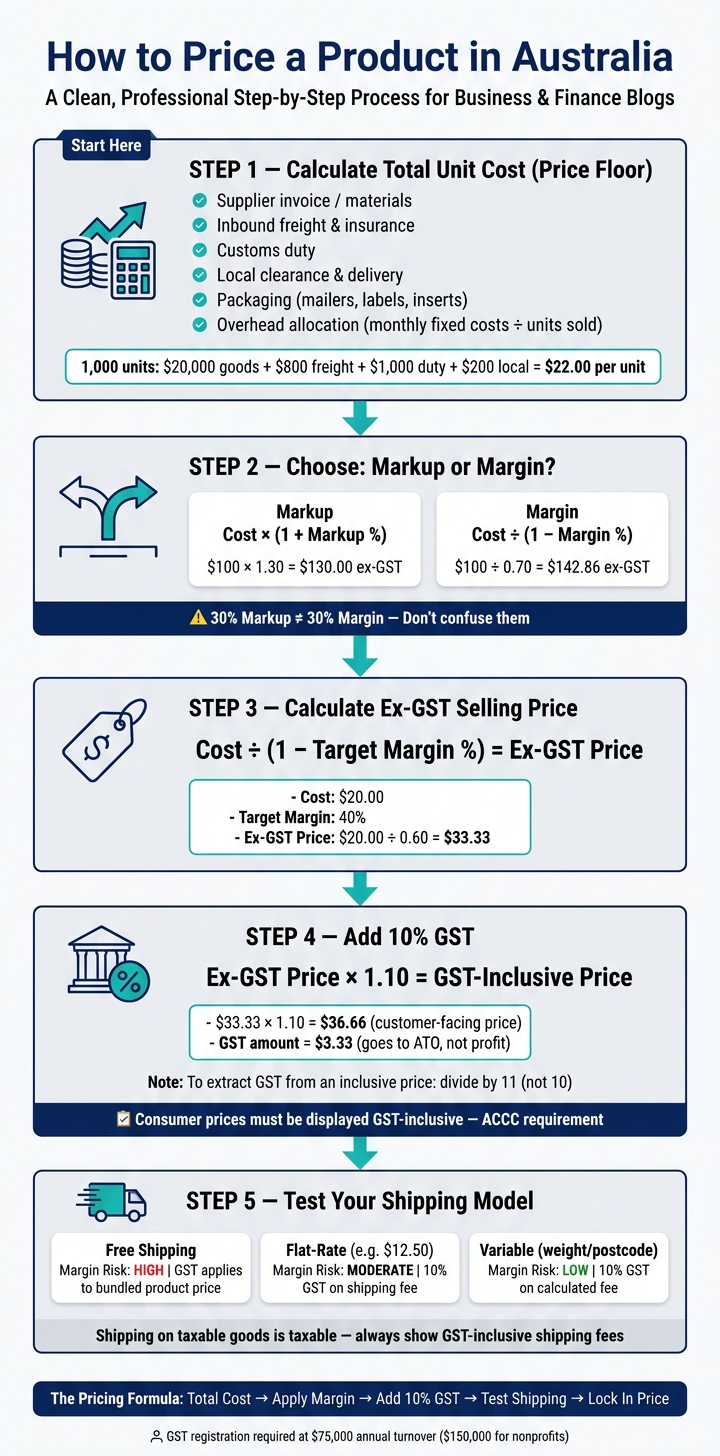

If I price a product in Australia, I use this order: cost first, margin second, GST last. That one sequence helps me avoid the two big pricing mistakes: missing costs and mixing up margin with markup.

Here’s the short version:

- I start with my total unit cost: product, packaging, freight, duties, overhead, and any shipping I absorb.

- I set my ex-GST selling price using a margin formula, not a markup formula.

- I add 10% GST after that to get the customer-facing price.

- I keep in mind that shipping is usually taxable too, so it also needs GST.

- If I sell to consumers in Australia, the displayed price should be GST-inclusive.

A simple example: if my cost is $20.00 and I want a 40% margin, I don’t add 40% on top. I divide $20.00 by 0.60 to get $33.33 ex-GST, then add 10% GST to get $36.66.

Quick comparison

| Item | What I use it for | Simple formula |

|---|---|---|

| Total unit cost | My pricing base | Product + freight + packaging + overhead |

| Markup | Add a percent to cost | Cost × (1 + markup) |

| Margin | Set profit as part of selling price | Cost ÷ (1 − margin) |

| GST | Get the final displayed price | Ex-GST price × 1.10 |

The main point is simple: if my cost base is right and my margin math is right, my final price is much less likely to be wrong.

How to Price a Product in Australia: GST, Margin & Shipping Step-by-Step

How to Calculate GST in Australia - GST Calculator Australia - Adding & Finding GST

sbb-itb-08dd11e

GST basics and price display rules in Australia

GST is a flat 10% tax on most goods and services sold in Australia. If your business hits $75,000 in annual GST turnover - or $150,000 for nonprofits - you need to register for GST. Once you're registered, consumer prices must be shown as one GST-inclusive amount. That number is the one your pricing formula needs to land on.

