mail or phone processing.

Before you start, gather the necessary details. You’ll need your Social Security number or Individual Taxpayer Identification Number (ITIN) as the responsible party. The responsible party is the individual who controls and manages the business, so choose carefully - this designation isn’t easy to change later. You’ll also need your business name, address, and the reason for applying for an EIN.

Be ready to specify your business structure, as this determines your tax obligations and filing requirements. For example, if you set up an LLC, you’ll need to decide whether it will be taxed as a sole proprietorship, partnership, or corporation.

Here are a few key tips for a smooth application process:

- Avoid duplicate EIN applications. The IRS considers applying for multiple EINs for the same business as fraudulent.

- Match your business name. Use the exact legal name you registered with your state. If you’re forming an LLC or corporation, complete your state registration first, then apply for the EIN.

- Submit only one application per day. The IRS limits EIN applications to one per responsible party per day. If you make a mistake or the system times out, you’ll need to wait until the next business day to try again.

Once your application is approved, print and save your EIN confirmation immediately. Banks and other institutions often require this document as proof, and the IRS doesn’t automatically send you a copy later.

If you’re an international applicant or don’t have a Social Security number, you’ll need to apply by mail or fax, which can take 4–6 weeks to process. But for most U.S.-based businesses, the online process is quick and straightforward, wrapping up in just 15 minutes.

sbb-itb-08dd11e

Step 3: Understand Sales Tax Requirements

Now that you’ve sorted your structure and secured your EIN, it’s time to tackle sales tax - a tricky but crucial part of staying compliant. Unlike federal taxes, sales tax rules differ wildly from state to state. Missteps here can lead to hefty fines or back-tax bills that could seriously hurt your business. Let’s break this down so you can avoid costly mistakes and stay on the right side of the law.

What Is Sales Tax and Who Needs to Collect It?

Sales tax is a consumption tax that businesses collect from their customers and pay to the government. But here’s the catch: the rules around rates, taxable items, and registration requirements depend on both your business location and where your customers are.

The 2018 Supreme Court ruling in South Dakota v. Wayfair introduced economic nexus rules. This means you may need to collect sales tax in states you’ve never even visited. Most states require registration once your sales hit $100,000 or 200 transactions in a calendar year. But thresholds vary - California sets the bar at $500,000 in sales, while Texas uses the same dollar limit but doesn’t factor in transaction count.

If you’re in a service-based business, don’t assume you’re off the hook. Digital products, software subscriptions, and some professional services are taxable in many states. For example, Texas taxes data processing services, while Washington applies sales tax to digital goods like e-books and streaming services.

For product sellers, the rules can be even more complicated. Tax rates and exemptions vary widely. Clothing might be tax-free in some states but fully taxable in others, and while many food items are exempt or taxed at reduced rates, prepared foods usually face full taxation.

Sales Tax Registration Decision Guide

Figuring out whether you need to register for sales tax depends on where you sell, what you sell, and how much you sell. It’s not just about where your business is located - it’s about where your customers are, too.

| Business Scenario | Registration Needed? | Key Considerations |

|---|---|---|

| Online retailer shipping nationwide | Likely in multiple states | Monitor state thresholds; some require pre-sale registration |

| Local service business (plumbing, consulting) | Depends on state and service type | Check if your services are taxable; some states exempt professional services |

| Software-as-a-Service (SaaS) company | Yes, in most states with customers | Many states tax digital products; nexus thresholds apply |

| Physical retail store | Yes, in state of operation | Register before opening; may need local permits too |

| Marketplace seller (Amazon, Etsy) | Varies by platform and state | Some platforms collect tax for you; others don’t |

Even if you sell through an online marketplace, you can’t assume they’ll handle everything. Many platforms do collect tax under marketplace facilitator laws, but you’re still responsible for tracking sales and monitoring thresholds in each state. If you wait too long to register after hitting a threshold, you could face penalties. Some states even require registration before your first taxable sale.

How to Register and Stay Compliant

Once you’ve determined where you need to register, it’s time to get started. Sales tax registration happens at the state level, and each state has its own process. Most states allow online registration through their Department of Revenue website, but processing times can vary from immediate approval to several weeks.

Start with your home state if you have a physical presence there. You’ll need your EIN, business formation documents, and details about your products or services. Some states may also ask for a security deposit, especially if you’re in a high-risk industry or have no prior business history.

Be prepared for ongoing filing requirements. Depending on your sales volume, you may need to file monthly, quarterly, or annually. Even if you don’t owe any tax, you still have to file returns - skipping this can lead to penalties.

Keep precise records and manage exemption certificates. You’ll need detailed records of all sales, including customer locations, tax collected, and any exempt sales. If a customer claims a tax exemption, make sure you collect and store their resale or exemption certificates. Missing or invalid certificates can leave you on the hook for unpaid taxes, plus penalties and interest.

Stay updated on rate changes and new laws. Sales tax rates can change frequently, sometimes quarterly. New nexus laws are also evolving. Set up alerts from state revenue departments or use automated tools to ensure you’re always charging the right rates.