The ACCC warns that adding GST only at checkout can mislead consumers. So, in plain English, if you sell to consumers, the price on your product page, social post, or any public-facing ad should already include GST. You can't list $45 and then tack on $4.50 at checkout.

GST-inclusive vs. GST-exclusive prices

To add GST, multiply by 1.1. To pull GST out of a GST-inclusive price, divide by 11, not 10. If you divide by 10, you overstate the tax amount.

| Pricing Scenario | Ex-GST Price | GST Amount (10%) | Total Price Paid |

|---|---|---|---|

| GST-inclusive product | $90.91 | $9.09 | $100.00 |

| B2B ex-GST quote | $100.00 | $10.00 | $110.00 |

B2B quotes can show ex-GST pricing if they're clearly labeled. But that changes when you're selling to consumers.

Use the ex-GST figure as the base for your total cost breakdown.

How GST applies to shipping and delivery charges

Shipping for taxable goods is taxable too. If you charge $8.00 for shipping on a taxable product, that fee includes GST. The GST part is $0.73, worked out as $8.00 ÷ 11. Put that GST share into your shipping charge before you set your margin.

Treat shipping as part of your unit economics before you set margin.

How to calculate your full product cost before setting a price

A lot of underpricing happens for one simple reason: sellers leave costs out. It’s usually not a math problem. It’s a cost-tracking problem.

Your true per-unit cost is everything it takes to get a product made, brought in, packed, and ready to sell.

Direct costs: product, packaging, inbound freight, and landed cost

If you import goods, landed cost is your pricing base, not the supplier’s invoice price.

Landed cost includes:

- the supplier invoice

- inbound freight

- insurance

- customs duty

- local clearance or delivery charges

Exclude GST from your cost base. You reclaim that separately.

Use landed cost, not invoice price, when pricing imported products. Here's a sample landed cost breakdown for a shipment of 1,000 units:

| Cost Component | Total Shipment (ex-GST) | Per Unit (ex-GST) |

|---|---|---|

| Goods (Customs Value) | $20,000.00 | $20.00 |

| International Freight & Insurance | $800.00 | $0.80 |

| Customs Duty (5%) | $1,000.00 | $1.00 |

| Local Charges (Clearance, Port, Delivery) | $200.00 | $0.20 |

| Total Landed Cost | $22,000.00 | $22.00 |

That means your cost base is $22.00 per unit, not $20.00. That extra $2.00 may not look like much at first glance, but it’s the difference between pricing on the full cost and pricing on wishful thinking. This is the number your margin needs to sit on top of.

Packaging belongs in unit cost too. Mailers, inserts, labels, and tissue all count.

Indirect costs: overheads and shipping decisions

Overheads are the costs your business carries no matter how many units you sell. Think rent, software subscriptions, utilities, and admin time. These costs can be easy to ignore because they don’t show up on a supplier invoice, but they still need to be paid.

Do not leave them out of unit cost. To assign them the right way, add up your fixed monthly costs and divide that total by the number of units you expect to sell that month.

For example, if your monthly overheads are $2,000 and you sell 500 units, your overhead allocation is $4.00 per unit. Every sale needs to recover that amount.

Spread fixed overheads, payment fees, and expected return costs across each unit.

Shipping should only go into unit cost when you absorb it. If the customer pays shipping as a separate charge, keep it separate from the product price.

Once you have this total cost base, that’s the number you use for margin and markup. Next, turn this cost base into a selling price using margin and markup.

How to use margin and markup formulas to set a selling price

Once landed cost and overheads are built into your base cost, the next job is turning that cost into a selling price. This is where markup and margin come in.

They sound similar, but they don't work the same way. And yes, that difference changes the final price.

Margin vs. markup: the difference that changes your final price

Markup adds a percentage to your cost. Margin looks at profit as a percentage of the selling price.

Here are the formulas:

- Markup formula: Selling Price (ex-GST) = Cost × (1 + Markup %)

- Margin formula: Selling Price (ex-GST) = Cost ÷ (1 − Margin %)

A simple example makes the gap obvious. A 30% markup on a $100 cost gives you $130. But a 30% margin gives you $142.86.

| Metric | 30% Markup | 30% Margin |

|---|---|---|

| Cost Base | $100.00 | $100.00 |

| Calculation | $100 × 1.30 | $100 ÷ (1 − 0.30) |

| Ex-GST Price | $130.00 | $142.86 |

| Profit ($) | $30.00 | $42.86 |

| GST (10%) | $13.00 | $14.29 |

| Final Price (inc-GST) | $143.00 | $157.15 |

That’s why people mix these up and end up underpricing. A 30% markup is not the same as a 30% margin.

Apply the formula to ex-GST cost only.