Getting ahead of your sales tax obligations will save you headaches and protect your business from financial trouble. Register early, stay organized, and don’t let this become a problem that snowballs out of control.

Step 4: Stay Compliant and Plan for Growth

Once you’ve established your business structure, obtained your EIN, and sorted out your sales tax, it’s time to wrap up your legal setup with a few final steps. These will ensure your business is on solid legal ground and ready to grow.

Open a Business Bank Account

Keeping your personal and business finances separate isn’t just a good idea - it’s crucial. It protects your personal assets and makes tax reporting much easier. To open a business bank account, you’ll usually need your EIN and proof of business formation. Choose an account that aligns with your business needs. A dedicated business account simplifies bookkeeping and helps you build credit for your business.

Keep Records and File on Time

Good record-keeping isn’t just about staying organized - it’s about protecting your finances and staying on the right side of tax laws. Keep track of receipts, invoices, bank statements, and payroll records. Digital tools can make organizing these much easier. Also, stay on top of filing deadlines to avoid penalties. While you can file for extensions, remember that any taxes owed will still accrue interest and fines if not paid on time.

Once you’ve got your compliance tasks under control, you can shift gears and start focusing on strategies to grow your business.

Use IdeaFloat for Growth and Compliance

With your legal groundwork in place, the next step is transforming your compliant business into a profitable one. Many entrepreneurs find that managing paperwork is only the beginning - the real challenge lies in validating their ideas, attracting customers, and building steady revenue streams.

This is where IdeaFloat comes in. For just $20 a month, this AI-powered platform helps you validate market demand, refine your go-to-market strategy, and create solid financial plans. By handling these critical areas, IdeaFloat allows you to focus on growing your revenue and scaling your business.

Countless entrepreneurs have used IdeaFloat to move from idea validation to running successful, profitable businesses. Its combination of market validation, strategic planning, and compliance support gives you the tools to confidently focus on finding customers, increasing revenue, and scaling your venture.

With your legal foundation set, you’re now ready to channel your energy into building a successful and thriving enterprise.

Conclusion: Your Legal Business Setup Complete

Congratulations! You've tackled the key steps to legally establish your business in the United States. From selecting the right business structure to securing your EIN from the IRS, understanding sales tax obligations, and putting compliance systems in place, you've laid the groundwork for a business that’s ready to operate smoothly and securely.

This solid legal foundation safeguards your personal assets, sets you up for growth, and ensures you stay on the right side of both federal and state regulations. With these essentials in place, it's time to shift your focus to validating your market and turning compliance into profitability.

Many entrepreneurs master the legal aspects but hit roadblocks when it comes to proving market demand. That’s where IdeaFloat steps in. For just $20 per month, this AI-powered platform helps you validate your business idea using real market data, craft a go-to-market strategy, and create financial projections that highlight profitability. Over 1,000 entrepreneurs worldwide have already used IdeaFloat to turn their legally compliant businesses into thriving ventures.

Now it’s time to build something your customers truly want. Your journey is just beginning!

FAQs

What’s the difference between an LLC and a corporation, and how do I choose the right one for my business?

The key distinctions between a Limited Liability Company (LLC) and a corporation lie in ownership, management, and taxation.

LLCs are owned by members and offer flexibility in how they’re managed. In contrast, corporations are owned by shareholders and follow a more formal structure, with a board of directors overseeing major decisions and officers handling daily operations.

Taxation is another major difference. LLCs are typically treated as pass-through entities, meaning profits are reported on the members’ personal tax returns, helping them avoid double taxation. That said, LLCs can opt to be taxed as a corporation if it aligns better with their financial strategy. Corporations, by default, face double taxation - once on company profits and again when dividends are distributed to shareholders. However, choosing S-corp status can help bypass this double taxation.

When deciding between the two, think about your business goals. LLCs work well for smaller businesses that value flexibility and a straightforward setup. Corporations, on the other hand, are a better fit for companies aiming to attract substantial investment or eventually go public.

How can I figure out which states I need to register for sales tax based on where my business operates and where my customers are located?

To figure out where you need to register for sales tax, start by assessing your business activities and where your customers are located. States generally require registration if your business meets their nexus standards. These standards can be based on physical presence - like owning an office or warehouse - or economic activity, such as your sales volume or transaction count.

The exact thresholds for economic nexus differ from state to state. For instance, some states mandate registration if your annual sales surpass $100,000 or if you process 200 transactions. It's crucial to review the specific requirements for each state to stay compliant. If this feels overwhelming, consider reaching out to a tax professional or using a tax compliance tool to make the process easier.

Why do I need an EIN for my business, even if I’m not hiring employees right away?

An EIN (Employer Identification Number) plays a key role in managing a business, even if you’re not planning to hire employees right away. It’s often necessary for tasks like opening a business bank account, applying for licenses, or filing federal taxes. Beyond that, having an EIN helps you keep your personal and business finances separate - something that’s critical for both legal and financial clarity.

Even as a sole proprietor, you might encounter vendors or clients who prefer an EIN over your Social Security Number (SSN) for tax reporting. This not only adds a layer of privacy but also gives your business a more professional edge.

Related Blog Posts

Get the newest tips and tricks of starting your business!