Step-by-step pricing example in AUD

Here’s the full math for a physical product using a hypothetical handmade candle.

| Step | Description | Calculation | Result (AUD) |

|---|---|---|---|

| 1 | Total Cost per Unit | Materials ($12) + labor ($5) + packaging and inbound freight ($3) | $20.00 |

| 2 | Target Margin | Choose 40% margin | 0.40 |

| 3 | Ex-GST Price | $20.00 ÷ (1 − 0.40) | $33.33 |

| 4 | GST Amount | $33.33 × 0.10 | $3.33 |

| 5 | Final Display Price | $33.33 + $3.33 | $36.66 |

| 6 | Profit before GST | $33.33 − $20.00 | $13.33 |

So the customer pays $36.66. Your profit is $13.33. The GST part goes to the ATO, not into your profit.

One more thing: if shipping is charged separately, take it out of the product price and run the margin check again.

Then test whether free shipping, flat-rate shipping, or variable shipping still leaves your target margin in place.

Pick a shipping structure and check that your price still works

Once you've set an ex-GST price, test shipping against your target margin. This step matters more than it looks. The shipping model you pick changes what the customer pays, how much profit room you keep, and how GST is handled.

Free shipping vs. flat-rate vs. variable shipping

Each shipping model comes with a plain trade-off: smoother checkout on one side, margin protection on the other.

Free shipping can make the offer feel simpler because the customer sees one clean, all-in price. But it only works if average freight is already built into the product price.

Flat-rate shipping gives shoppers a set number at checkout, such as $12.50. That can reduce friction without hiding the cost inside the item price. It's a middle-ground option. The catch? You can still end up undercharging on heavier orders or deliveries to Western Australia, the Northern Territory, or other regional areas where freight costs run higher.

Variable shipping uses weight or postcode to price delivery. This protects margin best on heavy or bulky items because the customer pays the actual cost. That makes undercharging less likely. The downside is simple: a higher shipping quote at checkout can put some buyers off.

| Shipping Model | What the Customer Sees | Margin Risk | GST Treatment |

|---|---|---|---|

| Free Shipping | $0.00 (or "Free") | High - freight must be absorbed into the product price | GST applies to the total bundled price |

| Flat-Rate | A fixed fee (e.g., $12.50) | Moderate - risk of undercharging on heavy or remote orders | 10% GST applies to the shipping fee as a separate line item |

| Variable | Real-time cost by weight/location | Low - actual costs are passed to the customer | 10% GST applies to the calculated shipping fee at checkout |

If you're shipping taxable goods, shipping is taxable too. So any shipping fee you show must be GST-inclusive. After you choose your model, run the numbers again using the full delivered price, not just the product price.

Use IdeaFloat to test pricing, costs, and profitability

Before you lock anything in, test each shipping model against your target margin. Use IdeaFloat to see whether free, flat-rate, or variable shipping still leaves your target margin intact. You can also compare break-even points across different pricing setups.

If the math still holds, you're in good shape to launch.

Conclusion: Start with total cost, add margin, then apply GST

After you’ve tested shipping, do one last check. Total cost, margin, and shipping need to work together before you lock in a price.

Start with your total landed cost, then add your overhead allocation. That gives you your price floor.

The pricing sequence is simple: apply your target margin to total cost, then add GST. Margin and markup are not the same thing. If you get that step wrong, profit slips away fast.

Once your ex-GST price works, multiply it by 1.1 to get the final customer-facing price. Shipping charges also carry GST. If you absorb GST instead of passing it on, you keep less from each sale.

That last check turns a rough estimate into a price you can trust. A clear cost table and a fixed formula help you avoid pricing too low.

FAQs

Should I include payment fees and returns in unit cost?

Yes - include payment processing fees in your unit cost.

They’re variable costs, which means they go up or down with sales volume. If you leave them out, your numbers can look better than they are, and that can push you into underpricing. Over time, that eats into your profit.

Returns matter too. They’re part of the broader cost of doing business, even if they don’t show up on every single order. Your pricing should cover both variable costs and fixed costs so your margins hold up as you grow.

What if I’m not registered for GST yet?

If you’re not registered for GST, don’t charge GST on your sales. That means you shouldn’t say GST is included in your prices or show GST as a separate line on invoices, because you’re not collecting it for the Australian Taxation Office.

There’s another side to this too: if you’re not registered, you can’t claim GST credits on business expenses.

It’s smart to keep an eye on your turnover. GST registration becomes mandatory if your gross business income reaches, or is expected to reach, A$75,000 over a 12-month period.

How often should I recalculate my prices?

Pricing isn’t something you set once and walk away from. It needs regular review.

Go back to your numbers when market conditions shift, customer demand changes, competitors move, or your costs go up or down. Any of those changes can affect your profit.

It also helps to watch your sales data closely and test small pricing changes to find the price point that works best.

And don’t stop at the top-line number. Review specific cost items each year, like tariff classifications, since trade schedules can change.

Related Blog Posts

- How to Price Your Product: A Beginner's Guide

- How to Price Products for Healthy Margins Without Killing Demand

- The Cheapest Businesses to Start in Australia That Still Have Margin

- High-Margin Small Business Ideas in Australia for One-Person Teams